Chips, cancer drugs, AR glasses and wound care: INDI, ADCT, VUZI, ORGO, RPAY and LAB dissected with real catalysts and brutally honest risk. One is already profitable. Are the others worth the bet?

OVERVIEW

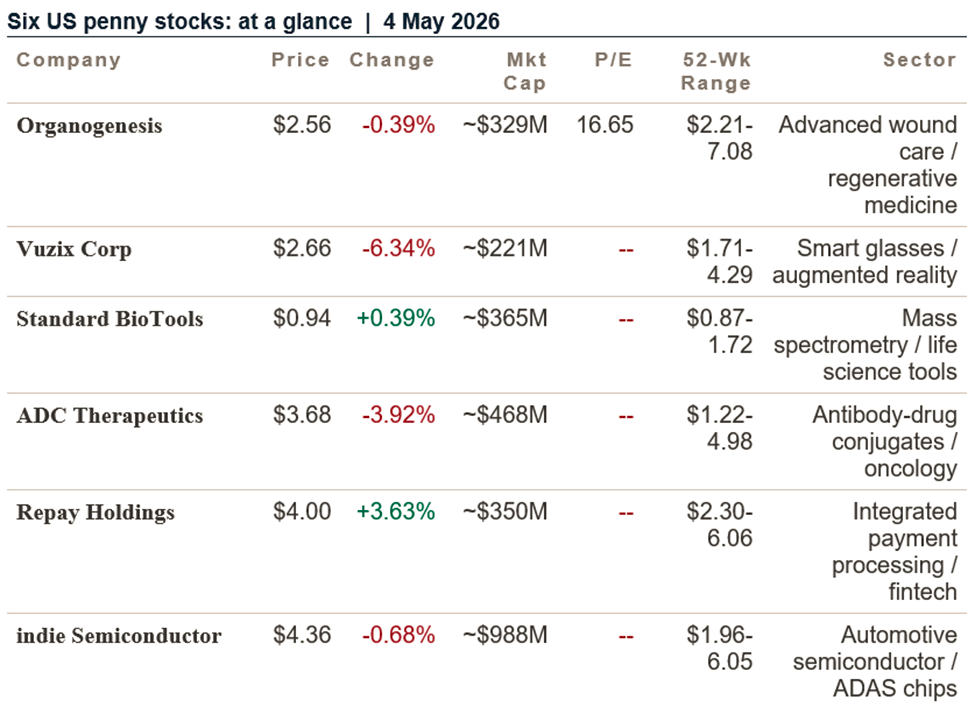

Six under-$5 stocks spanning healthcare, AR, biotech, oncology, fintech and chips

The US penny stock universe contains some of the most innovative companies in American business -- and some of the most speculative. These six NASDAQ and NYSE-listed stocks, all priced between $0.94 and $4.36, span sectors from advanced wound care to augmented reality, from mass spectrometry to antibody-drug conjugates. The range of business models, risk profiles and potential catalysts makes this list one of the most diverse small-cap selections possible.

The conventional definition of a US penny stock -- shares trading below $5 -- encompasses an enormous universe. All six stocks on this list qualify, with prices ranging from Standard BioTools at $0.94 to indie Semiconductor at $4.36. What distinguishes the better penny stock ideas from the rest is not price alone but the combination of: (1) a real, differentiated business model; (2) a specific catalyst that could re-rate the stock; (3) a balance sheet adequate to reach that catalyst; and (4) a management team with a credible execution track record. We assess each of these dimensions for all six companies.

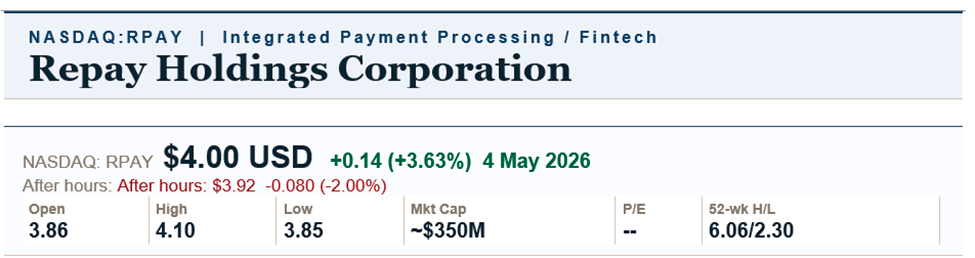

Four of six stocks were down on 4 May 2026 -- VUZI's -6.34 per cent was the largest single-day decline and warrants specific investigation. RPAY's +3.63 per cent was the standout positive mover. All six lack conventional dividends, consistent with their growth or restructuring phases. Only ORGO carries a positive P/E (16.65), while the others show '--' reflecting current-period losses or pre-earnings status.

Source: EODHD, 4 May 2026.

|

|

Business Analysis |

What Organogenesis does: Organogenesis Holdings Inc. is a commercial-stage regenerative medicine company focused on the development, manufacture and commercialisation of wound care and surgical biologics products. The company's portfolio includes advanced wound care products that promote healing in chronic wounds (diabetic foot ulcers, venous leg ulcers, pressure wounds), surgical reconstruction products, and periodontal disease treatments. Organogenesis sells primarily to hospitals, wound care centres, and outpatient clinics across the United States. [ORGO Annual Report 2024 / 10-K, SEC]

Key products: Organogenesis's commercial portfolio includes Apligraf (a living bilayered cell therapy for venous leg and diabetic foot ulcers -- one of the first FDA-approved living cell therapies), Dermagraft (a human fibroblast-derived dermal substitute for diabetic foot ulcers), and PuraPly AM (an antimicrobial collagen matrix wound dressing). These products represent different technology approaches to wound healing -- from living cell therapies to bioengineered tissue matrices to antimicrobial barriers.

