Geography still determines where leverage originates. Geoeconomics determines how it is exercised. An analysis of the structural shift reshaping supply chains, monetary policy, and investment risk in 2026.

Key Highlights

- Economic statecraft including sanctions, export controls, and supply chain leverage has replaced military force as the primary tool of geopolitical competition.

- The Strait of Hormuz crisis moved global markets, repriced sovereign bonds, and constrained monetary policy within days.

- Semiconductor and rare earth controls have fractured a $975B industry along political rather than commercial lines.

- The IMF now projects 3.1% growth and 4.4% inflation, a stagflationary trap that neutralises conventional policy responses.

- The shift from efficiency to resilience is permanent, embedding structurally higher costs into the global economy.

- Geopolitical alignment is now a capital allocation variable and investment frameworks that treat it as noise are obsolete

Introduction: A Shift in How Power Is Exercised

The relationship between geography and economic power has never been static. At Bretton Woods in 1944, the United States translated its geographic and industrial dominance into a dollar-anchored financial architecture that governed global trade for three decades. When that system strained in 1971, the response was monetary, not military. The 1973 oil embargo then demonstrated, for the first time at scale, that geographic control over a resource corridor could be weaponised as direct economic leverage, triggering inflation, recession, and a fundamental repricing of energy dependence across the developed world. The lesson was noted but not institutionalised. The globalisation era that followed treated geography as a logistical input rather than a strategic variable. Supply chains stretched across jurisdictions optimised for cost. Capital flowed to highest returns regardless of political context. Efficiency was the organising principle.

Source: Kalkine

That assumption is now structurally broken. The dominant tools of strategic competition in 2026 are not tanks or treaties. They are sanctions regimes, export control lists, industrial subsidies, currency settlement architecture, and the selective restriction of supply chain access. The shift did not begin with the current crisis. Western sanctions against Russia in 2014 demonstrated financial exclusion as a primary policy instrument. US semiconductor export controls from 2018 established technology access as a strategic variable. The 2022 freezing of Russian sovereign reserves revealed that the dollar-based financial architecture itself could be weaponised, a signal absorbed by every sovereign wealth manager in the world. What is unfolding in 2026 is the maturation of a transition building across four decades, now operating at full intensity.

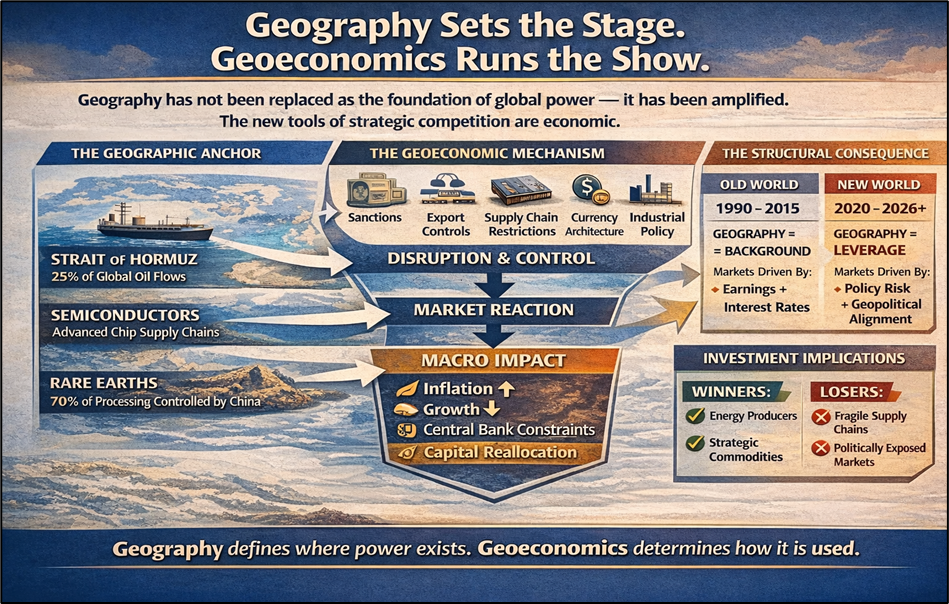

Geography has not become irrelevant. It has become the foundation on which geoeconomic leverage is constructed. The Strait of Hormuz, semiconductor supply chains, critical mineral flows, and global capital architecture each illuminate a different dimension of that transition, and together, they define the central analytical challenge facing macro investors today.

The Hormuz Proof Point: Geography Weaponised Through Economics

The Strait of Hormuz is 33 kilometres wide at its narrowest point. It carries 25% of the world's seaborne oil trade, 20% of global LNG, and roughly 30% of internationally traded fertilisers. Its geographic significance is not new. What the 2026 crisis clarified is that its strategic value was never primarily military; it was always economic. When the strait was disrupted in late February 2026, Brent crude surged to $126 per barrel, war-risk insurance premiums surged fivefold, QatarEnergy declared force majeure on LNG contracts, and the IMF revised global growth down to 3.1% while lifting inflation to 4.4%. The parallels to 1973 are structural: then as now, a geographic chokepoint generated macro consequences far exceeding its physical dimensions. The difference is speed. In 1973, transmission took months; in 2026, it took days, because financial markets now price geographic risk in real time rather than waiting for physical shortages to materialise.

