An equity research deep-dive on Tesla, Inc. (NASDAQ:TSLA), closes at $376.30, 343x P/E, $1.41T cap. Tesla's robotaxi bet, Cybercab launch & Optimus optionality make it 2026's most debated megacap. Dive in.

Key Highlights

- Tesla’s valuation reflects extreme forward expectations, with a P/E above 340x driven by robotaxi and AI narratives.

- Energy storage and software revenue provide emerging diversification beyond automotive cyclicality.

- Execution risk in autonomy and pricing pressure in EV markets remain central to earnings outlook.

Tesla (NASDAQ:TSLA) is no longer just an electric-vehicle manufacturer. By 2026, the company's narrative spans automotive (Models S, 3, X, Y, Cybertruck, the next-generation low-cost platform), energy (Megapack and Powerwall storage, vehicle-to-grid), autonomy (Full Self-Driving software and the robotaxi program), robotics (Optimus humanoid), AI infrastructure (Dojo and the underlying training stack), and a global Supercharger network that has become an effective industry standard.

Investors who treat Tesla as a car company on a P/E basis tend to miss the equity story. Investors who treat it as a robotaxi-and-AI story on a 2030 model often overshoot. The market price in 2026 reflects a tension between those two camps, with the trailing P/E of 343.78 on $1.09 of TTM EPS revealing how dependent the multiple is on future, not current, earnings.

Stock Performance in 2026 (YTD)

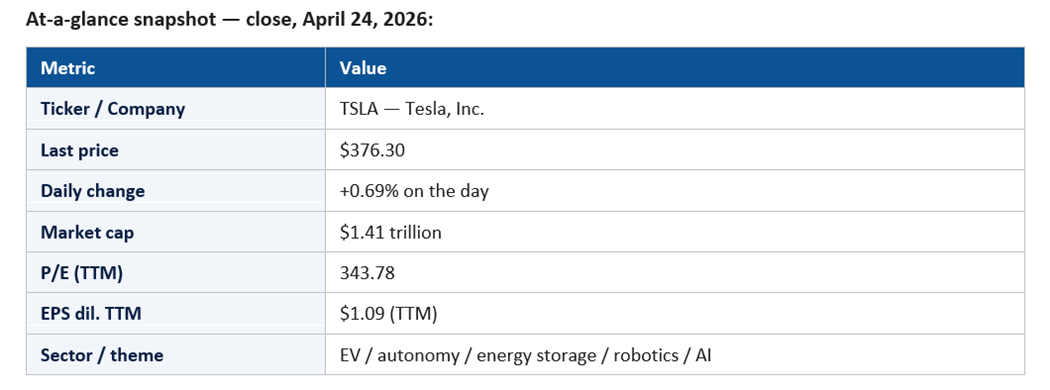

TSLA closed April 24, 2026 at $376.30, up 0.69% on a session in which AI-infrastructure names rallied hard. The market capitalization sits at $1.41 trillion. The trailing P/E of 343.78 is the most striking single number in the megacap universe and is a constant point of debate.

The implied YTD posture is volatile-with-narrative. Tesla has continued to trade at the intersection of three storylines: vehicle delivery cadence and pricing discipline, FSD/robotaxi commercialization, and Optimus/Dojo as long-duration AI options. On days when AI sentiment turns euphoric across the broader market, TSLA tends to participate; on days dominated by macro or auto-cycle nervousness, the stock can underperform sharply.

The +0.69% session sits inside that wider regime: a measured up-day that does not commit Tesla bulls or bears to anything decisive about the next quarter.

Key Price Movements and Milestones

Three milestones define the 2026 tape. First, the persistent re-rating around robotaxi commercialization. Each incremental data point — geographic expansion, ride volumes, FSD version improvements — has functioned as a discrete catalyst with sometimes outsized stock impact relative to immediate revenue.

Second, the energy-storage segment has continued to grow into a meaningful contributor to consolidated revenue and gross profit. That is the calmest, most under-appreciated part of the equity story, and the one analysts increasingly point to when defending the valuation.

Third, automotive gross margin volatility has persisted but moderated. The high-volatility era of price cuts and margin shocks has given way to a more disciplined posture, with margin recovery showing up modestly across the year.

Major Catalysts: Why the Stock Moved

The dominant 2026 catalyst is robotaxi. The path from supervised FSD to unsupervised robotaxi service is still being written in real time, with regulatory permissions, fleet scaling, ride economics, and software reliability each functioning as moving variables. Each new market launch, each new mile-driven disclosure, and each FSD version step has been a discrete catalyst.

The second catalyst is the next-generation, lower-priced vehicle platform. The success or failure of Tesla's lower-cost vehicle program is one of the most significant operating questions for the 2026–2027 narrative; demand and unit economics from this platform will materially shift the consolidated revenue base.

The third catalyst is energy. Megapack deployments, particularly to grid-scale customers, have become a meaningful and steadily growing contributor. Battery cell economics — driven by both Tesla's internal manufacturing and external supply — are a quieter but important variable in the model.

The fourth catalyst is Optimus and Dojo. Both remain pre-revenue or sub-scale, but each milestone (hardware iteration, in-factory deployment, model performance) shifts how investors price the long-duration option value.

Macro and Fed-rate sensitivity is real and bidirectional. Rate cuts support auto affordability; rate increases compress demand. Geopolitics matter through tariffs, supply chains, and access to specific markets — particularly China.

Sector Trends Influencing the Stock

Three sector trends underwrite the 2026 thesis. First, the EV market is normalizing. The era of breakneck growth has given way to a more competitive, more mature global EV market, with Chinese OEMs (BYD especially) representing the most serious global competitor. Tesla's response has emphasized cost, scale, and brand rather than pure pricing.

