Upstream control of chip fabrication, packaging, and critical minerals is redefining technology sector risk. Analyse how structural bottlenecks at key semiconductor nodes are creating unhedgeable exposure for downstream firms.

Key Highlights

- Semiconductor market power is consolidating at upstream nodes where substitution is technically or commercially infeasible.

- Advanced packaging, not wafer fabrication, is now the binding constraint on AI chip supply.

- China's export controls on gallium, germanium, and rare earths confirm that chokepoint leverage extends to raw materials, with the legal framework for reimposition intact.

- Hyperscaler capital expenditure is projected to exceed $600 billion in 2026, concentrating demand into a supplier cluster that cannot match the pace.

- Western policy responses, including the US CHIPS Act and European Chips Act, are undersized and too slow relative to the risks they target.

The Chain That Holds Everything Together

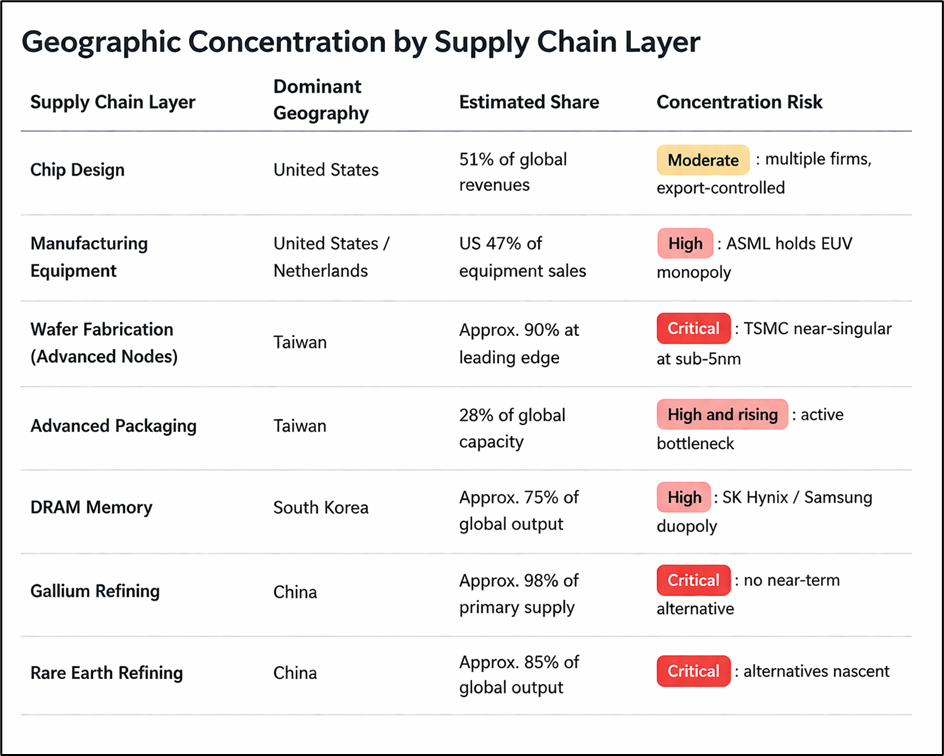

The semiconductor supply chain is one of the most technically complex industrial systems ever assembled. It is also, at several critical junctures, one of the most fragile. The chain runs from raw material refining through chip design, wafer fabrication, advanced packaging, and final distribution. Each stage involves a distinct set of firms, geographies, and technical requirements. At several of those stages, the number of credible suppliers narrows to one or two.

Source: Kalkine

The aggregate picture suggests geographic diversification. The node-level picture does not. A single disruption does not need to affect every layer simultaneously. Disabling any one critical node is sufficient to stall the entire chain downstream.

Built for Efficiency, Not Survival

This chain was deliberately optimised for cost over three decades, not for resilience. Just-in-time inventory practices removed buffers. Geographic specialisation deepened with each consolidation cycle. The model performed well under stable conditions. Under geopolitical stress, it proved structurally fragile.

The COVID-19 pandemic exposed this first, as production shutdowns across Asia cascaded into chip shortages that halted automotive and electronics output across multiple continents. What followed clarified that the disruption was not temporary. Escalating US-China technology restrictions, export controls on advanced lithography equipment, and sustained concern over Taiwan Strait security have collectively transformed supply chains from commercial infrastructure into contested strategic assets.

This matters analytically because it changes the location of risk. A growing portion of operational and financial risk for technology firms now originates upstream, in production nodes they do not own and cannot easily replicate. Historical margin and capital efficiency data for downstream firms may embed an unpriced geopolitical subsidy that is now being withdrawn.

Where Power Actually Concentrates

The concentration at several upstream nodes approaches monopoly conditions by any practical definition. The firms involved do not merely hold dominant market shares. They hold structural positions where substitution is technically infeasible or commercially prohibitive within any near-term horizon.