The wound care market: Chronic wound management is one of the fastest-growing segments of US healthcare, driven by the rising prevalence of diabetes (a primary cause of chronic wounds), an ageing population, and obesity. The Centers for Disease Control estimates over 34 million Americans live with diabetes, with approximately 15 per cent developing a diabetic foot ulcer during their lifetime. Each diabetic foot ulcer episode represents significant healthcare cost, and advanced wound care products that accelerate healing generate measurable clinical and economic value.

The only profitable P/E on the list: Organogenesis carries a positive P/E ratio of 16.65 -- the only company among the six to do so. This reflects a return to profitability following a period of restructuring and cost reduction. The profitable P/E at a $2.56 share price represents an earnings yield of approximately 6 per cent -- a meaningful number for a small-cap healthcare company with a differentiated product portfolio in a structurally growing market.

|

|

Financial Analysis |

Organogenesis's path to profitability reflects a combination of revenue growth from its commercial wound care portfolio and a significant restructuring programme that reduced the company's cost base. The P/E of 16.65 on a $2.56 share price implies trailing earnings per share of approximately $0.15. For a company in a growing healthcare niche with FDA-cleared products and an established commercial infrastructure, this earnings multiple is modest.

The company's revenue is generated from product sales to US healthcare facilities, with a mix of Medicare, Medicaid and commercial insurance reimbursement. Reimbursement policy changes by US government healthcare programmes (CMS) have historically been a material driver of Organogenesis's revenue -- changes to Medicare coverage policies for advanced wound care products have periodically expanded or contracted the addressable market.

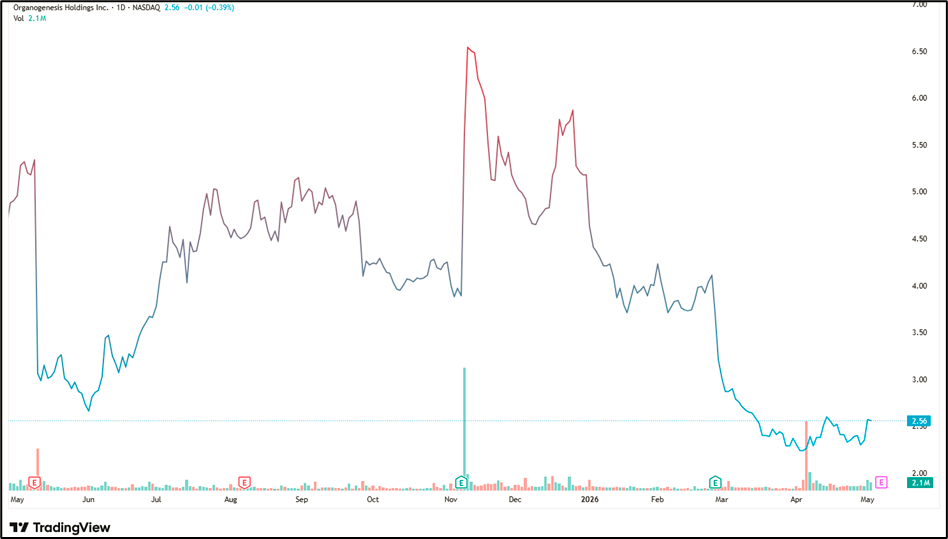

The 52-week range of $2.21 to $7.08 -- with the current $2.56 near the low end -- reflects significant share price pressure in the past year. Investors should investigate whether the decline from $7.08 reflects a fundamental business deterioration (CMS reimbursement changes, competition, revenue shortfall) or a broader small-cap healthcare sector re-rating.

|

|

Catalyst and Outlook |

The primary catalysts for Organogenesis are: US Medicare reimbursement policy updates for advanced wound care biologics (any favourable CMS policy change is a significant positive); continued commercialisation of the existing portfolio to wound care specialists and hospitals; and potential new product launches or line extensions. The wound care market's structural growth -- driven by diabetes, ageing and obesity -- provides a durable demand backdrop.

Key risks: CMS reimbursement risk is the dominant business risk -- the company's revenue is highly sensitive to Medicare coverage and reimbursement rates for advanced wound care products. Competition from other wound care biologics and conventional dressings. Execution risk in maintaining profitability while growing revenue. The 52-week high of $7.08 versus current $2.56 suggests the market has significantly downgraded expectations -- understanding why is critical before investing.

|

|

FAQs -- Organogenesis |

Q: What does Organogenesis make?

A: Advanced wound care biologics -- living cell therapies (Apligraf, Dermagraft), collagen matrices and other bioengineered products that promote healing in chronic wounds such as diabetic foot ulcers and venous leg ulcers. Sold to US hospitals and wound care centres.

Q: Why is ORGO the only stock with a positive P/E?

A: Organogenesis has returned to profitability following restructuring. The P/E of 16.65 implies trailing EPS of approximately $0.15. The other five stocks are pre-earnings or loss-making.

Q: What is the biggest risk for ORGO?

