Meta description: China's gold imports surged to 162 tonnes in March 2025 — the highest since March 2024 — as the People's Bank of China extended its buying streak to 17 consecutive months, lifting official reserves to a record 2,313 tonnes. Here is what Beijing's accelerating gold accumulation means for global markets.

Key highlights

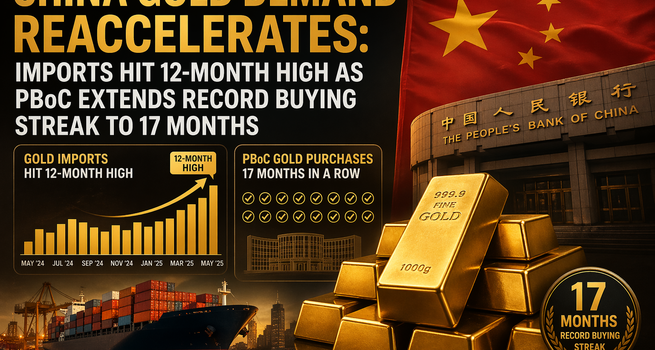

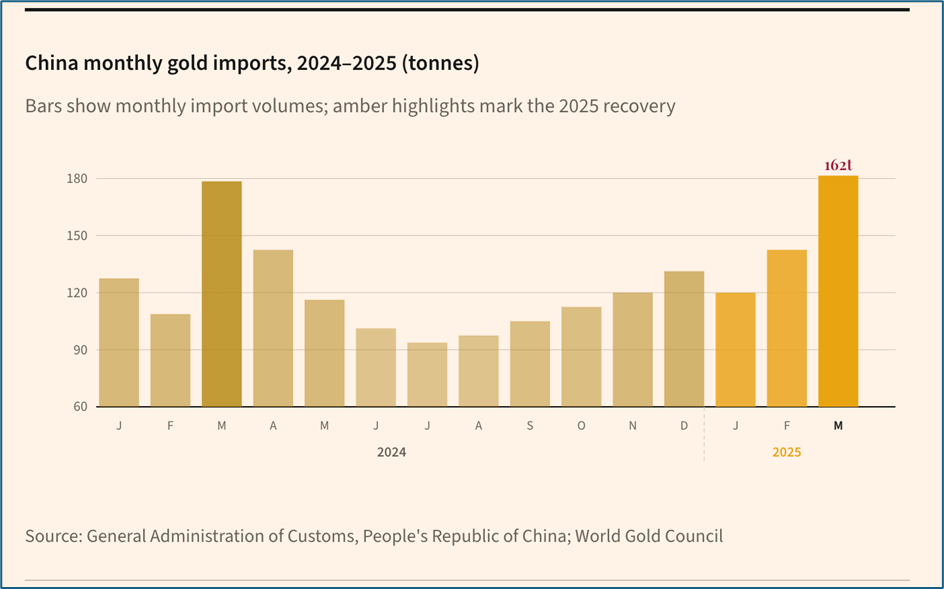

- Chinese gold imports rose to 162 tonnes in March — the highest monthly figure since March 2024 and the third consecutive monthly increase

- Year-to-date imports stand at approximately 365 tonnes, tracking well above recent comparable periods

- The PBoC added 5 tonnes in March, its largest single-month purchase since February 2025

- Seventeen consecutive months of central bank buying — an unbroken streak

- Official PBoC gold holdings now stand at a record 2,313 tonnes

China's gold market is accelerating again. After a pronounced lull through the middle of 2024, when elevated domestic prices and a softening consumer mood combined to suppress demand, the world's largest buyer of gold is reasserting itself with considerable force.

Imports of gold into China climbed to 162 tonnes in March, the highest monthly tally since March 2024, according to data from the General Administration of Customs. The figure represents the third consecutive month of rising inflows, with year-to-date imports reaching approximately 365 tonnes — a pace that, if sustained, would place 2025 among the stronger years on record for Chinese gold demand.

