_04_27_2026_08_15_15_448770.jpg)

Amazon (NASDAQ: AMZN) closes at $263.99, $2.84T cap. AWS AI, ad growth & retail margins quietly re-rate Amazon into 2026's most complete megacap compounder. Full dive.

Key Highlights

- AMZN hit an all-time intraday high of $264.50 on its own anchor date — a milestone the article itself never mentions.

- AWS + Ads + Retail margin expansion are compounding consolidated profitability faster than revenue, making 36.81x the most defensible P/E in Amazon's history.

- At $2.84T, Amazon is the only megacap simultaneously exposed to AI infrastructure, consumer spending, and digital advertising — a macro hedge no other single stock offers.

Amazon (NASDAQ:AMZN) is three businesses welded together by a logistics spine: a global e-commerce franchise, a hyperscale cloud (AWS), and a fast-growing advertising platform that has become the third pillar of the consolidated story. Inside those three is a subscription engine (Prime), a streaming and content arm (Prime Video, MGM, live sports), a devices ecosystem (Echo, Kindle, Fire), a healthcare ambition (Amazon Pharmacy, One Medical), and a satellite-internet program (Project Kuiper).

The 2026 narrative on Amazon is increasingly margin-led. After years in which top-line growth was the marquee number, investors are now focused on the structural lift coming from the high-margin trio: AWS, advertising, and third-party seller services. Each of those lines carries margin profiles that are materially above the consolidated average, and as their share of revenue grows, the consolidated margin profile re-rates upward almost mechanically.

Stock Performance in 2026 (YTD)

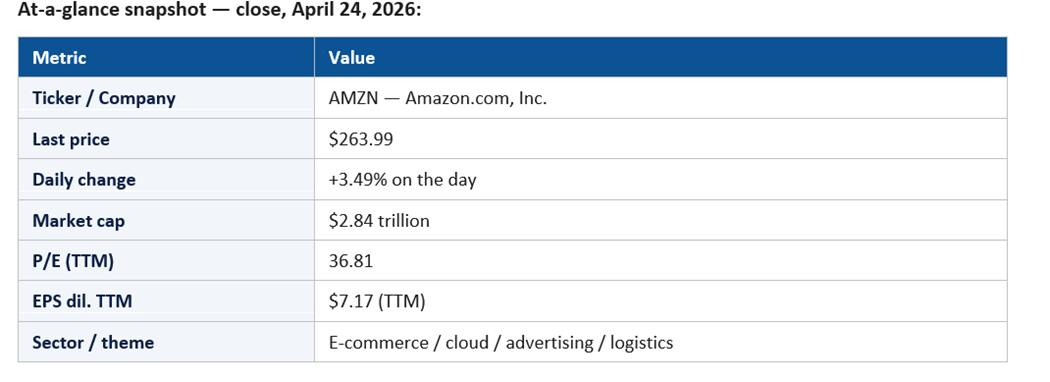

AMZN closed April 24, 2026 at $263.99, up 3.49% on the day, with a market capitalization of $2.84 trillion. The session move outpaced the S&P 500's 0.80% gain by a wide margin and confirmed Amazon's regime as one of the highest-beta megacaps when AI-infrastructure narratives turn positive.

At a P/E of 36.81 on $7.17 of TTM diluted earnings, AMZN trades at a clear growth premium but at a more grounded multiple than its prior decade — a function of growing earnings and a more disciplined capital story. The implied YTD trajectory is one of compounding: the stock has methodically converted operating-leverage upside into share-price gains without leaning heavily on multiple expansion.

On a tape that has rotated aggressively between AI-infrastructure beneficiaries and consumer-defensive names, Amazon has been one of the few megacaps able to participate in both regimes. The 3.49% session move is consistent with a stock that the market has decided is core to the AI-build-out story while still being underwritten by retail and ads.

Key Price Movements and Milestones

Three milestones shape the 2026 tape. First, the persistent consolidation through and beyond the $2.5 trillion threshold and the breakout into the $2.8T-plus zone. That breakout has changed the index-weighting math: Amazon now occupies a position in passive flows that didn't exist 18 months ago. Second, AWS quarterly print volatility has compressed: each cloud disclosure has reaffirmed an AI-led acceleration, removing one of the recurring sources of stock-specific drama from prior years.

