An equity research deep-dive on Exxon Mobil (NYSE:XOM), anchored on the April 24, 2026 close. The largest Western supermajor is navigating a year in which the energy transition and the AI-data-center power thirst are colliding head-on.

Key Highlights

- Exxon’s valuation reflects improved capital discipline and diversified earnings across upstream, downstream, and chemicals.

- AI-driven power demand is reshaping long-term natural gas and energy market dynamics.

- Strong free cash flow supports sustained capital return and balance sheet stability.

Exxon Mobil (NYSE:XOM) is the largest Western integrated oil and gas company, with global upstream production, the largest U.S. refining footprint, a large chemicals business, and a low-carbon-solutions arm that is increasingly part of the corporate narrative. Following its consolidation of Pioneer Natural Resources, the company holds one of the most attractive upstream resource bases in the world, anchored by a deep, low-cost-of-supply position in the Permian Basin and complemented by deepwater positions in Guyana and other strategic basins.

By 2026, the equity story is shaped by three forces. First, capital discipline and structurally improved cost of supply have made XOM's earnings more resilient through commodity cycles. Second, the chemicals and downstream segments add diversification that is often underappreciated by investors who treat the stock as a pure oil-price proxy. Third, the AI-data-center power-demand wave has reshaped the longer-term gas demand narrative in ways that are constructive for integrated operators with reliable, low-emissions gas supply.

Stock Performance in 2026 (YTD)

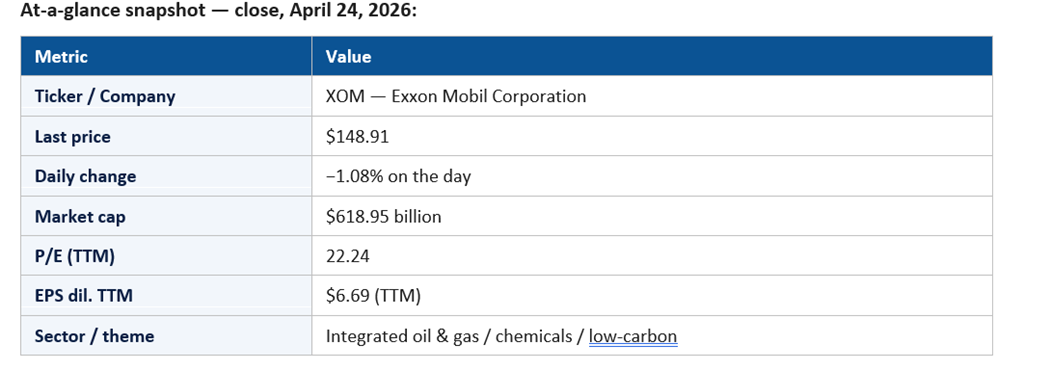

XOM closed April 24, 2026 at $148.91, down 1.08% on the day, with a market capitalization of $618.95 billion. The trailing P/E of 22.24 on $6.69 of TTM diluted EPS reflects a reasonably priced cyclical with embedded structural improvements. The implied YTD posture has been shaped by oil-price moves, OPEC+ supply discipline, geopolitical developments, and the broader energy-transition narrative.

On the April 24 session, the broader energy complex was modestly weak — Chevron −1.27%, ConocoPhillips −2.10% — even as the AI-led tape lifted the index. That divergence is consistent with a regime in which oil names trade more on commodity dynamics and supply discipline than on the broader risk-on/risk-off pulse of the index.

Key Price Movements and Milestones

Three milestones define the 2026 tape. First, the persistent consolidation around the $145–$155 zone, with the stock trading in a wide commodity-driven band. Second, capital return — the buyback and the dividend — has continued to be a defining feature of investor positioning, providing a structural bid that shapes intraday action.

Third, project execution milestones — particularly Permian throughput, Guyana FPSO ramps, and key downstream and chemicals projects — have functioned as discrete catalysts, with the market responding to each disclosure of cost of supply, project economics, and capital efficiency.