Second, the autonomy sector is concentrating. Waymo and Tesla represent two distinct strategic approaches — sensor-rich versus camera-only, geofenced rollout versus generalized FSD — and the market has yet to definitively pick a winner. Both can succeed; both can stumble.

Third, energy storage is one of the most under-appreciated growth sectors in the market. Grid-scale storage is becoming a strategic infrastructure category, and Tesla's Megapack franchise has placed it at the front of that wave.

Competitive Positioning

Tesla's competitive position in 2026 is best described as differentiated-but-pressured. In automotive, the company faces intense competition from BYD and other Chinese EV makers globally, and from a maturing EV lineup at legacy OEMs. Tesla's brand, charging network, and software experience remain meaningful advantages, but pricing power is no longer unilateral.

In autonomy, Tesla competes with Waymo for narrative leadership and operational primacy. Waymo's geofenced robotaxi service has demonstrated commercial viability earlier; Tesla's bet is that a generalized, vision-based FSD scales more quickly once it crosses the threshold of unsupervised reliability. Both sides of that argument are credible.

In energy storage, Tesla competes with a smaller cohort of Chinese and U.S. battery makers; the brand and integration advantage remains real. In humanoid robotics, the field is still pre-commercial, but Tesla is one of a small number of companies with a credible at-scale ambition.

Financial Highlights

TTM diluted EPS of $1.09 against a $376.30 share price gives Tesla a P/E of 343.78. That number is intentionally provocative; it is also legitimate to the extent that Tesla's earnings have been temporarily compressed by a mix of pricing discipline, capex for next-generation products, and ongoing investment in autonomy and AI infrastructure.

Revenue mix has continued to evolve. Automotive remains the largest line, but energy and services have grown into meaningful segments, and software/FSD revenue (deferred and recognized) is a high-margin layer that the bull case has long argued is under-appreciated.

Free cash flow generation has held up through a period of significant capital investment. Tesla's ability to fund both auto and AI/robotics ambition out of operating cash flow has been a quieter but important financial signal.

Key Risks and Challenges

The first risk is autonomy execution. Robotaxi is the central pillar of the bull thesis; any sustained delay or technical setback meaningfully compresses the multiple.

The second risk is auto-cycle competition. Chinese OEMs continue to set the pace on price and product cadence in the global EV market, and Tesla's automotive margins are sensitive to that pricing pressure.

The third risk is regulatory. Both autonomy and energy operate inside complex, evolving regulatory regimes. A negative regulatory event in a major market — particularly around FSD operations — could disrupt the narrative.

The fourth risk is key-person and governance. Tesla's equity story remains uniquely tied to its CEO; changes in role, compensation, or focus continue to be material narrative variables.

Institutional and Investor Sentiment

Institutional positioning in Tesla in 2026 is bifurcated. Some growth and thematic mandates remain meaningfully overweight; many traditional core mandates remain underweight or neutral. Sell-side coverage is among the most divergent in the megacap universe, with target prices spanning a much wider range than is typical.

Retail investor enthusiasm continues to be a meaningful factor in price action, with options activity often amplifying intraday moves. The combination of institutional ambivalence and retail enthusiasm produces the kind of two-sided volatility that has defined the stock for years.

Signals to Watch in the Coming Quarters

Six concrete signals will define how the Tesla narrative evolves. The first is robotaxi geographic expansion. Each new operating market, each disclosed mile-driven count, and each iteration of the ride-economics commentary moves the implied long-run TAM. The market has been willing to pay for option value, but it wants visible scaling and unit economics commentary at each milestone.

The second signal is the next-generation low-cost vehicle platform. Production timing, cost structure, gross margin profile at launch, and demand trajectory will collectively determine whether the platform is the volume catalyst the bull case requires or another delay-driven disappointment.

The third signal is FSD version progression. Each release — particularly any release that meaningfully changes the supervised-versus-unsupervised distinction or the geographic operating envelope — is a discrete catalyst. Investors care less about benchmark improvements than about the operational implications for robotaxi and FSD subscription monetization.

The fourth signal is energy-storage deployments and Megapack backlog. The energy segment has been the steadiest contributor to consolidated growth; any quarter that disclosed accelerating deployments, longer backlog, or improving gross margin would reinforce the diversification narrative.

The fifth signal is Optimus and Dojo milestones. While neither is a near-term P&L driver, each generation of hardware iteration, in-factory deployment metric, and AI-training capacity disclosure shifts the long-duration option value embedded in the multiple.

The sixth signal is auto gross margin ex-credits. The path of automotive gross margin remains the most direct read on pricing discipline, cost structure, and product-mix dynamics. The 2026 trajectory has been incrementally constructive; any reversal would be a meaningful narrative event.

Outlook for the Rest of 2026

The base case is continued narrative-driven volatility. Robotaxi expansion delivers incremental but not yet definitive proof points; the new vehicle platform launches with reasonable but not extraordinary reception; energy compounds quietly; Optimus and Dojo continue to function as long-duration options. In that scenario, the stock could stabilize in a wide band around current levels.

The bull case is a clear inflection in robotaxi economics combined with a successful low-cost vehicle launch and continued energy growth. That combination could meaningfully re-rate the stock higher and partially close the gap between the trailing P/E and a more rational forward P/E.

The bear case is a slower-than-expected robotaxi ramp, compounded by auto pricing pressure and any execution issues on the new platform.

Tesla in 2026 is not priced for what it is. It is priced for what its believers are convinced it will become. That gap is both the bull case and the risk.

For now, the modest +0.69% session reflects the stalemate between camps. Until robotaxi or the new vehicle platform delivers something definitive, the stock will keep doing what it has done all year: trade on narrative, with everyone waiting for the next data point.

Please wait processing your request...

Please wait processing your request...