A: CMS (US Medicare/Medicaid) reimbursement policy. Advanced wound care biologics are expensive; if CMS restricts coverage or cuts reimbursement rates, Organogenesis's revenue falls directly.

|

|

Business Analysis |

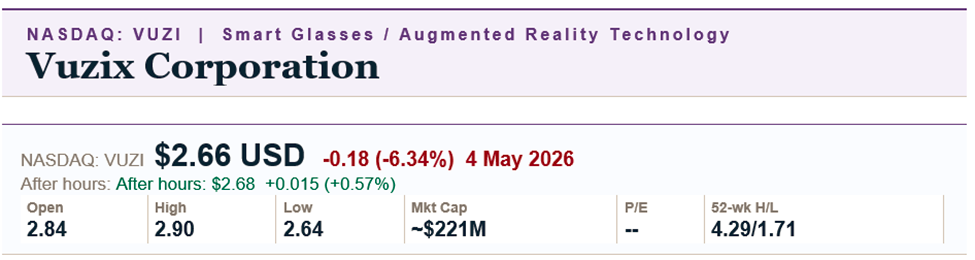

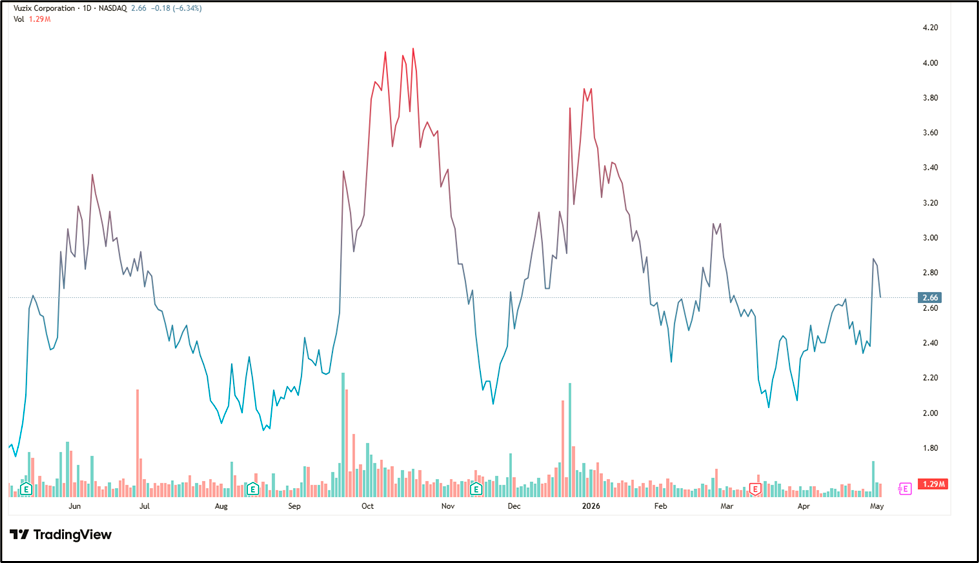

What Vuzix does: Vuzix Corporation is a US manufacturer of smart glasses and augmented reality (AR) technology, primarily selling enterprise-grade wearable AR devices. The company's products allow workers in logistics, manufacturing, field service, healthcare and other industries to access digital information -- instructions, schematics, video calls, AI assistance -- hands-free while performing physical tasks. Vuzix's commercial products include the M400 and M4000 smart glasses ranges, designed for industrial and enterprise deployment.

The enterprise AR market: Industrial augmented reality -- AR glasses enabling workers to see digital overlays on the physical world -- is one of the most promising but slower-to-develop technology markets of the past decade. The promise is clear: a warehouse picker or field technician who can see pick lists, technical diagrams or remote expert guidance overlaid on their field of view is faster, more accurate and more efficient than one who must reference a tablet or manual. The challenge is product robustness, battery life, comfort and enterprise IT integration.

OEM partnerships and licensing: Beyond its own branded products, Vuzix pursues OEM and licensing partnerships with larger technology companies who want to integrate Vuzix's optics and waveguide technology into their own products. These partnerships -- with undisclosed and disclosed partners -- have been a key strategic differentiator, as they provide revenue streams that do not depend solely on Vuzix's own commercial sales execution. Any significant OEM partnership announcement is a major stock catalyst.

Waveguide technology: Vuzix has developed proprietary waveguide optical technology that is central to miniaturised AR displays. Waveguides allow light to be guided along a thin, transparent substrate to create AR overlays visible to the wearer without the bulk of traditional optics. This technology has applications beyond Vuzix's own products -- in consumer AR glasses (the market that Apple, Meta and Google are pursuing), Vuzix's waveguide manufacturing capability may be licensed or OEM-supplied to major technology companies.

|

|

Financial Analysis |

Vuzix is a pre-profitability technology company. Revenue is generated from product sales (enterprise smart glasses) and technology licensing. The P/E of '--' (not available) reflects ongoing operating losses as the company invests in product development, sales and distribution ahead of the scale inflection that would make it profitable. Vuzix has historically required periodic equity raises to fund operations, creating dilution risk for existing shareholders.

The 52-week range of $1.71 to $4.29 for a stock at $2.66 shows the typical volatility profile of a small-cap technology company whose valuation is driven by sentiment around AR technology adoption. The market cap of approximately $221 million implies a modest revenue multiple for a company with genuine proprietary technology -- but the multiple is constrained by current losses and the timeline to profitable scale.

|

|

Catalyst and Outlook |

The primary catalyst for Vuzix is a major OEM or technology partnership announcement -- particularly with a Tier 1 technology company (Apple, Google, Microsoft, Meta or similar) for waveguide supply or technology licensing. Enterprise AR adoption growth from existing customers is the organic growth driver. Any announcement of a significant contract win in healthcare, logistics or defence would also be material.