Major Catalysts: Why the Stock Moved

The dominant 2026 catalyst is the global oil supply-demand balance. OPEC+ production decisions, U.S. shale supply trajectory, Russian export dynamics, and demand growth from emerging markets collectively determine the spot price, which in turn drives upstream earnings. Each major macro print and OPEC+ communication has been a discrete catalyst.

The second catalyst is gas. The intersection of LNG demand growth, AI-data-center power demand, and pipeline-infrastructure constraints has shifted the longer-term gas narrative meaningfully constructive. Investors increasingly view integrated operators with low-cost gas supply as structurally advantaged in the AI-power era.

The third catalyst is project execution. Each disclosure on Pioneer integration synergies, Permian production growth, Guyana ramp, and downstream/chemicals project delivery is a discrete narrative event.

The fourth catalyst is low-carbon. CCS, hydrogen, and biofuels investments have grown in narrative importance, with each commercial milestone shifting how investors view the long-duration optionality of the company's energy-transition strategy.

Macro and Fed-rate sensitivity is meaningful — energy is rate-sensitive through the global growth channel. Geopolitics matter directly through sanctions, conflict, and trade dynamics that affect physical supply and pricing.

Sector Trends Influencing the Stock

Three structural trends underwrite Exxon's 2026 thesis. First, U.S. upstream consolidation has restructured the competitive landscape, concentrating high-quality acreage in the hands of a smaller number of disciplined operators. ExxonMobil-Pioneer is the largest of those combinations and the principal beneficiary.

Second, the global LNG market continues to grow, with U.S. Gulf Coast capacity ramps, European import demand, and Asian buyer commitments all reinforcing the structural picture. Integrated operators with embedded gas supply are well-positioned in that environment.

Third, the AI-data-center power-demand surge has reshaped utility and IPP capacity planning, with natural gas as a bridge fuel benefiting from the speed and reliability constraints of the buildout. That trend has been one of the most significant under-appreciated supports for integrated operators in 2026.

Competitive Positioning

Exxon's competitive position in 2026 is one of scale, integration, and cost discipline. Among Western supermajors, XOM and Chevron are the two structurally advantaged operators, with the European supermajors operating more capital-constrained energy-transition strategies. Within the U.S. shale industry, the post-consolidation Permian operator group is increasingly dominated by a small number of well-capitalized operators, and Exxon is the largest.

In chemicals, ExxonMobil's large-scale, integrated complexes provide a cost advantage that has consistently translated into segment-level earnings resilience through commodity cycles. In downstream, the U.S. refining footprint remains advantaged by complexity, scale, and integration with the upstream.

In low-carbon, the strategy is explicitly anchored to capabilities Exxon already possesses — subsurface, project execution, large industrial complexes — rather than to greenfield bets in unrelated areas.

Financial Highlights

TTM diluted EPS of $6.69 on a $148.91 share price gives Exxon a P/E of 22.24. Free cash flow generation has remained strong across the cycle, supporting both meaningful capital return and a measured capital expenditure program.

The dividend continues to be one of the most-watched aristocrat-tier yields in the megacap universe, providing a structural component of total return that complements buybacks. Capital expenditure has been disciplined relative to the structural improvement in cost of supply, with Pioneer integration synergies adding to the efficiency story.

Balance-sheet strength has been a recurring narrative. Exxon's net debt levels remain manageable, providing the flexibility to act counter-cyclically — buying assets at attractive prices when peers are stressed.

Key Risks and Challenges

The first risk is commodity price. Oil and gas prices are subject to a wide range of macro, geopolitical, and supply-side variables, and a sustained downside move would compress upstream earnings even with the structural cost-of-supply improvements.

The second risk is the energy transition. Long-duration concerns about oil demand peaking and ultimately declining remain part of the equity story, and any acceleration in transition policy or technology would raise the cost of capital for the sector.

The third risk is regulatory. Methane regulation, climate disclosure, and tax dynamics across multiple jurisdictions all affect the cost structure and the strategic flexibility of the franchise.

The fourth risk is project execution. Major capital projects across upstream, downstream, chemicals, and low-carbon all carry execution risk that, while well-managed historically, is never zero.