The critical observation is not that the strait was militarily contested. It is that contesting it moved equity markets, repriced sovereign bonds, altered monetary policy expectations, and restructured institutional portfolio exposures across every asset class. The geographic feature generated economic consequences. The economic consequences became the strategic objective. That is the geoeconomic model in its clearest form: geography defines the pressure point, economics determines the outcome.

Nor does the strait need to be closed to generate maximum leverage. Controlled ambiguity, through partial disruption, intermittent enforcement, and deliberate uncertainty, sustains the oil price premium and keeps insurance markets priced for risk. Markets react faster than militaries. Financial transmission precedes physical escalation. That asymmetry is the mechanism through which geographic leverage now operates.

The Technology and Resource Dimensions: Export Controls and Critical Minerals

Export Controls and Critical Minerals Energy chokepoints are the most visible expression of geoeconomic statecraft. They are not the most structurally consequential one.

The semiconductor industry illustrates how geoeconomics operates at the technology layer. The global market is projected to reach $975 billion in 2026, a historic peak driven by AI infrastructure demand, yet beneath that figure lies a fragmentation driven by geopolitical logic rather than commercial efficiency. Since 2018, US export controls on advanced chips directed at China have progressively tightened, culminating in the January 2025 AI Diffusion Rule that divided the world into preferred, regulated, and restricted jurisdictions. Capital allocation has followed. China accelerated state-backed investment in domestic semiconductor manufacturing, while in late 2025 the Dutch government split Nexperia into separate Chinese and Dutch entities, a geopolitically mandated corporate restructuring with immediate supply chain consequences. Investment decisions once governed by cost cycles are now governed equally by export control compliance and geopolitical alignment risk.

The same logic runs deeper, into the raw materials underpinning the technology. China controls the processing of roughly 60 to 70% of global rare earth supply, inputs that underpin semiconductor fabrication, electric vehicle batteries, and defence systems. Beijing demonstrated in 2025 that rare earth export restrictions are a viable retaliatory instrument. This is geographic leverage of a different kind: not a maritime chokepoint, but a processing monopoly embedded in specific geology. The geoeconomic tool is identical, restricting resource access to extract strategic concessions, but the terrain is mineralogical rather than nautical.

A third domain completes the picture. The Persian Gulf accounts for roughly 30% of globally traded urea and 20 to 30% of ammonia exports. When Hormuz is disrupted, the agricultural input shock transmits directly into food price inflation across import-dependent economies in Asia, Africa, and the Middle East, a transmission channel the IMF identifies separately from the energy shock in its April 2026 WEO. Geography, in this case, does not merely move energy markets. It governs the cost of feeding populations.

Capital Markets Pricing Policy, Not Just Fundamentals

For four decades, equity and fixed income markets were primarily responsive to earnings, growth, and monetary policy. Geopolitical risk was priced at the margin, a tail premium applied episodically during crises and faded quickly afterward. That framework is no longer adequate.

The IMF's April 2026 World Economic Outlook makes the shift explicit. The pre-conflict 2026 growth forecast would have been revised upward to 3.4%. Instead it sits at 3.1%, with inflation at 4.4%, a stagflationary configuration in which the conventional policy toolkit is genuinely impaired. Central banks cannot stimulate without risking inflation entrenchment. They cannot tighten without deepening the slowdown. The IMF's adverse scenario models the federal funds rate rising 50 basis points in 2026 and 100 basis points in 2027, not as a response to demand strength, but as a forced reaction to supply-side price pressure originating from geography. That reprices assets across the entire risk spectrum. Equity markets have confirmed this in real time. S&P 500 movements in April 2026 have tracked Gulf diplomatic signals more closely than US earnings results, which have started the reporting season strongly. When Iran signalled the strait was reopening, equities surged to record highs. When gunfire resumed days later, futures fell and oil jumped. The geopolitical variable is not noise around a fundamental signal. It is the signal.

The crisis is also accelerating a challenge to dollar architecture that predates it. The 2022 freezing of Russian sovereign reserves signalled to governments worldwide that dollar-denominated assets carry sovereign risk. Bilateral non-dollar settlement has expanded, Gulf states have explored yuan-denominated oil contracts, and BRICS economies have invested in alternative payment infrastructure. The dollar has behaved as expected in the current crisis, strengthening against emerging market currencies as capital seeks safety, yet that reflex sits in direct tension with the fragmentation dynamic. A currency functioning simultaneously as a safe haven and a sanctions instrument creates the structural incentive to hedge against it, even among nations still reliant on it. The dollar's reserve status is not under immediate threat. The incentive to reduce exposure to it is growing permanently.