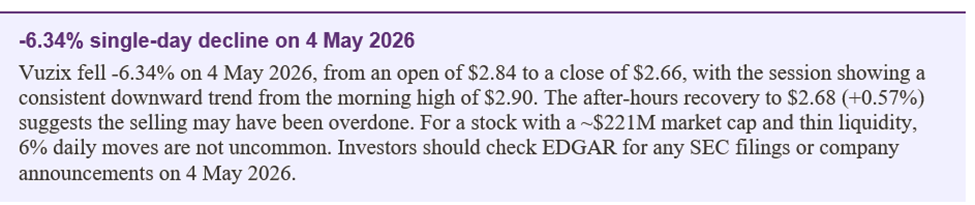

Key risks: Execution risk in competing with well-funded players like Microsoft HoloLens and Meta Quest Pro in enterprise AR. Dilution risk from equity raises needed to fund operations. Slower-than-expected enterprise AR adoption. OEM partnership dependency -- if an anticipated partnership does not materialise or is delayed, the stock can fall sharply. The -6.34% day move illustrates this binary news sensitivity.

|

|

FAQs -- Vuzix |

Q: What does Vuzix make?

A: Enterprise smart glasses and augmented reality hardware -- wearable computers that overlay digital information on the user's field of view. Sold to logistics, manufacturing, field service and healthcare customers.

Q: Why is Vuzix not profitable?

A: The company is in a growth investment phase -- spending on R&D, product development and sales ahead of the revenue scale needed for profitability. This is common for early-stage technology companies.

Q: What is waveguide technology?

A: A proprietary optical technology that guides light along a thin transparent substrate to create AR displays. Vuzix's waveguide IP could be licensed to major consumer AR companies (Apple, Google, Meta), which would be a transformative revenue event.

|

|

Business Analysis |

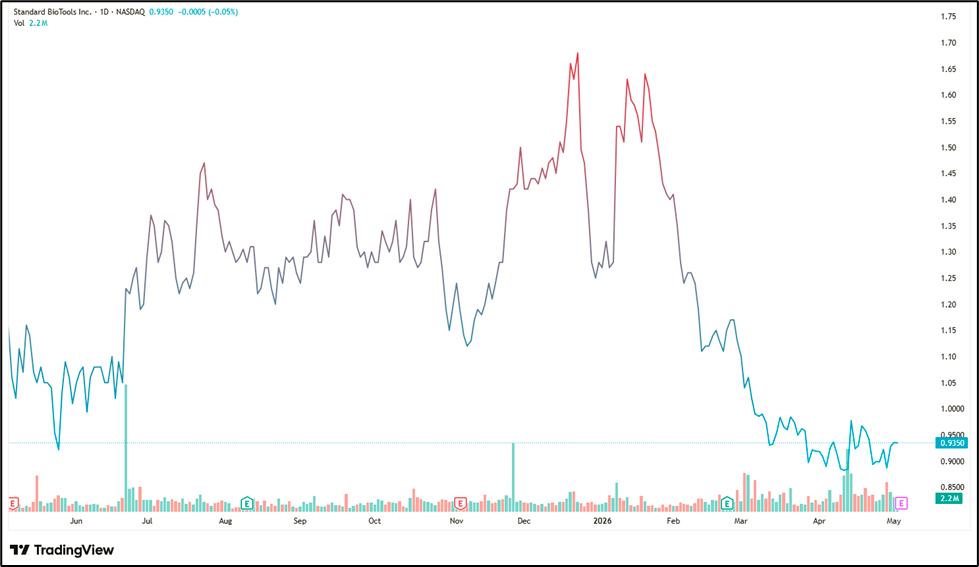

What Standard BioTools does: Standard BioTools Inc. (formerly Fluidigm) is a life science instruments company providing mass cytometry (CyTOF) and microfluidics platforms for single-cell biological analysis. The company's instruments allow researchers to simultaneously measure dozens of proteins in individual cells -- enabling unprecedented resolution in understanding cell biology, immunology, cancer and drug mechanism of action. Its platforms are used by pharmaceutical companies, academic research institutions and government laboratories globally.

CyTOF technology -- mass cytometry: CyTOF (Cytometry by Time of Flight) is Standard BioTools' flagship technology platform. Unlike conventional flow cytometry (which uses fluorescent markers with limited parameter count), CyTOF uses heavy metal isotope tags detected by mass spectrometry, allowing simultaneous measurement of 40-50+ protein markers per cell. This multiplexing capability enables researchers to study complex biological systems -- cancer immunology, immunotherapy response, stem cell biology -- with far greater depth than conventional techniques.

SomaScan proteomics platform: Standard BioTools acquired SomaLogic in 2023, adding the SomaScan platform -- a high-throughput proteomics service that can measure more than 7,000 proteins in a single blood sample. SomaScan has applications in drug discovery, biomarker identification and personalised medicine. The combined Standard BioTools / SomaLogic entity provides a broader multi-omic analysis capability than either company could deliver alone.

Transition and restructuring: Standard BioTools has been in an extended restructuring and business transformation phase, simplifying its product portfolio, reducing costs and focusing on the highest-value applications of its platforms. The company has narrowed its focus to the segments where its technology provides the clearest value: precision medicine research, immunology and oncology. This focus is reflected in the company's new name -- 'Standard BioTools' conveys the aspiration to provide standardised, routine biological measurement tools.

|

|

Financial Analysis |

Standard BioTools is currently loss-making -- the '--' P/E reflects this. At $0.94, the stock sits just above its 52-week low of $0.87 and well below the $1.72 52-week high. At approximately $365 million market cap, the stock is valued modestly relative to its combined instrument install base and the SomaScan proteomics franchise. The SomaScan platform in particular -- with its ability to measure 7,000+ proteins per sample -- has substantial potential value in the rapidly growing proteomics market.

The primary financial risk is the cash burn associated with the restructuring and integration of SomaLogic. Standard BioTools must demonstrate a clear path to EBITDA break-even or positive operating cash flow for the stock to re-rate materially. At $0.94, any positive revenue growth and cost improvement showing would represent a meaningful catalyst.

|

|

Catalyst and Outlook |

Key catalysts include: evidence of SomaScan commercial adoption beyond academic research (pharmaceutical company partnerships for drug development proteomics); progress on cost reduction to a cash-flow-neutral position; and any partnership or licensing agreement for CyTOF technology in clinical diagnostics (applying mass cytometry to routine clinical testing is a large potential market). The $0.87 52-week low provides a context for downside; the $1.72 high shows the stock can double on positive newsflow.

