Shares of Rivian Automotive surged nearly 30% intraday, marking one of the stock’s strongest single-day performances since its post-IPO decline. The rally followed the company’s unveiling of a more affordable electric SUV platform—an announcement that appears to have altered investor perceptions of Rivian’s long-term scale, addressable market, and competitive positioning within the global electric vehicle (EV) industry.

The market reaction suggests not an abrupt improvement in near-term profitability, but rather a reassessment of Rivian’s strategic trajectory. In an EV sector increasingly shaped by price sensitivity, slowing demand growth, and tighter capital conditions, affordability has emerged as the industry’s defining battleground. Rivian’s pivot signals a transition from premium exclusivity toward volume-driven electrification.

From Premium Adventure Brand to Scaled EV Platform

Rivian’s early success was built on the R1T pickup and R1S SUV—vehicles that established strong brand equity, engineering credibility, and customer loyalty within the premium “electric adventure” niche. Yet price points north of USD 70,000 imposed natural limits on demand elasticity and volume expansion.

The forthcoming lower-cost SUV represents a deliberate recalibration of Rivian’s business model. By targeting a broader consumer base, management is implicitly acknowledging that long-term EV winners will be determined less by novelty and more by manufacturing scale, cost discipline, and supply-chain optimisation.

In theory, higher volumes offer meaningful advantages: improved fixed-cost absorption, stronger negotiating leverage with suppliers, and declining battery costs through learning curves. In practice, however, moving down-market introduces operational complexity and margin pressure. Rivian’s challenge will be to scale without eroding the brand, balance-sheet resilience, or manufacturing execution.

Delivery Growth Expectations and the Execution Question

Investor enthusiasm reflects rising confidence that a competitively priced electric SUV could materially expand Rivian’s delivery trajectory—particularly as EV adoption shifts toward middle-income consumers. Until now, Rivian’s delivery volatility has stemmed from both production ramp inefficiencies and demand concentration among affluent buyers.

A broader pricing architecture may mitigate demand cyclicality. But history offers cautionary lessons: automotive markets routinely punish companies that announce ambitious products without delivering consistent output.

Rivian’s ability to translate strategic intent into sustained production will depend on execution across validation builds, supplier coordination, and operational efficiency at its Normal, Illinois facility. Announcements may move markets; factories ultimately determine outcomes.

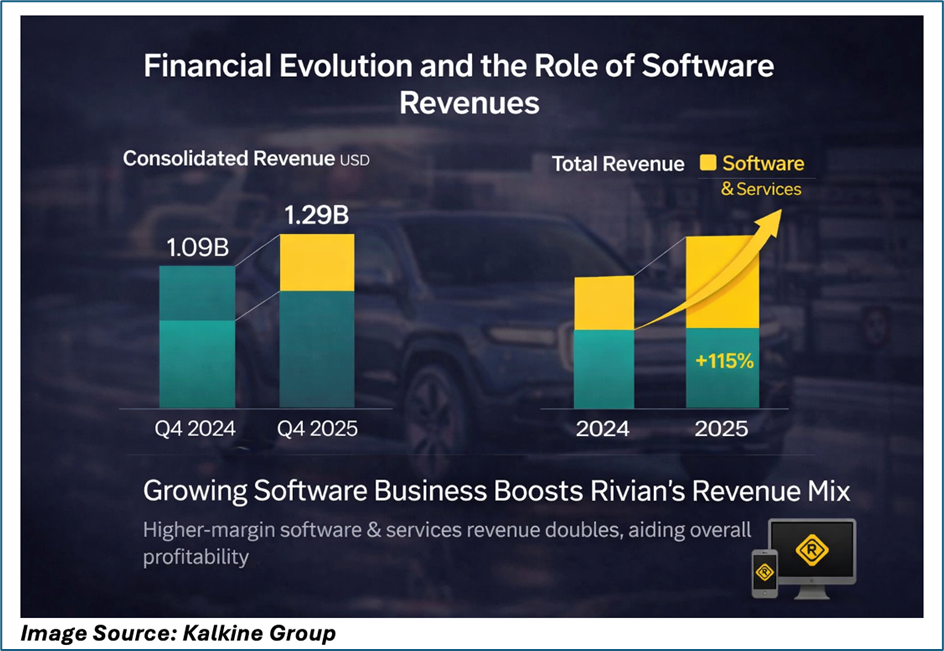

Financial Evolution and the Role of Software Revenues

Rivian’s latest financial results underscore a company in transition. Fourth-quarter 2025 consolidated revenue reached USD 1.29 billion, though automotive revenue declined year on year, reflecting lower deliveries and reduced regulatory credit sales following US tax-credit changes.

