An equity research deep-dive on Berkshire Hathaway (NYSE:BRK.B), anchored on the April 24, 2026 close. BRK.B at $469.32, P/E 15.12, mkt cap $1.01T. Berkshire's cash mountain & insurance edge make it 2026's top defensive megacap.

Key Highlights

- Berkshire’s valuation remains grounded at ~15x earnings, reflecting stable cash flows and disciplined capital allocation.

- Large cash and Treasury position provides counter-cyclical optionality and interest income support.

- Insurance underwriting and operating businesses continue to deliver steady earnings amid market volatility.

Berkshire Hathaway (NYSE:BRK.B), is a unique conglomerate built around a core of property and casualty insurance (GEICO, Berkshire Hathaway Reinsurance, General Re), a railroad (BNSF), an energy and utilities arm (Berkshire Hathaway Energy), a sprawling collection of wholly owned operating businesses spanning manufacturing, services, and retail, and a publicly traded equity portfolio that is the most-watched institutional book in the world.

By 2026, the strategic frame is well understood. Berkshire is a culturally disciplined, owner-operated capital allocator, structurally biased toward businesses with durable competitive advantages, conservative leverage, and predictable cash flows. The combination of insurance float, operating cash flow, and a substantial cash and short-term Treasury position has made Berkshire one of the most counter-cyclical large-caps in the market — a balance sheet specifically designed to act when others cannot.

Stock Performance in 2026 (YTD)

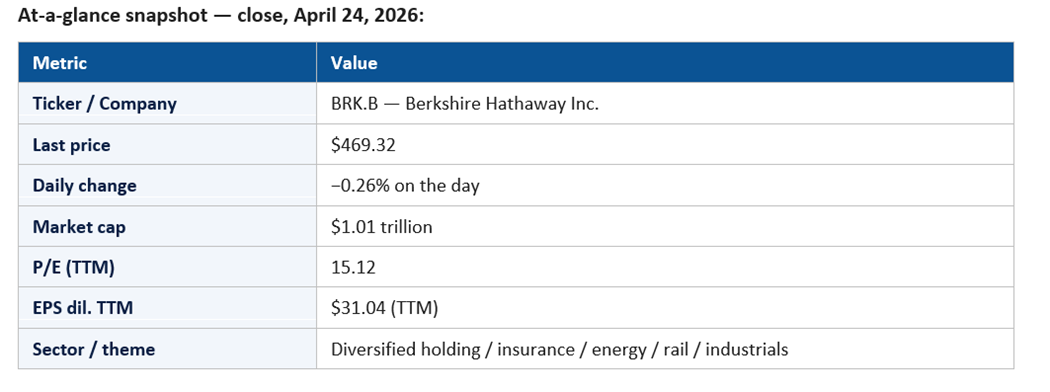

BRK.B closed April 24, 2026 at $469.32, down 0.26% on the day, with a market capitalization of $1.01 trillion. The trailing P/E of 15.12 on $31.04 of TTM EPS is the cleanest valuation in the megacap universe, reflecting a real-earnings business with no AI-narrative premium baked in.

The implied YTD posture is steady-with-defensiveness. Berkshire has functioned as the natural counterweight to the AI-rally regime: on days when the chip complex rallies sharply, BRK.B underperforms mildly; on days when macro nervousness reasserts itself, it outperforms. The −0.26% session sits inside that pattern.

What the YTD shape obscures is the structural story. Berkshire's cash position has continued to be a defining variable, and the patience with which the company has held that cash through an extended bull tape has become one of the most-watched signals in the market.

Key Price Movements and Milestones

Three milestones define the 2026 tape. First, the persistent defense of the trillion-dollar market cap. Second, the equity portfolio rotation: continued trimming of long-held positions and gradual accumulation in defensive names has been the dominant signal in successive 13F filings. Third, the operating-business performance has held up well, with insurance underwriting, BNSF rail volumes, and BHE generation steady through a year of macro chop.

There is also a milestone that has not happened in the way some had feared: a leadership-driven multiple reset. The succession framework — with Greg Abel as the named successor and Ajit Jain continuing to oversee insurance — has been internalized by the market without any disruptive narrative event.

Major Catalysts: Why the Stock Moved

The dominant 2026 catalyst is interest income on the cash and short-term Treasury position. With short-term yields still elevated relative to the prior decade, the implied interest income on Berkshire's cash pile is a meaningful contributor to operating earnings. Each macro print that suggests rates stay higher for longer reinforces this part of the equity story.

The second catalyst is insurance underwriting. GEICO's profitability cycle and the broader P&C reinsurance environment have been net constructive, with hard-market pricing supporting underwriting margin even as catastrophe activity remains a watch item.

The third catalyst is energy. BHE has continued to deploy capital into transmission, generation, and renewables. While the segment generates more controversy among investors than the others, its long-duration cash flows are a structural positive for the consolidated story.

The fourth catalyst is portfolio activity. Each disclosure of new positions or trims at the equity-investment level is treated as a discrete catalyst by sentiment, even when the immediate dollar impact is modest.

Macro and Fed-rate sensitivity is unique. Berkshire benefits from higher short-rates via interest income, but also from lower rates via equity-portfolio mark-to-market. The net effect is one of relative insulation rather than directional sensitivity.

Sector Trends Influencing the Stock

Three sector trends matter for Berkshire's 2026 thesis. First, the insurance market has remained in a hard-pricing phase, supporting underwriting profitability. Second, the rail and freight environment has shown signs of stabilization after a period of softer volumes. Third, the energy and utilities segment is benefiting from the long-duration buildout of grid infrastructure, which is increasingly seen as both an electrification story and an AI-data-center story.