Key risks: Technology adoption pace -- mass cytometry and high-dimensional proteomics remain specialist research tools not yet routine in clinical settings, limiting market size. Integration risk from the SomaLogic acquisition. Cash burn and potential need for equity raise at a dilutive price. Competition from larger life science instrument companies (Thermo Fisher, Beckman Coulter) expanding into high-parameter cytometry.

|

|

FAQs -- Standard BioTools |

Q: What is CyTOF technology?

A: Mass cytometry -- using metal isotope tags rather than fluorescent markers to measure 40-50+ proteins per cell simultaneously. Standard BioTools' CyTOF instruments are used in cancer immunology, immunotherapy and stem cell research.

Q: What is SomaScan?

A: A proteomics service platform measuring 7,000+ proteins in a single blood sample. Acquired from SomaLogic in 2023. Applications in drug discovery, biomarker identification and personalised medicine.

Q: Why is LAB priced below $1?

A: Standard BioTools is loss-making and in a restructuring phase post-SomaLogic acquisition. At $0.94 with a $0.87 52-week low, the stock is near exchange minimum price thresholds -- investors should note that NASDAQ requires stocks to maintain a minimum $1.00 bid price or face delisting proceedings.

|

|

Business Analysis |

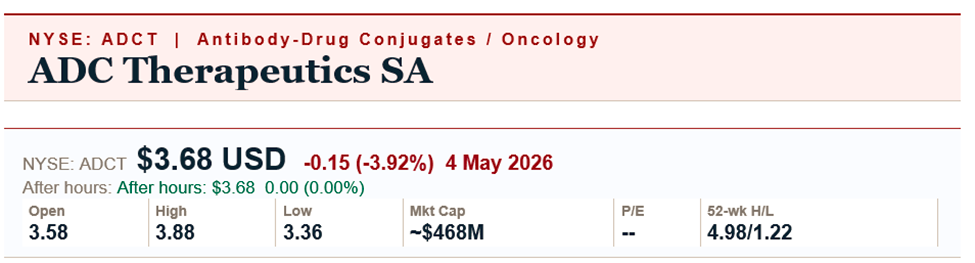

What ADC Therapeutics does: ADC Therapeutics SA is a Swiss-American commercial-stage oncology company focused on antibody-drug conjugates (ADCs) -- a class of cancer therapies that combine a tumour-targeting antibody with a cytotoxic payload, designed to deliver chemotherapy directly to cancer cells while sparing healthy tissue. The company's lead commercial product, Zynlonta (loncastuximab tesirine), is approved by the US FDA for the treatment of relapsed or refractory diffuse large B-cell lymphoma (DLBCL) in adults who have received at least two prior lines of therapy.

Zynlonta -- the commercial product: Zynlonta was approved by the FDA in April 2021 and represents a significant clinical advance for heavily pre-treated DLBCL patients. DLBCL is the most common aggressive lymphoma, and patients who progress after standard therapy have limited options. Zynlonta's mechanism -- targeting CD19 on B-cell lymphomas and delivering a DNA-damaging pyrrolobenzodiazepine (PBD) payload -- provides a different mechanism of action from other approved therapies, making it complementary to existing treatment algorithms.

ADC technology platform: Beyond Zynlonta, ADC Therapeutics has a pipeline of ADC candidates in development, applying its PBD dimer payload technology to additional haematological malignancies and potentially solid tumours. The ADC drug class has emerged as one of the most important new cancer treatment modalities -- multiple ADCs have received FDA approval in recent years, including Enhertu (trastuzumab deruxtecan) which has become one of oncology's most commercially significant new drugs.

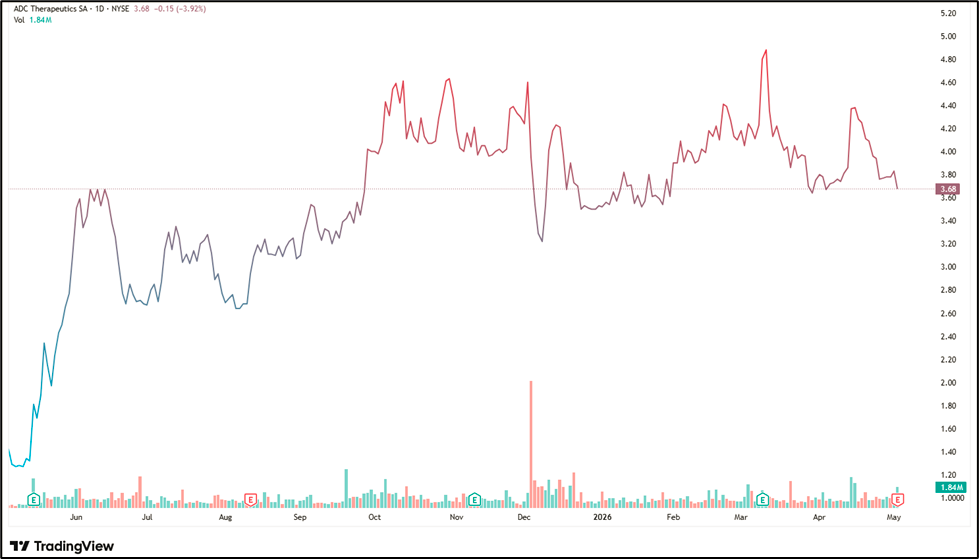

Commercialisation challenges: Despite the clinical promise of Zynlonta, the company has faced significant commercialisation challenges -- particularly in building market share against more established DLBCL therapies and navigating the competitive dynamics of a market rapidly changing with the approval of CAR-T cell therapies and bispecific antibodies. The revenue ramp has been slower than initial projections, contributing to the significant share price decline from highs.

|

|

Financial Analysis |

ADC Therapeutics is pre-profitability -- the '--' P/E reflects ongoing losses as the company funds Zynlonta's commercialisation and pipeline development. The company's financial sustainability depends on growing Zynlonta revenues to a level that covers commercialisation and R&D costs. Any partnership or licensing of the ADC platform technology -- particularly to a larger pharmaceutical company -- could provide non-dilutive capital and validate the technology.