Third, advertising has graduated from segment to story. The disclosure cadence around the ads business has tightened, and analyst models now treat it as a high-margin, double-digit-growth annuity that anchors the consolidated multiple. The +3.49% session reflects how much sentiment can move when AI-cloud and ads narratives reinforce each other on the same day.

Major Catalysts: Why the Stock Moved

The dominant 2026 catalyst is AWS AI. Amazon's strategic posture — multi-model neutrality on the inference side via Bedrock, plus aggressive investment in custom silicon (Trainium, Inferentia) and Anthropic-aligned capacity — has turned AWS into a credible second AI-cloud after Azure. Each quarter that AWS prints accelerating growth attributable to AI workloads validates that thesis and reduces the perceived gap to Microsoft.

The second catalyst is retail margin expansion. Years of network re-architecture — regionalization of fulfillment, robotics in the warehouse, last-mile optimization — have begun to drop visibly into the operating margin line. Investors care about margin trajectory more than about gross merchandise volume in 2026, and Amazon has methodically delivered on it.

The third catalyst is advertising. As more retail attention gets monetized at the point of search and discovery on Amazon properties, the ads business has turned into a consolidated-margin engine that few competitors can match in scale. Each quarter of 20%-plus growth in ads revenue reinforces the multiple.

Macro and Fed-rate sensitivity is mixed. AWS is sensitive to enterprise spending. Retail is sensitive to consumer health. Ads ride both. Amazon's consolidated exposure to the macro is therefore broad rather than concentrated, which is itself a kind of resilience.

Sector Trends Influencing the Stock

Three structural trends underwrite the 2026 thesis. First, the cloud-AI build-out is still in its early innings. Capacity is the binding constraint, not demand, and Amazon's capex is being deployed to capture share of a workload type — AI inference at enterprise scale — that maps cleanly to AWS's strengths.

Second, the retail-media advertising shift is durable. As cookies become unreliable and traditional digital ad targeting weakens, first-party purchase data has become the most valuable signal in the funnel, and Amazon owns more of it than any other public company.

Third, logistics is increasingly a moat rather than a cost center. The same network that ships Prime orders in hours can also serve as a third-party logistics platform — and as a vector for monetizing capacity beyond Amazon's own e-commerce demand. That optionality is rarely modeled, and is one of the quieter sources of upside.

Competitive Positioning

Amazon's competitive position in 2026 is layered. In retail, it remains the dominant U.S. e-commerce platform, with Walmart's e-commerce business as the most credible competitor and an expanding battle in groceries and same-day delivery. In cloud, AWS is one of three serious hyperscale options; the gap to Microsoft has narrowed but AWS still leads on overall workload count and on developer-tooling depth.

In ads, the competitor set is Google and Meta — but Amazon's first-party purchase data is a structurally different asset class. Advertisers increasingly view Amazon ads as the rare ROI-measurable spend in a fragmented digital ad world.

The most underrated competitive vector is Project Kuiper. Whatever it ultimately becomes commercially, the strategic value of low-earth-orbit connectivity to a logistics and cloud company is meaningful. It is option value, not 2026 P&L, but it is real.

Financial Highlights

TTM diluted EPS of $7.17 on a $263.99 share price gives Amazon a P/E of 36.81. The earnings power story is the heart of the bull case: operating income has compounded faster than revenue for several years, and the mix shift toward higher-margin segments has not yet plateaued.

AWS operating margin remains the single most-watched metric in the consolidated statement, with high-30s to low-40s margins depending on capex timing. Advertising margins are inferred to be even higher; retail margins, while structurally lower, are visibly expanding.

Free cash flow generation has firmly returned to the narrative after years in which it was suppressed by capex cycles. Amazon's ability to fund AI capex out of operating cash flow rather than incremental debt is a quietly important structural advantage relative to less-capitalized competitors.

