Image Source : Krish Capital Pty Ltd

Index Update: US stocks fell on Monday despite President Trump extending a 90-day tariff pause on Chinese goods, with the Dow down 0.45%, the S&P 500 off 0.25%, and the Nasdaq down 0.3%. Losses were broad-based, led by energy, real estate, and technology sectors. Markets are also pricing in a near 90% chance of a Fed rate cut in September, while Trump announced a deal for Nvidia and AMD to remit 15% of revenue from certain AI chip sales to China and confirmed that gold imports would remain tariff-free.

Market Movers: On Monday, the top gainers were Telos Corporation (+62.61%), followed by International Money Express, Inc. (+60.56%). On the contrary Thumzup Media Corporation (-38.87%) and Owens & Minor, Inc. (-34.70%) declined the most the same day.

Commodities Update: WTI crude rose to $64.1 per barrel and Brent to $66.8 after President Donald Trump extended the US–China tariff truce by 90 days, averting new tariffs and easing fears of weaker energy demand. Attention now shifts to US–Russia talks on the Ukraine war, though both Trump and Ukrainian President Zelensky have played down the likelihood of a breakthrough. A peace deal, if reached, could lower risks to Russian oil supply, while traders also await key OPEC, US EIA, and IEA reports for fresh supply–demand cues. Gold rebounded to around $3,350 per ounce after Monday’s 1.6% drop, as investors awaited US inflation data for clues on the Federal Reserve’s rate path. Prices had fallen after Trump clarified that gold imports would not face tariffs, alongside his extension of the tariff truce with China. Markets are also watching the upcoming Trump–Putin meeting in Alaska on August 15 for potential developments in the Ukraine conflict.

Macro Update: The US NFIB Small Business Optimism Index climbed to 100.3 in July 2025, its highest in five months and above the long-term average, beating forecasts of 98.6. Gains were driven by improved expectations for business conditions and expansion, with 36% of owners anticipating better conditions and 16% seeing it as a good time to expand. Labor quality emerged as the top concern, while only 11% cited inflation as their biggest challenge. The US annual inflation rate is projected to accelerate for a third consecutive month to 2.8% in July, the highest since February, driven by retailers passing on higher import duties in goods like household furnishings and recreational items. Core inflation is expected to edge up to 3%, with the monthly core CPI rising 0.3%—its fastest pace in six months—amid increases in used car and airline fares, while gasoline and new car prices decline.

Dollar Commentary: The dollar index held near 98.5 as markets awaited July CPI data, expected to show a 0.2% monthly rise and an annual increase to 2.8%, with core CPI seen at 0.3%. Despite persistent inflation signals, investors are pricing in a near 90% chance of a September Fed rate cut. A 90-day extension of the US–China trade truce and an upcoming Trump–Putin meeting on the Ukraine conflict also drew market attention.

Bonds Commentary: The US 10-year Treasury yield held near 4.28% as investors awaited July CPI data, expected to show a 0.2% monthly rise and an annual increase to 2.8%, with core CPI seen up 0.3%. Despite lingering inflation pressures, markets are pricing in a near 90% chance of a September Fed rate cut. Traders also look ahead to PPI, retail sales, and industrial production data, while a 90-day extension of the US–China trade truce offers more time for negotiations.

Futures Update: U.S. stock futures were mixed as investors awaited key inflation data that could influence the Federal Reserve’s interest rate outlook. The previous session saw declines in major indexes, partly due to concerns over reports that leading semiconductor companies agreed to give the U.S. government a 15% share of their AI chip sales to China, raising worries about margin impacts and potential precedent for taxing critical exports. In other developments, the chief economist of the Heritage Foundation was appointed as the new U.S. Bureau of Labor Statistics commissioner shortly after the previous head’s dismissal, and Elon Musk accused Apple of favoring OpenAI’s ChatGPT over his AI start-up xAI on the App Store.