ASML (NASDAQ:ASML) is the sole global supplier of extreme ultraviolet lithography machines, the equipment required to manufacture chips below 7nm. No credible second source exists anywhere in the world. A single EUV system contains over 100,000 components and draws on supplier relationships built over decades. That irreproducibility gives ASML a form of structural market power that conventional antitrust frameworks, designed around output markets and consumer pricing, were not built to address.

TSMC (NYSE:TSM) holds an equivalent position in advanced chip fabrication. The combination of process expertise, ecosystem depth, and capital intensity of modern fab construction, where a single leading-edge facility exceeds $20 billion, has proved insurmountable for any challenger attempting to replicate its capability at comparable scale or speed.

Source: Kalkine

A platform's dominance can in principle be disrupted by a superior product or regulatory intervention. ASML's monopoly cannot. This makes upstream node concentration categorically more durable than the forms of market power typically analysed in technology equity research.

Source: Kalkine

The AI Cycle and Active Fault Lines

The current AI infrastructure investment cycle has sharpened these risks considerably. Training and deploying large AI models requires advanced GPUs, high-bandwidth memory, and fabrication at the most advanced process nodes. All three requirements route through the same narrow supplier cluster, and demand is rising faster than available capacity can accommodate.

The bottleneck has moved from front-end wafer fabrication to back-end advanced packaging, specifically TSMC's chip-on-wafer-on-substrate process required to integrate high-bandwidth memory with AI processors. Industry projections place packaging capacity in the range of 120,000 to 130,000 wafers per month by end of 2026. Given the pace of AI infrastructure investment, the supply gap is unlikely to close within that horizon.

On materials, China initiated export licensing requirements on gallium and germanium in August 2023, broadly interpreted as calibrated retaliation against Western semiconductor equipment controls. In December 2024, Beijing tightened this to an effective export ban on gallium, germanium, antimony, and superhard materials directed specifically at the United States. Those controls were temporarily suspended in November 2025 as part of US-China trade negotiations, but the legal framework enabling their reimposition remains fully intact. By May 2025, China had restricted exports of at least 16 key minerals and alloys, a number that has continued to expand.

On demand, according to Epoch AI analysis published in February 2026, combined capital expenditure by the five largest cloud providers grew at an average annual rate of approximately 72 percent between mid-2023 and end-2025. Aggregate hyperscaler infrastructure spending is projected to exceed $600 billion in 2026, with approximately 75 percent directed at AI-specific infrastructure. This level of sustained demand creates structural pricing power for the upstream suppliers absorbing it.

Scenario Analysis: When the Chain Breaks

The concentration mapped above is not merely a market structure concern. It carries concrete, asymmetric risk across industries, economies, and capital markets. A disruption at any critical upstream node would not produce a contained supply shortage. It would trigger a cascading system failure.

Scenario 1: Taiwan Operational Disruption

The most severe risk centres on Taiwan. A sustained disruption to TSMC's operations, whether from geopolitical conflict, natural disaster, or critical infrastructure failure, would within months simultaneously halt production of AI accelerators, smartphones, data centre processors, and automotive chips. No alternative source exists capable of absorbing that volume at comparable process nodes. Recovery timelines, based on the pace of fab construction elsewhere, would be measured in years. For institutional investors, this risk is effectively unhedgeable through conventional financial instruments.

Scenario 2: Broad Raw Materials Cutoff

China initiated export licensing requirements on gallium and germanium in August 2023, tightening to an effective US-targeted ban in December 2024 before a temporary suspension in November 2025 as part of trade negotiations. The legal framework enabling reimposition remains fully intact. By May 2025, China had restricted exports of at least 16 key minerals and alloys. A broader restriction extending across rare earths would simultaneously affect consumer electronics, defence systems, and electric vehicle motors. Unlike chip fabrication, where Western capacity duplication is underway, rare earth refining alternatives remain nascent and are unlikely to reach meaningful scale before the early 2030s.

Scenario 3: Advanced Packaging Constraint

This scenario is not hypothetical. It is the current operating condition. TSMC's chip-on-wafer-on-substrate process is the binding constraint on AI accelerator supply. Industry projections place packaging capacity in the range of 120,000 to 130,000 wafers per month by end of 2026, but this expansion is being absorbed in real time by accelerating AI infrastructure investment. Long-term supply contracts provide allocation priority, not volume guarantees. The supply gap is unlikely to close before 2027 at the earliest, meaning AI deployment timelines across the industry are being set by TSMC's packaging allocation decisions, not by the AI firms themselves.

Scenario 4: EUV Supply Disruption

ASML produces extreme ultraviolet lithography machines at a single facility in the Netherlands. No second source exists anywhere in the world. A disruption to that production, whether from physical damage, regulatory intervention, or export control escalation, would make advanced chip manufacturing below 7nm impossible for any period of interruption. Recovery would require rebuilding institutional knowledge and supplier relationships that took decades to assemble. Of all scenarios, this carries the longest potential recovery horizon and the least available mitigation.

Insurance frameworks are not designed for systemic supply chain failures of this nature, and hedging instruments for physical semiconductor supply do not exist in any practical form. The risk, for institutional investors holding concentrated downstream positions, is largely unhedgeable through conventional financial means.