The Structural Trade-Off: Efficiency Yielding to Resilience

The globalisation model built from the 1990s through the 2010s was organised around comparative advantage and cost optimisation. Supply chains were concentrated in lowest-cost locations. Capital flowed to highest returns regardless of political context. The system was efficient and, as successive disruptions have demonstrated, structurally fragile.

The response, from governments in the United States, Europe, Japan, and across emerging markets, has been to redirect capital toward strategic resilience. Domestic semiconductor subsidies, strategic petroleum reserve policies, near-shoring of critical supply chains, and state-directed defence investment all share the same logic: market efficiency subordinated to strategic security. The macroeconomic consequence is permanently higher structural costs. Redundant supply chains, domestically subsidised manufacturing, and strategic inventory buffers are all more expensive than their optimised equivalents. These are not temporary adjustments. They are durable increases in the global cost base embedded by policy decisions that will not reverse on short timescales.

The burden falls unevenly. Energy-exporting nations, including Gulf producers and certain Latin American commodity exporters, benefit from the sustained price premium that geoeconomic tension generates. Energy-importing emerging markets face the opposite: currency depreciation as import bills rise, inflationary pass-through constraining domestic consumption, and fiscal pressure on governments with limited buffers. The IMF's growth revision for emerging market and developing economies runs 0.3 percentage points below the January forecast, with commodity-importing nations facing materially worse outcomes. The geoeconomic transition is not a uniform global experience. It is producing structural divergence between nations on opposing sides of the resource and alignment divide.

The Limits: Geography Has Not Been Displaced

The geoeconomic framework requires one qualification. Geography has not been superseded; its role has been amplified.

The Strait of Hormuz matters because it is physically irreplaceable. Taiwan matters because leading-edge semiconductor fabrication is geographically concentrated on a single island. Rare earths, lithium, and cobalt matter because they are physically located in specific jurisdictions, Congo, Chile, China, and cannot be relocated by policy decree. The leverage geoeconomics exercises is always anchored to something geographic: a location, a resource, a processing node in a physical network.

What has changed is the form that leverage takes.

The objective of disrupting Hormuz is not territorial; it is the ability to move commodity markets, inflate global energy costs, and constrain central bank policy across dozens of countries.

The objective of semiconductor export controls is not to occupy Taiwan; it is to determine which nations access the technologies defining the next decade of economic competitiveness.

The objective of rare earth restrictions is not geological; it is negotiating leverage in a broader competition.

The geoeconomic premium is not permanent by assumption. It would compress under specific conditions: a durable multilateral framework reducing strategic uncertainty around chokepoints; the institutionalisation of competing blocs with rules clear enough to eliminate alignment ambiguity for firms and capital allocators; or technological substitution reducing dependence on specific geographic nodes, such as advanced battery chemistries lowering rare earth intensity, or energy transition pathways structurally reducing hydrocarbon demand. None is imminent. But an analytically honest framework must acknowledge them. The magnitude of the geoeconomic premium depends on the perceived permanence of disruption, not merely its current intensity. Geography sets the stage. Geoeconomics runs the performance.

Conclusion: A Structural Transition, Not a Cyclical Shift

The transition from geographic to geoeconomic statecraft is not a temporary condition created by specific conflicts or administrations. It reflects a durable shift in how states compete, how supply chains are organised, and how capital is allocated in a world where economic systems are simultaneously the target and instrument of strategic power. Hormuz demonstrated how a geographic chokepoint translates into inflation, central bank constraints, equity market volatility, and institutional portfolio risk. Semiconductor export controls and rare earth restrictions demonstrated how technology and resource policy reshapes capital allocation along geopolitical rather than commercial lines. The dollar's reserve architecture faces a structurally motivated challenge as nations build alternatives to financial systems revealed as leverage instruments. The IMF's revised macro baseline, slower growth, higher inflation, stagflationary policy constraints, reflects the aggregate cost of that transition.

For investment frameworks, the implication is direct. Models treating geopolitical risk as an episodic overlay on a fundamentals-driven baseline are operating with an outdated architecture. Policy risk is embedded in valuation. Geopolitical alignment is a capital allocation variable. Energy infrastructure, domestically anchored technology supply chains, defence exposure, and commodity producers in geopolitically stable jurisdictions command structural premiums in this regime. Globally integrated industrials, multinationals concentrated in jurisdictions subject to bloc competition, and assets denominated in currencies vulnerable to sanctions architecture face persistent re-rating pressure.

The question is no longer whether geography shapes economic outcomes. It always did. The question is how completely geoeconomics has become the primary language through which that shaping occurs, and whether investment frameworks have caught up to that reality.

Please wait processing your request...

Please wait processing your request...