Why Exxon Has Become the Quiet Beneficiary of the AI Power Story

The dominant narrative around AI in 2026 has belonged to chips, hyperscaler capex, and accelerator architectures. The under-told story is that every gigawatt of new data-center demand is a gigawatt of net-new electricity load that has to come from somewhere, and a meaningful share of that somewhere is natural gas. Integrated operators with reliable, low-emissions gas supply are positioned to monetize that demand for years, and Exxon is at the front of that line.

What makes XOM specifically advantaged is the combination of upstream resource quality and downstream connectivity. The Permian position, post-Pioneer, is one of the lowest-cost gas-and-liquids supply basins in the world. The Gulf Coast LNG and chemicals complex provides the export and conversion optionality. Together, these assets convert AI-power demand into realized free cash flow at multiple points in the value chain rather than at any single bottleneck.

The result is an equity that has spent 2026 quietly inverting the conventional wisdom about energy and AI. The market expected oil majors to be losers in the AI-narrative trade. What has emerged is the opposite: integrated operators with the right asset mix have been steady beneficiaries, and Exxon's combination of capital discipline and structural advantage has positioned it to participate without taking on the volatility of the pure cyclicals.

Institutional and Investor Sentiment

Institutional sentiment on Exxon in 2026 is constructive but not euphoric. Many income-oriented and value mandates carry XOM as a core holding because of the dividend and capital-return profile. Sell-side coverage is broadly positive, with the bull case anchored to capital discipline and integrated economics, and the bear case anchored to long-duration transition risk.

The options market reflects measured pricing of upside and downside, consistent with a cyclical with structural improvement. Energy-sector volatility tends to spike around macro events rather than firm-specific ones.

Signals to Watch in the Coming Quarters

Six concrete signals will define how the Exxon narrative evolves. The first is the pace of Permian production growth and the realized cost of supply. Pioneer-related synergies have been a multi-year unlock; the market wants visible quarterly evidence that the integration is delivering as promised on cost-per-barrel, well productivity, and capital efficiency.

The second signal is Guyana ramp. Stabroek block production milestones, FPSO commissioning timing, and the disclosed economics of incremental projects collectively define the long-tail growth trajectory of upstream. Each milestone is a discrete narrative event.

The third signal is gas and LNG. Pricing dynamics, contract structures, and any commentary on AI-data-center demand integration into long-term gas planning will reframe how investors think about the value of integrated gas exposure.

The fourth signal is downstream and chemicals. Refining cracks, chemicals margins, and the operating performance of major integrated complexes collectively determine whether the diversified earnings story holds when upstream prices soften. The 2026 trajectory has been mixed; investors want stabilization.

The fifth signal is low-carbon. Each commercial milestone in CCS, hydrogen, biofuels, or lithium reframes the long-duration optionality. The strategy is explicitly asset-leveraged, but each project that converts from FID to operations is a discrete proof point.

The sixth signal is capital return. Buyback pace, dividend increases, and any commentary on the relative balance between distribution and reinvestment determines the total-return profile. The dividend has been a defining feature; the buyback has been the swing variable.

Outlook for the Rest of 2026

The base case is continuation: oil and gas prices remain rangebound; Pioneer integration synergies continue to deliver; Guyana ramps as expected; chemicals stabilizes; capital return continues. In that scenario, the stock grinds higher in line with operating earnings and the dividend, with the multiple holding in the low-to-mid 20s.

The bull case is a sustained tightening in oil and gas markets — driven by OPEC+ discipline, AI-data-center gas demand, or geopolitics — combined with above-plan project execution. The bear case is a sustained commodity weakness combined with regulatory or transition shocks.

Exxon in 2026 is the integrated supermajor that has spent the AI year quietly proving that the most boring assets in the index — pipelines, gas, refining capacity — are exactly what the AI economy is going to need.

For now, the −1.08% session is the kind of muted move that has framed the year. The stock continues to do what well-managed integrateds do: convert commodity volatility into shareholder return.

Please wait processing your request...

Please wait processing your request...