The rebound is striking in its speed and breadth. Private consumer demand, which had stalled as domestic gold prices tracked global spot prices sharply higher last year, appears to be reviving. Jewellery retailers across the country had faced a painful squeeze: international prices surging past $2,400 per troy ounce last spring drew in large volumes of institutional and investment buying even as discretionary consumers pulled back on ornamental purchases. That tension is now easing, with underlying demand re-engaging at levels not seen since the spike that preceded last year's high-watermark.

The structural drivers are well-documented. China's property sector remains in a prolonged contraction, stripping hundreds of millions of savers of what had been their primary store of value. Equity markets, while intermittently buoyant, inspire little confidence as a long-term wealth vehicle. Against this backdrop, gold has emerged as a credible alternative — tangible, liquid, and increasingly culturally embedded. The World Gold Council has noted that Chinese consumer attitudes towards gold have undergone a generational shift, with younger buyers in particular treating the metal as an essential component of a diversified personal balance sheet.

The central bank: seventeen months and counting

Private demand tells only part of the story. The People's Bank of China added five tonnes to its official gold reserves in March, the largest single-month acquisition since February 2025 and the seventeenth consecutive monthly purchase. Total official holdings now stand at 2,313 tonnes, a record high.

The PBoC's uninterrupted buying streak has become one of the defining features of the global gold market. Central bank demand broadly has been elevated since Russia's invasion of Ukraine in 2022 prompted a reassessment of dollar-denominated reserve assets, particularly among emerging-market institutions. China, which holds the largest foreign exchange reserves in the world at approximately $3.2 trillion, has made no secret of its intent to reduce the proportion denominated in US Treasury securities. Gold, which carries no counterparty risk and cannot be frozen or sanctioned, is the natural beneficiary of that reallocation.

At 2,313 tonnes, China's official gold holdings represent just under five per cent of its total reserves — well below the ratios maintained by the United States (around 70 per cent), Germany (roughly 68 per cent) or even Italy. The International Monetary Fund's data suggests that China remains substantially underweight gold relative to its peers among major reserve-holding nations. Even modest steps towards global averages would require purchases measured not in tonnes but in hundreds of tonnes per year.

Geopolitics and the reserve calculus

The March data lands against a backdrop of renewed geopolitical friction. Ongoing trade tensions between Washington and Beijing have sharpened Beijing's focus on reserve diversification, and gold's role as an asset that exists entirely outside the dollar-clearing system has rarely looked more strategically attractive. Each fresh episode of financial coercion, whether directed at Russia, Iran or others, reinforces the logic underpinning the PBoC's accumulation strategy.

Analysts at the World Gold Council estimate that central bank buying globally accounted for over a thousand tonnes of demand in both 2022 and 2023, with 2024 broadly in line. China has been a consistent contributor to that total, and there is little in the March data to suggest any abatement. If anything, the combination of record holdings and continued monthly additions indicates that the PBoC views its current position not as a destination but as a waypoint.

Price implications and the road ahead

Gold's sustained performance — spot prices have traded above $3,000 per troy ounce for much of early 2025 — reflects in part the structural demand backdrop that China represents. A market in which the world's largest consumer nation is simultaneously re-engaging on the private side and steadily accumulating on the official side provides meaningful price support even as Western investment flows remain inconsistent.

The risk to this picture is familiar: a significant appreciation in the Chinese yuan, or a material decline in international gold prices, could dampen import economics and weigh on consumer appetite. There is also the perennial uncertainty around PBoC reporting, which releases data monthly but does not disclose the granular composition of purchases.

For now, however, the trajectory is unambiguous. China imported more gold in the first three months of 2025 than it did in the equivalent period of several recent years. Its central bank has not missed a month of buying in over a year and a half. The gold market's most consequential participant is, once again, fully engaged.

Data sourced from the General Administration of Customs of the People's Republic of China, the People's Bank of China, the World Gold Council, and the International Monetary Fund.

Please wait processing your request...

Please wait processing your request...