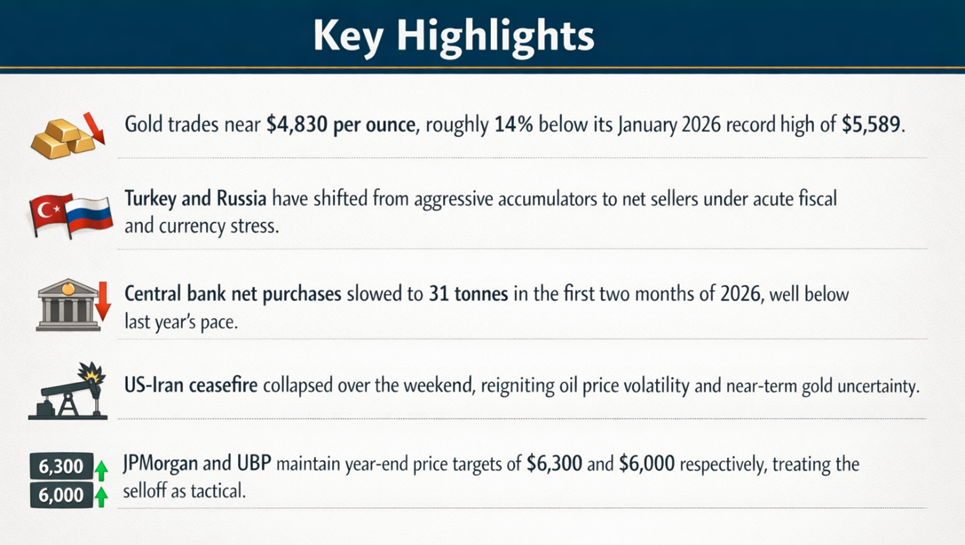

Central banks shift from gold buyers to sellers as war-driven fiscal stress tests the metal's reserve role, with prices down 14% from January highs and institutional forecasts still targeting $6,000–$6,300 by year-end.

Source: EODHD/Others, Analysis by Kalkine

From Accumulation to Liquidation

For three consecutive years following Russia's 2022 invasion of Ukraine, central bank gold demand operated as one of the most dependable structural forces in commodity markets. The 1,237 tonnes purchased by sovereign institutions in 2025 alone exceeded the combined annual mine output of several mid-sized producing nations, distributed across more than 40 central banks: a demand base broad enough to resist disruption from any single buyer's policy shift.

That architecture is now under strain. Gold scaled a record $5,589 per ounce in late January 2026 before entering a sharp correction. The metal touched a cycle low near $4,099 on March 23, representing a decline of roughly 27% from peak, before recovering as ceasefire hopes briefly eased energy market pressure. As of April 15, spot gold trades near $4,830, partially recovering on renewed diplomatic signals between Washington and Tehran, but still approximately 14% below its January high.

Wartime Economics Driving the Selloff

Source: EODHD/Others, Analysis by Kalkine

The drivers are specific and traceable. The Iran war disrupted the Strait of Hormuz, drove crude oil sharply higher, and pushed safe-haven flows into gold throughout early 2026.

For central banks in import-dependent and conflict-adjacent economies, the combination of a stronger US dollar, elevated energy costs, and weakening domestic currencies has transformed gold reserves accumulated during calmer years into emergency liquidity instruments. The Central Bank of Turkey utilised approximately 50 tonnes of its gold reserves in March for liquidity purposes and foreign exchange operations, with Governor Fatih Karahan confirming that a significant portion of these transactions involved gold-currency swap futures.

Russia has been selling gold since 2025 to help fund budget shortfalls, while Turkey's lira hit its eleventh consecutive record low against the US dollar within sixteen trading sessions of the Iran conflict beginning. Poland, the largest central bank buyer of bullion in both 2024 and 2025, has also entered the debate. Governor Adam Glapiński proposed generating approximately $13 billion through potential gold sales to finance the country's fast-growing defense expenditure, with the stated intention of subsequently repurchasing reserves.

Structural Demand Is Decelerating

Selling pressure from distressed sovereign holders is compounded by a broad deceleration in core buying. Central banks bought a net 27 tonnes in February 2026, a rebound from a quiet January, but the two-month cumulative total of 31 tonnes tracks well behind the 50 tonnes recorded over the same period in 2025.

The picture is not uniformly bearish among buyers. China reported its sixteenth consecutive month of net purchases in February, bringing gold reserves to 2,308 tonnes, equivalent to 10% of total reserves. The Czech Republic extended its buying streak to thirty-six consecutive months, while Southeast Asian and African central banks have continued to emerge as new entrants.

Tactical Retreat, Not Structural Exit

Institutional consensus treats the current episode as a tactical adjustment within a longer-term accumulation cycle rather than a fundamental reassessment of gold's reserve asset status. During the past fifteen years of continuous net buying by the official sector, monthly sales have occurred regularly for reasons including currency defence and portfolio rebalancing, without interrupting the broader trend.

UBP reaffirmed its $6,000 per ounce year-end target on April 13 and has rebuilt its gold allocation from approximately 3% to 6% of discretionary client portfolios after reducing exposure during the Iran war selloff. JPMorgan maintains a $6,300 year-end forecast. Gold held near $4,840 in early April 15 trading, supported by reports that Washington and Tehran are working to schedule a second round of peace negotiations before the ceasefire expires on April 21.

The fundamental paradox is straightforward. Gold was acquired as financial insurance against precisely the kind of shock currently unfolding. When that shock arrives and fiscal pressure intensifies, the insurance policy is redeemed. What the market must now determine is whether patient buyers in Asia and among longer-horizon institutional investors can absorb that redemption pressure before it translates into a deeper structural reset of prices.

Please wait processing your request...

Please wait processing your request...