Policy Response: Ambition Versus Execution

Western governments have moved to address supply chain vulnerability with substantive capital commitments. The analytical question is whether these programmes are sufficient in scale, speed, and design to meaningfully reduce the structural risks they target. On current evidence, the answer is no.

The US CHIPS and Science Act committed approximately $52 billion toward domestic semiconductor manufacturing and research. It is the most execution-credible programme among Western initiatives. TSMC's Arizona first fabrication facility entered high-volume production in the fourth quarter of 2024. The second facility, targeting 3-nanometer production, is now expected to reach mass production in the second half of 2027, an improvement on earlier timelines but still more than five years from the original project announcement. A third facility broke ground in April 2025. The trajectory is encouraging. It does not resolve the near-term supply gap.

The European Chips Act mobilises approximately 43 billion euros in policy-driven investment to 2030, targeting a 20 percent share of global chip output. In April 2025, the European Court of Auditors published a special audit finding that the 20 percent target was very unlikely to be met. The EU Commission directly controls only approximately 10 percent of total public funding committed under the programme, with the remainder fragmented across member state budgets without a central coordination mechanism. Progress on Pillar I, covering research and design, has been reasonable. Progress on Pillar II, covering large-scale manufacturing investment, has been slow.

Japan's approximately $6 billion in subsidies supporting the TSMC Kumamoto joint venture produced a Phase 1 facility that entered production in February 2024. It is among the fastest-executing Western-aligned programmes. It produces chips at legacy and mid-range process nodes, not at the leading edge where the strategic dependency is most acute.

India's Semicon India Programme, backed by approximately $10 billion in incentives, had approved 10 projects across six states as of December 2025. The Kaynes Semicon and Micron assembly and testing facilities opened in early 2026. The programme is building a foundation in packaging, testing, and legacy fabrication. It does not address the advanced node gap.

The binding constraint across all programmes is not solely financial. Advanced semiconductor manufacturing talent cannot be scaled at policy speed. Supplier ecosystems built over decades in Taiwan and South Korea cannot be transplanted by capital incentives alone. Even optimally designed domestic capacity would not produce strategic redundancy before the early 2030s.

Implications for Capital Allocation

Firms controlling critical upstream nodes command premium valuation multiples grounded in durable pricing power. That premium is analytically defensible, but it coexists with geopolitical tail risk that standard discounted cash flow models do not adequately capture.

For downstream companies, the risk is less visible and for that reason potentially more consequential. Alphabet (NASDAQ:GOOGL) and Amazon (NASDAQ:AMZN) are developing custom silicon to reduce GPU dependency, yet both continue to rely on TSMC's advanced fabrication nodes. Vertical integration at the design layer does not resolve dependency at the production layer. It merely relocates the interface at which upstream concentration is encountered.

The technology sector is structurally moving away from an asset-light earnings model. Long-term supply contracts, upfront capacity reservations, and equity participation in fab expansions are becoming standard instruments for securing constrained production. This increases capital intensity, reduces earnings flexibility, and introduces a category of balance sheet commitment that analysts should factor into free cash flow assessments. Global semiconductor revenues are projected to approach $1 trillion by end of decade, rising from approximately $650 billion in 2024. An increasing share of that value will accrue to firms controlling physical production constraints, not those commanding product markets.

The Structural Reality

Supply chain bottlenecks in technology are not a cyclical disruption awaiting correction. They reflect a structural paradox that deepens with each cycle of technological advance: the more central advanced chips become to economic activity, the more the entire system depends on a shrinking number of highly specialised, geographically concentrated, and politically exposed production nodes. Progress and fragility are not in tension. They are coupled.

The risk categories that matter most have shifted in both location and character. Competitive risk has moved from end markets to upstream production access. Financial risk has shifted from demand cyclicality to supply availability. Geopolitical risk has escalated from tariff friction to the deliberate weaponisation of materials and equipment controls. Innovation risk now carries an upstream dependency layer that did not previously exist. Regulatory risk has expanded from antitrust in output markets to export controls in input markets, a dimension that existing frameworks were not designed to address.

For firms controlling critical upstream nodes, that repositioning represents durable structural pricing power. For downstream technology companies, it represents an embedded and largely unquantified exposure. Alphabet and Amazon are developing custom silicon to reduce GPU dependency, yet both continue to route through TSMC's advanced fabrication nodes. Vertical integration at the design layer does not resolve dependency at the production layer.

Global semiconductor revenues are projected to approach $1 trillion by end of decade, rising from approximately $650 billion in 2024. An increasing share of that value will accrue to firms controlling physical production constraints, not those commanding end markets. Investors and analysts evaluating technology sector exposure need to extend their competitive framework accordingly. The question of who controls the inputs to advanced technology, who holds the fabrication chokepoints, who commands packaging capacity, and who supplies critical raw materials, may prove over the next decade to be as consequential for capital allocation outcomes as the question of who controls the outputs.

Please wait processing your request...

Please wait processing your request...