More encouraging was the sharp rise in software and services revenue, which more than doubled. Growth was driven by the Volkswagen joint venture, increased remarketing activity, and expanded fleet services. For full-year 2025, consolidated gross profit improved materially versus 2024, aided by cost-per-vehicle reductions and higher-margin software contributions.

This shift hints at Rivian’s longer-term ambition: to evolve from a pure-play automaker into a vertically integrated mobility and software platform. Yet automotive margins remain acutely sensitive to volume, pricing, and incentive structures, making execution paramount as affordability becomes central to the strategy.

Analyst Upgrades and a Re-rating of Strategic Optionality

Following the announcement, sell-side analysts revised delivery assumptions and valuation frameworks, citing improved visibility into Rivian’s product pipeline and a more credible path to scale. The re-rating reflects strategic optionality rather than near-term earnings acceleration.

In a capital-intensive sector exposed to interest-rate cycles and consumer financing conditions, clarity of direction carries disproportionate weight. Still, most analysts maintain a cautious stance, emphasising production execution, competitive intensity, and capital allocation discipline as key determinants of medium-term equity value.

Competition, Autonomy, and Differentiation in the Electric SUV Segment

The electric SUV market remains one of the most fiercely contested arenas globally. Legacy automakers and EV-native rivals alike are compressing price bands and accelerating model launches.

Rivian’s historical differentiation has rested on a blend of lifestyle branding, vertical integration, and proprietary software. Its recent Autonomy & AI Day reinforced these ambitions, showcasing developments such as the RAP1 autonomy processor and expanded assisted-driving capabilities.

As the company pivots toward affordability, differentiation will likely hinge less on rugged exclusivity and more on software integration, autonomy features, and total cost of ownership—areas where scale and data advantages compound over time.

Capital Discipline and the Cost of Scaling

Despite renewed optimism, risks remain substantial. Rivian continues to face production-ramp complexity, supply-chain volatility, and macroeconomic headwinds, including elevated borrowing costs.

Management’s 2026 outlook forecasts deliveries of 62,000 to 67,000 vehicles, alongside ongoing adjusted EBITDA losses and significant capital expenditures. With free cash flow still negative, liquidity management and capital efficiency will remain central to investor scrutiny.

The market’s patience will ultimately be conditioned on evidence that growth can be achieved without perpetual balance-sheet strain.

Technical Analysis: Daily Chart Signals a Momentum Inflection

Price Structure and Moving Averages

Rivian shares surged to USD 18.11, firmly reclaiming the 21-day moving average (~USD 15.32) while testing the 50-day moving average near USD 17.50–18.00. This places the stock in an early recovery phase within a broader corrective trend from the USD 22.69 peak. A sustained close above the 50-day average would materially strengthen the intermediate-term technical outlook.

Momentum and RSI

The Relative Strength Index (RSI) has recovered to approximately 56, signalling neutral-to-moderately bullish momentum. Importantly, the indicator remains well below overbought territory, suggesting room for continuation should buying pressure persist.

Volume and Key Levels

Trading volume exceeded 50 million shares, lending credibility to the breakout. Near-term resistance sits at USD 18.50, while initial support is forming around USD 15.30, with stronger structural support in the USD 13.50–14.00 range.

An Institutional View on Rivian’s Strategic Inflection

Rivian now appears to be navigating a structural shift—from premium EV entrant to scalable electric mobility platform integrating hardware, software, and autonomy. The affordable SUV initiative aligns with a maturing EV market in which cost competitiveness and operational discipline increasingly determine survival.

Recent gains in software revenue and consolidated gross profit suggest tangible progress. Yet durable value creation will hinge on execution: consistent delivery growth, margin stabilisation, and disciplined capital allocation.

The market’s reaction reflects confidence in direction rather than destination. Whether that confidence endures will depend on Rivian’s ability to convert strategic ambition into industrial reality, quarter by quarter, vehicle by vehicle, and dollar by dollar.

_06_19_2026_04_14_48_775022.jpg)

_06_19_2026_04_15_58_896873.jpg)

_06_19_2026_04_16_38_970455.jpg)

_06_19_2026_04_17_25_556135.jpg)

_06_19_2026_04_18_05_865257.jpg)

_06_19_2026_04_19_00_614719.jpg)

Please wait processing your request...

Please wait processing your request...