Key Highlights

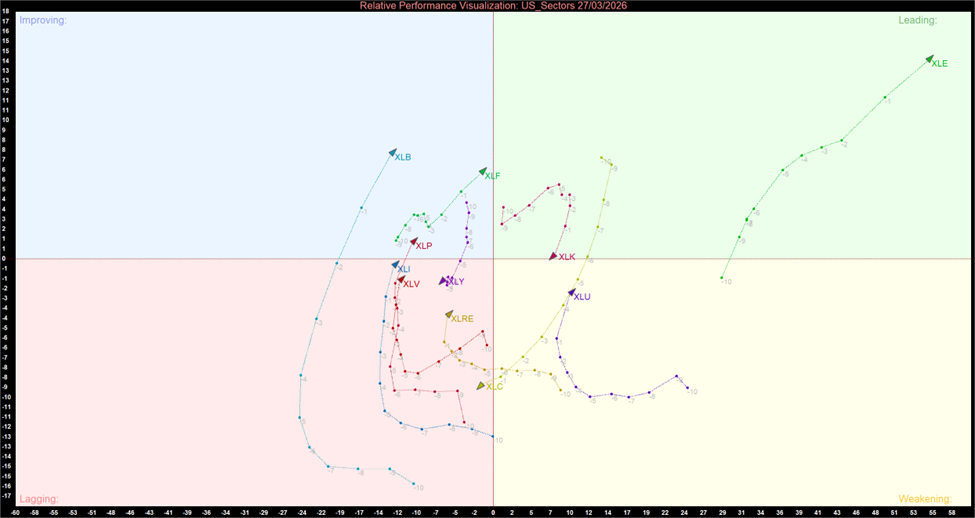

- The Lone Leader: Energy (XLE) is the singular sector remaining in the Leading quadrant, cementing its status as the market's only true area of absolute strength and momentum.

- Tech's Fall from Grace: Information Technology (XLK) has slipped out of leadership, flatlining on momentum and bleeding relative strength.

- A Massive Lagging Cluster: Communication Services (XLC) has officially crossed the vertical axis into the Lagging quadrant, joining Industrials (XLI), Health Care (XLV), Consumer Discretionary (XLY), and Real Estate (XLRE). Nearly half the market is now technically underperforming the S&P 500.

- Synchronized Leftward Shift: In a rare technical alignment, ten out of the eleven sectors have trails hooking left (West), indicating a broad-based loss of relative strength mathematically skewed by Energy's massive outperformance.

The US sector rotation on 27 March 2026, reveals a highly unusual and skewed momentum environment. As the momentum chart illustrates, capital is not broadening out; it is funneling aggressively into one specific theme, leaving a growing portion of the market struggling in the Lagging quadrant.

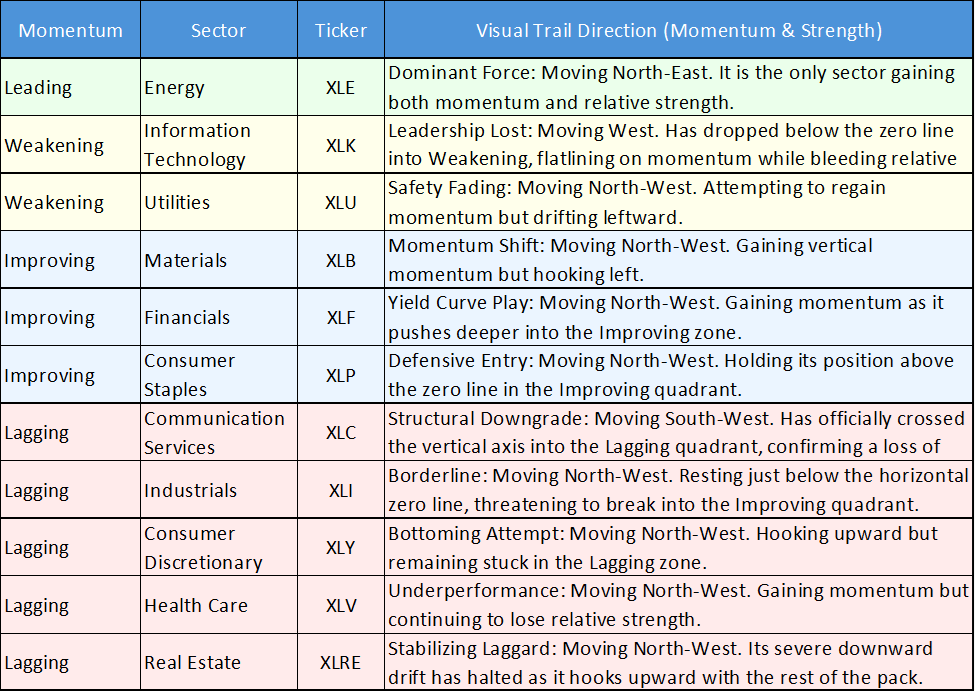

Daily US Sector Momentum Summary

The following table categorizes all 11 sectors into their confirmed RRG quadrants based on precise horizontal and vertical zero-line crossings:

Daily US Sector Relative Momentum Chart – 27/03/2026

US Sector Relative Momentum Chart (at the closing price of 28th March 2026). Powered by: amibroker.com

Daily US Sector Momentum Summary Table

Key Market Themes

The Solitary Leadership of Energy

When only one sector occupies the Leading quadrant, it is a glaring warning sign about market breadth. Capital is crowding exclusively into Energy (XLE) as an inflation hedge and safe haven. Because the RRG measures performance relative to the S&P 500, Energy's massive, uninterrupted North-East surge is skewing the benchmark average. This forces the rest of the market's relative strength to point leftward (West) simply because no other sector can match the commodity space's aggressive capital inflows.

The Swelling Lagging Cluster

The confirmation that Communication Services (XLC) has dropped into the Lagging quadrant highlights a growing problem for the broader market. With XLC joining Discretionary, Real Estate, Health Care, and Industrials, nearly half of the major US sectors are now officially underperforming the broader benchmark. This concentration of weakness confirms that the current market environment is highly selective and unforgiving to sectors without an immediate catalyst.

The Mixed "Improving" Bag

The Improving quadrant contains a strange mix of bedfellows: Materials (XLB), Financials (XLF), and Consumer Staples (XLP). This lacks a cohesive macroeconomic theme (like a pure cyclical recovery or a pure defensive flight). Instead, it suggests a fragmented market where institutional managers are selectively hunting for value and yield-curve stabilization (Financials) or basic inflation hedges (Materials) while keeping a small allocation in pure safety (Staples) as they rotate out of tech and communications.

Bottom Line

The momentum landscape as of March 27 is defined entirely by the solitary strength of Energy and a rapidly growing cluster of laggards. With Tech and Communications officially losing their leadership status, the rest of the market is caught in a synchronized leftward drift. Until a unified thematic recovery emerges to join Energy, the market remains highly vulnerable to macro-driven headline risk.

Please wait processing your request...

Please wait processing your request...