The 52-week range of $1.22 to $4.98 for a stock at $3.68 shows significant recovery from the lows -- the stock has tripled from its 52-week low. The current $3.68 near the midpoint of the range reflects a company that has stabilised but not yet demonstrated the commercial execution needed to approach its 52-week high. The intraday volatility on 4 May 2026 (open $3.58, high $3.88, low $3.36) reflects the high-beta nature of clinical-stage oncology stocks.

|

|

Catalyst and Outlook |

Key catalysts include: Zynlonta revenue growth acceleration (capturing market share in later-line DLBCL and potentially earlier-line combinations); pipeline clinical data readouts (particularly data from combination studies or new indications); and any partnership, licensing or acquisition approach from a larger oncology company. The ADC sector has seen significant M&A activity -- major pharmaceutical companies have paid substantial premiums for ADC assets and platforms.

Key risks: Zynlonta commercial adoption may continue to disappoint if competition from CAR-T therapies and bispecifics captures the heavily pre-treated DLBCL market. Cash burn and potential need for equity raise. Pipeline clinical failure risk. Regulatory risk for label expansions. The -3.92% day decline on 4 May 2026 reflects the ongoing investor uncertainty about commercial execution.

|

|

FAQs -- ADC Therapeutics |

Q: What are antibody-drug conjugates (ADCs)?

A: Cancer drugs that combine a tumour-targeting antibody with a chemotherapy payload, designed to deliver treatment directly to cancer cells while minimising side effects on healthy tissue. ADCs are one of oncology's most important new drug classes.

Q: What is Zynlonta?

A: ADC Therapeutics' FDA-approved cancer drug for adults with relapsed/refractory diffuse large B-cell lymphoma (DLBCL) who have received at least two prior therapies. The first PBD-based ADC to reach the market.

Q: Why might a larger pharma company acquire ADCT?

A: ADC is the hottest drug class in oncology. Major pharma companies have paid multi-billion dollar premiums for ADC platforms. ADC Therapeutics' PBD technology, Zynlonta data, and pipeline could attract strategic interest.

|

|

Business Analysis |

What Repay Holdings does: Repay Holdings Corporation is a US payment technology company providing integrated payment processing solutions to specialised lending and financial services vertical markets. The company's core business is enabling lenders -- consumer finance, auto dealers, mortgage servicers, personal loan providers and business lenders -- to accept loan repayments through multiple channels (debit card, ACH, digital wallet) via an integrated software and payments platform.

Vertical market focus: Repay's strategic differentiation is its focus on specialised lending verticals rather than competing with Stripe or Square in the broad merchant payments market. Consumer finance lenders (personal loan companies, installement lenders, credit unions) have specific repayment processing needs -- they need to accept scheduled loan payments from borrowers, not retail point-of-sale transactions. Repay's platform is purpose-built for this repayment use case, providing software integrations with lending management systems that general-purpose payment processors do not offer.

Business and consumer payments: Repay also serves business-to-business payment needs, enabling companies to pay suppliers via card and ACH. This B2B payments segment has been a growth area as businesses seek to extend payment terms and capture card rewards on supplier payments. The combination of consumer loan repayment processing and B2B supplier payment processing provides two distinct growth vectors within the integrated payment market.

Technology integrations: Repay's competitive moat lies in its deep software integrations with loan origination and servicing platforms. When a lending software platform integrates Repay's payment processing, lenders can offer borrowers seamless payment experiences without leaving their primary software environment. These integrations create switching costs -- replacing the embedded payment provider requires migrating the entire payments workflow, which lenders are reluctant to do.

|

|

Financial Analysis |

Repay is a high-revenue but currently pre-GAAP-profit payments company. The '--' P/E reflects GAAP losses driven primarily by non-cash charges (amortisation of intangibles from acquisitions, stock-based compensation). On an adjusted EBITDA basis, Repay is profitable -- the company generates positive operating cash flow. The GAAP versus adjusted earnings discrepancy is common in payment technology companies that have grown through acquisitions.

The +3.63 per cent positive close on 4 May 2026 (the strongest performer of the six on this date) suggests positive newsflow or sentiment. The after-hours pullback to $3.92 (-2.00%) partially reverses the day's gain. The 52-week range of $2.30 to $6.06 shows the stock has recovered significantly from its lows. At $4.00, it is in the upper half of the 52-week range.

Payment processing companies are typically valued on revenue multiples and adjusted EBITDA multiples rather than GAAP earnings. At approximately $350M market cap and the revenue levels reported in recent filings, Repay trades at a modest multiple relative to payment technology peers -- reflecting the micro-cap scale, lower growth rate than high-profile payments companies, and the GAAP loss position.

|

|

Catalyst and Outlook |

Key catalysts include: acceleration in payment volume growth as the US consumer lending market recovers; new vertical market expansions (healthcare payments, government payments); strategic partnership announcements with major lending software platforms; and any M&A approach from a larger payment processor (the payments industry has been consolidating rapidly). The +3.63% day move may reflect one of these catalysts.