Key Risks and Challenges

The first risk is regulatory. Amazon's footprint in retail, logistics, cloud, devices, and advertising is broad enough that antitrust scrutiny — both in the U.S. and Europe — is a permanent feature of the operating environment. Specific risks include marketplace conduct rules, AWS market-power inquiries, and Prime-bundling investigations.

The second risk is consumer health. Amazon's retail revenue is sensitive to discretionary spending, and a sustained consumer slowdown would test the margin expansion narrative just as it is hitting its stride.

The third risk is AI-capex digestion. AWS capex has scaled significantly to capture AI workloads, and any sign that demand growth is decelerating could compress segment operating margin before revenue catches down. That is the same risk the entire hyperscaler cohort faces — Amazon is not unique here, but it is exposed.

Finally, execution risk on the AI-product roadmap is real. Bedrock, Anthropic-aligned capacity, custom silicon, and AWS-native developer AI products all need to keep pace with Microsoft and Google. A stumble on any one of those fronts would dent the AI-cloud narrative.

Institutional and Investor Sentiment

Institutional positioning in Amazon has shifted decisively constructive in 2026. The combination of AWS AI exposure, advertising momentum, and visible retail margin expansion has made AMZN a near-consensus overweight in growth and core mandates. Sell-side price targets have ratcheted higher, and the bear case has narrowed primarily to multiple-compression risk rather than business deterioration.

The options market reflects relatively sober pricing of upside and downside, with implied volatility behaving as one would expect for a high-beta megacap rather than a speculative name. Amazon in 2026 has earned its place as a core compounder, not a story stock.

Signals to Watch in the Coming Quarters

Five concrete signals will define how Amazon's 2026 narrative evolves. The first is AWS growth net of foreign-exchange, with the AI contribution disclosed as clearly as possible. Investors compare AWS sequentially against Azure and Google Cloud at every print, and the gap dynamics determine where megacap allocators add and trim cloud exposure. Any clarity on Bedrock revenue, custom-silicon adoption, or Anthropic-related capacity utilization will be material.

The second signal is North American retail operating margin. The thesis that fulfillment regionalization, robotics deployment, and last-mile efficiency are structural rather than cyclical will keep being tested with each print. A widening gap between revenue growth and segment operating profit growth would re-rate the consolidated multiple meaningfully.

The third signal is advertising. The disclosed ad revenue line is one of the cleanest growth stories on the income statement, and each quarter the market wants visible double-digit growth, ideally with commentary on Prime Video monetization, sponsored-product expansion, and DSP traction. Any deceleration here would be read as a market-share or category problem, not an Amazon-specific issue.

The fourth signal is Project Kuiper. Throughout 2026, Kuiper has been an option-value narrative more than an income-statement contributor, but each launch milestone, customer-pilot disclosure, or commercial agreement updates the long-duration thesis. Kuiper does not need to drive the stock, but it does need to keep delivering credibility milestones to remain a free option in the bull case.

The fifth signal is capex commentary. The shape of Amazon's AI infrastructure spend, the implied return on capacity investment, and the cadence of activation will define free-cash-flow trajectory. The market in 2026 has tolerated elevated capex; the moment it stops tolerating it is the moment the multiple compresses.

Outlook for the Rest of 2026

The base case is operating-leverage continuation: AWS prints AI-driven acceleration; ads compounds at 20%-plus; retail margins drift higher; capex moderates as a percentage of revenue once AI buildout matures. In that scenario, EPS growth runs ahead of revenue growth and the multiple is defended on fundamentals rather than narrative.

The bull case is a fast-tracked monetization of advertising, driven by retail-media maturation and AI-driven ad-product improvements. The bear case is a consumer slowdown plus an AWS deceleration, which is the symmetric risk to the stock's 2026 leadership.

Amazon in 2026 is finally the business its long-term investors always insisted it would be: a logistics-and-cloud-and-ads compounder with the discipline of a mature company and the upside of an AI platform.

For now, the +3.49% session is the kind of move that confirms regime: when AI-infrastructure narratives turn constructive, AMZN is one of the names that participates without being a chip stock. That is exactly the slot the market has decided it owns.

Please wait processing your request...

Please wait processing your request...