There is also a market-wide trend that affects how investors think about Berkshire: the growing disparity between AI-narrative valuations and traditional businesses. As that gap widens, the case for Berkshire as the defensive counterweight in a barbell strategy strengthens.

Competitive Positioning

Berkshire's competitive position is structural and cultural rather than product-specific. The combination of permanent capital, a long time horizon, and a willingness to act decisively at moments of dislocation gives Berkshire a real advantage over most other capital allocators. The conglomerate's ability to deploy meaningful sums on short notice — at terms that would be unavailable to almost anyone else — is itself a kind of moat.

At the operating-business level, Berkshire's portfolio is competitive but not uniquely dominant. BNSF competes with Union Pacific in U.S. rail; GEICO competes with Progressive and other insurers; BHE competes with regulated and unregulated peers. The strategic edge comes less from any single business and more from the quality of the consolidated capital structure.

Financial Highlights

TTM diluted EPS of $31.04 on a $469.32 share price gives Berkshire a P/E of 15.12. That is the most grounded multiple among the megacaps. Operating earnings (excluding mark-to-market on the equity portfolio) have continued to grow at a measured pace, and the cash position has continued to compound through interest income.

Capital deployment in 2026 has been notably disciplined. Buybacks remain a possible but not aggressive tool. There has been no announcement of a transformative acquisition, and the implicit communication has been that the bar for acting remains high. That patience itself is a financial-strategic asset.

Book value growth — Berkshire's traditional yardstick — has tracked with operating earnings and equity-portfolio dynamics. The relationship between price and book has remained within the band that has historically characterized the stock, with the implication that the market is pricing the franchise rationally rather than aggressively.

Key Risks and Challenges

The first risk is succession. While the framework is in place, the cultural transition from the founders' era to the next generation of leadership is the single most consequential variable in the long-term equity story.

The second risk is concentration in the equity portfolio. A handful of positions represent a disproportionate share of the publicly disclosed book, and any meaningful drawdown in those names would mark Berkshire's stated equity values down at the consolidated level.

The third risk is the cost of patience. In a sustained bull tape, holding a substantial cash position is a real opportunity cost. If the market continues to advance without the kind of dislocation Berkshire is built to exploit, the equity story is one of steady but unspectacular returns.

The fourth risk is sector-specific: insurance loss volatility, rail-volume softness, or energy regulatory headwinds could dent operating earnings even as the consolidated balance sheet remains pristine.

Institutional and Investor Sentiment

Institutional sentiment on Berkshire in 2026 is sober and constructive. Many large allocators carry Berkshire as a defensive core position precisely because of its low correlation with the AI-driven beta of the rest of the index. Sell-side coverage is limited relative to the AI cohort, but where it exists, the bias is modestly bullish.

Retail interest in Berkshire continues to be more cultural than tactical, anchored to the legacy of the company's leadership and the annual meeting cadence. The options market is comparatively thin, reflecting an investor base that views the stock as a long-term hold rather than a trading vehicle.

Signals to Watch in the Coming Quarters

Five concrete signals will define how the Berkshire narrative evolves. The first is the cash and short-term Treasury position. Each quarterly disclosure of the cash pile is treated as a strategic signal: whether the company is accumulating, deploying, or holding pat. Any meaningful drawdown of cash into a transformative acquisition or sustained equity-portfolio build would be a major narrative event.

The second signal is the equity portfolio. The 13F filings continue to be among the most-watched institutional disclosures in the market, with each new position, each meaningful add, and each trim parsed for strategic intent. The longer-arc rotation toward more defensive or income-oriented names has been a multi-year theme; any decisive change in direction would be material.

The third signal is insurance underwriting. Combined ratios at GEICO, Berkshire Hathaway Reinsurance, and the broader insurance segment determine the operating-earnings base on which the rest of the franchise compounds. Catastrophe activity and reinsurance pricing dynamics are the principal external variables.

The fourth signal is BNSF and BHE. Rail volumes, freight rates, and energy-segment regulatory and capital-allocation commentary collectively determine the operating cash-flow cadence outside insurance. Both segments have been steady through 2026; any meaningful deviation in either direction would be noteworthy.

The fifth signal is succession communication. The market has internalized the framework, but each annual letter, each annual meeting, and each operational disclosure that touches on leadership continuity is parsed carefully. There is no expected catalyst here in the conventional sense, but it is the longest-duration risk in the equity story.

Outlook for the Rest of 2026

The base case is continued steady compounding. Operating earnings grow modestly; the cash pile continues to generate meaningful interest income; insurance underwriting holds; portfolio activity remains incremental rather than transformative. In that scenario, the stock grinds higher in line with operating earnings, with the multiple holding in the mid-teens.

The bull case is a market dislocation that Berkshire is uniquely positioned to exploit. A genuine widening of credit spreads or a meaningful equity drawdown would create the kind of opportunity set the cash position was built for, and any visible deployment in such a moment would be a powerful narrative event.

The bear case is a sustained continuation of the high-multiple AI-led tape, in which Berkshire's cash discipline becomes a continued opportunity cost relative to the index.

Berkshire in 2026 is the rare megacap whose biggest competitive advantage is the willingness to do nothing for a long time. In a market that wants spectacle, that is itself a kind of edge.

For now, the −0.26% session is the kind of measured underperformance that defines the year. Berkshire is not designed to win the daily tape. It is designed to be the position you don't worry about while you are watching everything else.

Please wait processing your request...

Please wait processing your request...