Key risks: US consumer lending market conditions -- if personal loan originations decline in an economic slowdown, Repay's payment volumes fall with them. Competition from larger payment processors (FIS, Fiserv, PayPal) entering the vertical lending market. Acquisition integration risk. The GAAP loss position creates earnings uncertainty for investors applying conventional valuation frameworks.

|

|

FAQs -- Repay Holdings |

Q: What payments does Repay process?

A: Primarily loan repayments -- enabling borrowers to repay personal loans, auto loans, mortgage servicer payments and other consumer finance products via debit card, ACH and digital wallet. Also B2B supplier payments.

Q: Why is RPAY profitable on adjusted EBITDA but not on GAAP?

A: GAAP losses are driven by non-cash charges: amortisation of intangible assets from acquisitions and stock-based compensation. Adjusted EBITDA strips these out to show the cash-generating nature of the core business.

Q: What drove the +3.63% move on 4 May 2026?

A: The specific reason is not confirmed in the source data. Check EDGAR for any SEC filings or company announcements on 4 May 2026 that may explain the positive move. The after-hours decline suggests some of the intraday enthusiasm was not sustained.

|

|

Business Analysis |

What indie Semiconductor does: indie Semiconductor Inc. is a US fabless semiconductor company designing chips and software for the automotive market, with a focus on advanced driver assistance systems (ADAS), autonomous driving, in-cabin user experience and electrification (EV powertrains and charging). The company's products include LiDAR SoCs (system-on-chips for light detection and ranging sensors), radar processor chips, in-cabin sensing SoCs for driver and occupant monitoring, and EV charging and battery management semiconductor solutions.

The automotive semiconductor market: Modern vehicles contain increasingly complex electronics -- advanced safety systems (automatic emergency braking, lane keeping, adaptive cruise control), connected infotainment, electrified powertrains and over-the-air software update capability all require specialised semiconductor content. The average semiconductor content per vehicle has been rising at double-digit rates annually, and the shift to electric vehicles further increases chip content per car. Automotive-grade chips must meet more demanding reliability, temperature and certification requirements than consumer electronics -- creating a barrier to entry for new suppliers.

ADAS and autonomous driving focus: indie's primary focus is the sensor processing chips that underpin ADAS features. LiDAR, radar and camera sensors generate enormous amounts of data that must be processed in real time to identify pedestrians, other vehicles, lane markings and road hazards. indie's SoCs perform this sensor fusion processing at automotive-grade specifications. As ADAS features become standard across mid-range and economy vehicles (not just luxury cars), the total addressable market for ADAS chips expands dramatically.

Acquisitions and platform build-out: indie has grown through a series of acquisitions of smaller automotive semiconductor companies, assembling a multi-function automotive chip platform that covers LiDAR sensing, radar, in-cabin monitoring and EV charging. This platform approach -- where indie can supply multiple chips to the same car programme -- differentiates it from single-product competitors and increases revenue per vehicle.

|

|

Financial Analysis |

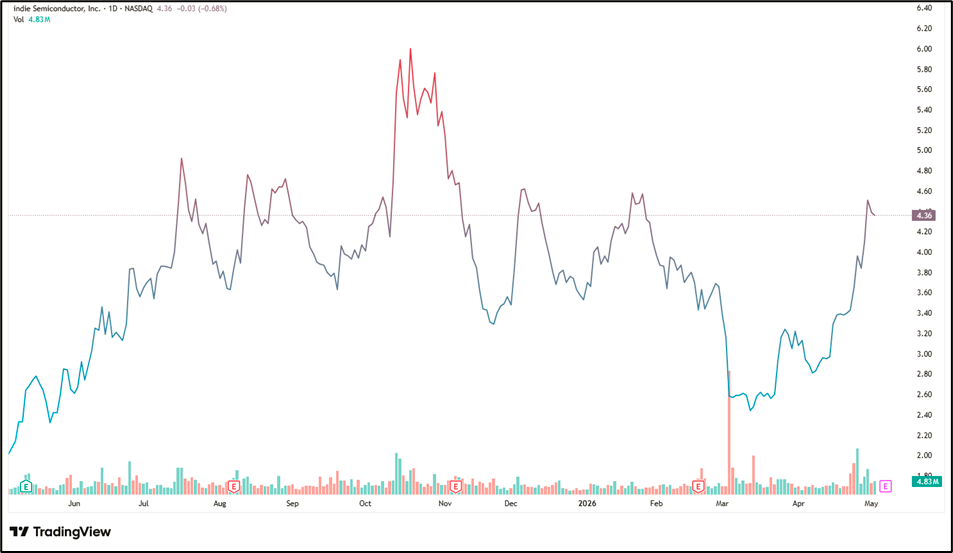

indie Semiconductor is the largest-cap company on this list at approximately $988 million -- nearly at the conventional $1 billion small/mid-cap threshold. The '--' P/E reflects operating losses as the company invests in automotive chip development, qualification (automotive chips require 12-18 months of reliability testing and certification before production shipment) and production ramp-up. Revenue has been growing as design wins convert into production shipments.

The 52-week range of $1.96 to $6.05 for a stock at $4.36 shows indie has more than doubled from its 52-week low, reflecting recovery in automotive semiconductor sentiment and company-specific design win momentum. The modest -0.68% decline on 4 May 2026 with an after-hours recovery of +0.46% is relatively stable for a small-cap semiconductor stock.