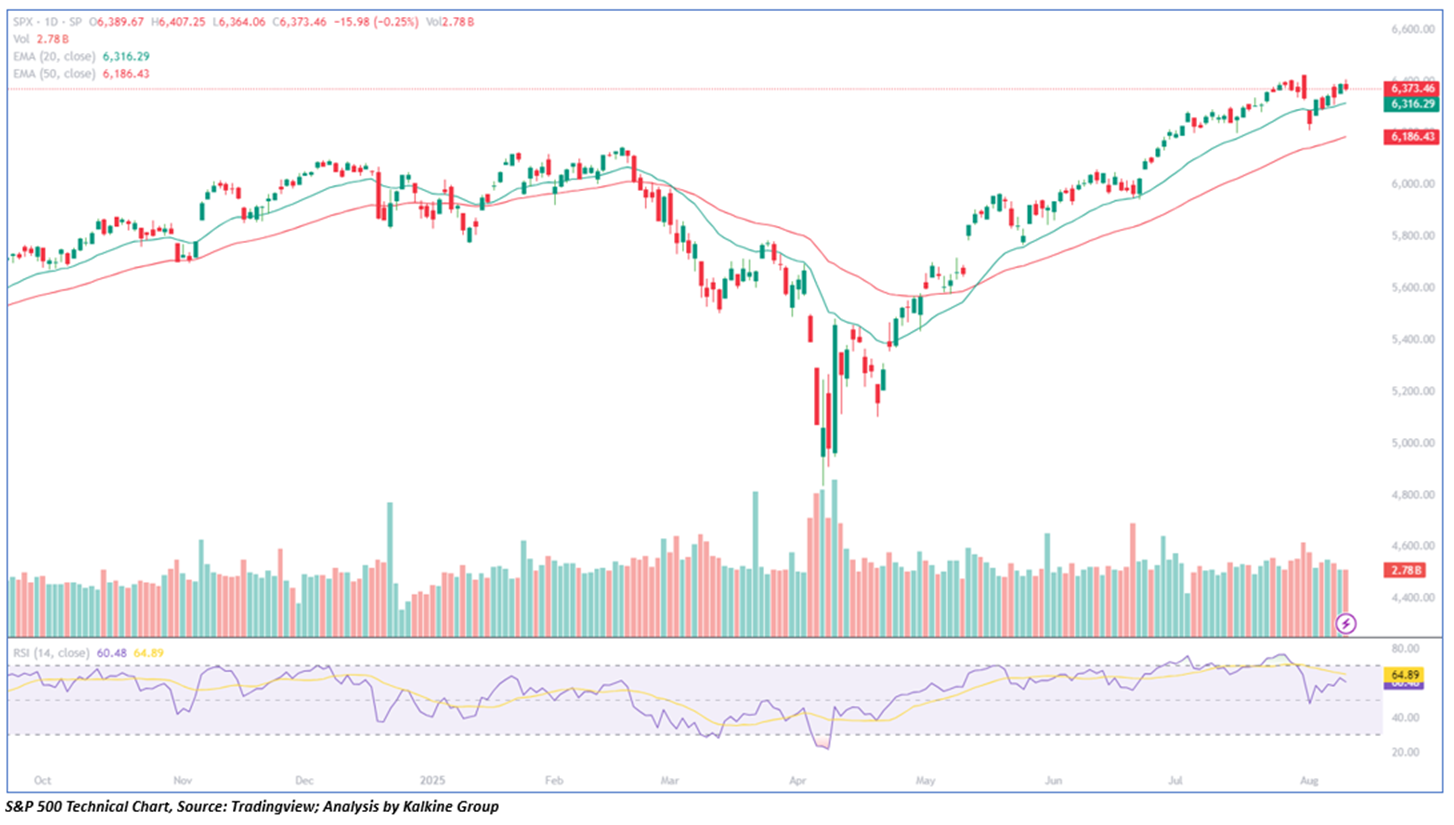

Following a strong rally in the previous week, stocks showed a lack of clear direction during Monday’s trading session. The choppy trading on Wall Street reflected traders’ caution ahead of the upcoming July CPI report from the Labor Department. The S&P 500 fell by 15.98 points, or 0.25%, closing at 6,363.46. From a technical standpoint, the index price is approaching a previous supply zone and may experience an extended period of consolidation in the near term. The 14-day RSI remains above the midpoint, indicating ongoing bullish momentum. Support levels are reinforced by other key moving averages below the current price, with important support near 6,300 and resistance around 6,488.

Please wait processing your request...

Please wait processing your request...