Image Source : Krish Capital Pty Ltd

Index Update: U.S. stocks advanced on Wednesday, with the Nasdaq hitting a record high and the Dow and S&P 500 posting their first gains in three sessions, driven by strong tech sector performance and AI optimism. Nvidia and Palantir led the gains, while Verona Pharma surged over 20% on acquisition reports involving Merck. On the policy front, President Trump announced a 50% tariff on Brazilian imports, which Fed minutes later highlighted as potentially inflationary, influencing the central bank's cautious stance on rate cuts.

Market Movers: On Wednesday, the top gainers were Evoke Pharma, Inc (+162.78%), followed by Basel Medical Group Ltd (+98.90%). On the contrary BitMine Immersion Technologies, Inc (-40.16%) and RxSight, Inc (- 37.84%) declined the most the same day.

Commodities Update: Crude oil prices declined, with WTI falling below $68 and Brent slipping under $70 per barrel, amid rising concerns over global trade disruptions following new U.S. tariff threats, including on Brazil and copper imports. Weighing further on oil was a surprise 7.1 million barrel build in U.S. crude inventories, though declines in gasoline and distillate stocks signaled solid demand. Geopolitical tensions in the Red Sea offered some support, while upcoming OPEC+ supply increases in September raised concerns about market balance despite the UAE noting strong ongoing demand. Precious metals advanced as gold rose to around $3,320 per ounce and silver climbed above $36.50, supported by a weaker U.S. dollar and falling Treasury yields. Investor sentiment was influenced by Fed minutes revealing division over the timing of rate cuts, with most policymakers open to easing later this year. Market participants also reacted to President Trump's expanded tariff agenda targeting 21 countries, intensifying concerns about inflation and global trade uncertainty.

Macro Update: President Trump announced a 50% tariff on copper imports starting August 1, citing national security concerns and the need to protect domestic production of this critical material. He emphasized copper's importance in sectors like defense, semiconductors, and energy. In 2024, the U.S. imported nearly half of its copper needs, with Chile, Canada, and Mexico expected to be the most impacted by the new tariffs.

Bonds Commentary: The 10-year U.S. Treasury yield stabilized around 4.33% after a prior sharp drop, supported by strong demand at a bond auction. Fed minutes showed most policymakers are open to rate cuts later this year, while markets also reacted to Trump's push for a significantly lower Fed funds rate and hints of a dovish Fed nominee in 2026. On the trade front, Trump announced a 50% tariff on Brazilian imports and imposed new duties on several other countries, raising concerns over inflation and global trade tensions. Attention now turns to potential trade deals with India and the EU.

Dollar Commentary: The U.S. dollar index fell for a second straight day to around 97.3 as investors shifted toward riskier assets amid a broad market rally and declining Treasury yields. The dollar weakened further following Fed minutes showing openness to rate cuts later this year. However, it jumped over 2% against the Brazilian real after President Trump announced a 50% tariff on Brazilian imports and additional duties on eight other countries. Markets now await potential trade deals with India and the EU.

Futures Update: U.S. stock futures edged lower as investors reacted to renewed trade tensions, with President Trump targeting Brazil with potential new tariffs amid his ongoing tariff agenda. The Dow, S&P 500, and Nasdaq 100 futures all registered modest declines. Meanwhile, minutes from the Federal Reserve's latest meeting indicated a possible interest rate cut later this year. In corporate news, shares of WK Kellogg surged after-hours following reports that Ferrero may be close to acquiring the cereal maker.

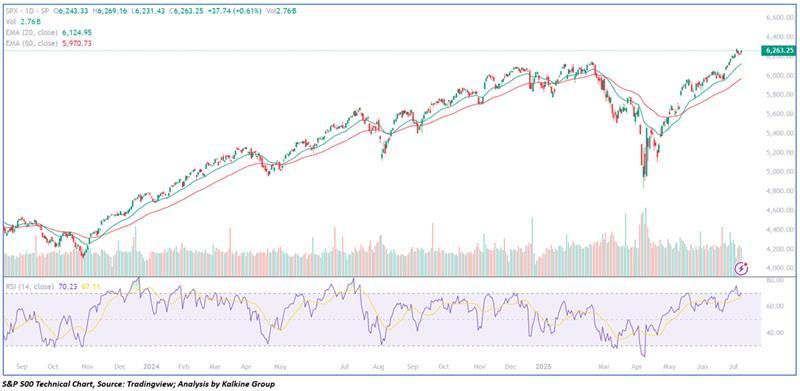

Following a subdued and choppy trading session on Tuesday, stocks largely moved higher throughout Wednesday's trading day. The S&P 500 rose by 37.74 points, or 0.61%, finishing at 6,263.25. From a technical perspective, the index remains above critical resistance zones, suggesting the possibility of continued gains in the short term. Moreover, the 14-period Relative Strength Index (RSI) is on an upward trajectory, reflecting ongoing bullish strength unless a divergence appears. Key support levels are around 6,100, while resistance is anticipated near 6,380.

Please wait processing your request...

Please wait processing your request...