At ~$988M market cap, indie is approaching the market cap level where it begins to attract meaningful institutional coverage and investment. Growth-oriented semiconductor investors may be accumulating the stock in anticipation of a profitability inflection as production volumes scale.

|

|

Catalyst and Outlook |

Key catalysts include: design win announcements with major OEMs (a single Tier 1 automotive platform programme can be worth hundreds of millions in chip revenue over its life cycle); progress toward adjusted EBITDA break-even as revenue scales; LiDAR market share gains as vehicle manufacturers adopt LiDAR for higher ADAS levels; and EV-related chip design wins as electrification ramps. The automotive semiconductor market tailwind is structural and long-duration.

Key risks: Automotive production volume risk -- a global auto market slowdown reduces chip demand with a lag as inventory normalises. Customer programme risk -- automotive chip companies are highly dependent on winning specific OEM programmes; losing or being displaced from a programme is a significant revenue event. EV adoption pace uncertainty -- slower EV ramp-up delays indie's electrification chip revenue. Fabless model risk -- dependency on TSMC and other foundries for manufacturing. Cash burn while the revenue profile scales to profitability.

|

|

FAQs -- indie Semiconductor |

Q: What chips does indie Semiconductor make?

A: Chips for automotive ADAS (LiDAR, radar, camera processing), in-cabin sensing (driver and occupant monitoring), and EV electrification (battery management, charging). Sold to Tier 1 automotive suppliers and OEMs.

Q: What is a LiDAR SoC?

A: A system-on-chip that processes data from LiDAR (Light Detection and Ranging) sensors used in autonomous driving and ADAS systems. LiDAR uses laser pulses to build a 3D map of the environment. indie's SoCs perform the signal processing required to interpret this data in real time.

Q: Why is indie Semiconductor near $1B market cap but still classified as a penny stock?

A: At $4.36/share and ~$988M market cap, indie is technically a penny stock by the sub-$5 price definition, but is functionally a small-cap company approaching the institutional investor threshold. It is the most 'established' company on this list -- higher revenue, more design wins, closer to profitability than several others.

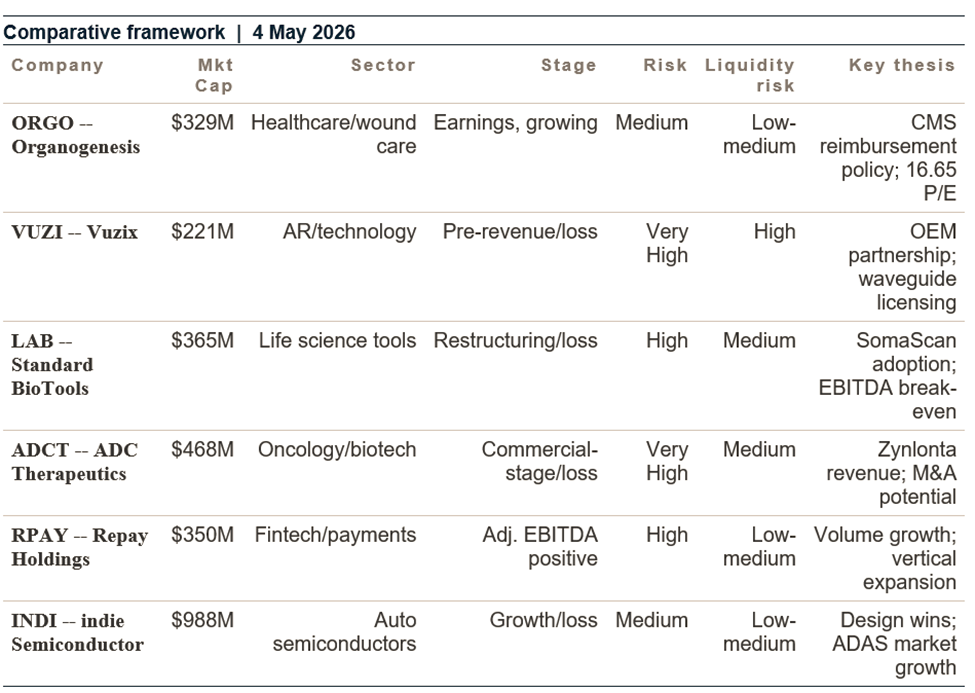

COMPARATIVE ANALYSIS

Six stocks compared: matching risk profile to investment objective

The six stocks span a wide range of sectors, development stages and risk profiles. Understanding where each sits on the risk-reward spectrum is essential before committing capital.

For the only profitable pick: Organogenesis (ORGO) at P/E 16.65 is the sole earnings-positive company. For investors who want small-cap healthcare exposure with current-period profits and a clear commercial model, ORGO is the natural starting point.

For the highest-conviction growth technology bet: indie Semiconductor (INDI) at ~$988M is the highest-quality business on the list -- a fabless automotive chip company with genuine OEM design wins, a structural market tailwind (ADAS, electrification) and the largest market cap providing the most institutional-grade investment profile of the six.

For the speculative high-upside play: Vuzix (VUZI) offers the highest potential upside if a major OEM waveguide deal materialises -- and the highest downside if it does not. ADC Therapeutics (ADCT) similarly offers binary M&A optionality in the hottest drug class in oncology. Both are high-risk, high-reward positions for investors with specific conviction about the catalyst.

For fintech exposure: Repay Holdings (RPAY) provides access to vertical market payment processing with an adjusted EBITDA-positive business model and specific vertical market expertise that creates switching costs. The +3.63% day move on 4 May 2026 may indicate positive news flow.

For the deepest-value turnaround: Standard BioTools (LAB) at $0.94 -- near its 52-week low and below the NASDAQ $1.00 minimum bid threshold -- represents either a deep-value turnaround (if SomaScan and CyTOF find commercial traction) or a value trap. This is the highest-conviction research requirement of the six: investors must understand the SomaScan commercial pipeline and the company's liquidity runway before entering at this level.

Please wait processing your request...

Please wait processing your request...