Key Highlights

- Copper futures recovered above $5.80 per pound after a volatile week.

- Escalating Middle East tensions lifted oil prices and strengthened the US dollar.

- A stronger dollar and delayed rate-cut expectations pressured base metals.

- China’s 4.5 to 5 percent growth target raised concerns about future copper demand.

- Structural supply deficits continue to support the long term copper investment outlook.

Global Copper Market Analysis: Macro Shocks Drive Price Volatility

Copper prices staged a modest recovery at the end of the week, with COMEX copper futures climbing back above $5.80 per pound after several days of heavy selling pressure. The rebound offered some relief to commodity investors, but the broader weekly trajectory still points to losses as macroeconomic and geopolitical forces dominate price action.

Figure 1: COMEX Copper Futures Price, Source: tradingview.com

The metal, often viewed as a barometer of global economic health, has been pulled into the turbulence created by rising geopolitical tensions, renewed inflation concerns, and a cautious outlook for Chinese growth.

While copper’s long term demand fundamentals remain strong due to electrification and digital infrastructure expansion, short term market direction has increasingly been dictated by global macro developments rather than industrial consumption trends.

Geopolitical Tensions and Commodity Markets: Oil Shock Ripples Through Metals

The escalation of military conflict involving the United States, Israel, and Iran has introduced a new layer of uncertainty across global markets.

As the confrontation entered its seventh day, concerns about energy supply security intensified after Tehran launched missile and drone strikes across the Gulf region. Financial markets reacted swiftly. Investors rotated toward safe haven assets while risk sensitive sectors weakened.

The copper market was caught in this broader risk repricing.

Although copper itself is not directly tied to Middle Eastern energy supply chains, the impact of geopolitical shocks on inflation expectations and currency markets often transmits quickly to industrial metals.

Oil prices surged to multi month highs as traders priced in the risk of potential supply disruptions through the Strait of Hormuz. Higher oil prices tend to push global inflation expectations upward, which in turn influences monetary policy outlooks.

This macro transmission mechanism has historically played a significant role in copper price movements.

Inflation Expectations and the US Dollar: A Key Driver of Commodity Prices

Rising energy prices revived fears that the global disinflation trend may stall.

For the Federal Reserve, the timing presents a delicate challenge. After gradually easing monetary policy during 2024 and 2025 as inflation cooled, policymakers now face the possibility that renewed energy inflation could delay further interest rate cuts.

Financial markets quickly adjusted expectations.

Bond yields moved higher and the US dollar strengthened as traders pushed back the timeline for policy easing. A stronger dollar typically weighs on commodities priced in US currency, including copper, by making them more expensive for international buyers.

The relationship between copper and the US dollar has been particularly visible over the past year. Since September 2025, copper prices have risen roughly 28 percent even as periods of dollar strength created intermittent corrections.

The result is a market where long term structural optimism collides with short term macro headwinds.

China Copper Demand Outlook: Growth Target Signals Slower Industrial Momentum

Another major pressure point for copper this week emerged from China, the world's largest consumer of the metal.

Beijing announced a new economic growth target in the range of 4.5 to 5 percent. While the figure signals continued expansion, it also reflects a more cautious policy stance amid deflationary pressures and ongoing trade tensions with the United States.

For commodity markets, the implications are significant.

China accounts for more than half of global copper consumption, primarily driven by construction, infrastructure development, manufacturing, and renewable energy investment. Any shift in Chinese growth expectations can therefore reshape the demand outlook for industrial metals.

Recent indicators already suggest a moderation in copper demand momentum.

Chinese import premiums have softened and inventory trends remain mixed. Analysts note that much of the strong copper import activity seen earlier in 2025 reflected front loading ahead of potential trade restrictions rather than sustained downstream consumption.

Research from Goldman Sachs indicates that Chinese refined copper demand declined by approximately 8 percent year on year during the fourth quarter of 2025 as stimulus effects began to fade.

While Beijing continues to prioritize infrastructure and energy transition projects, near term industrial activity remains subdued compared with previous expansion cycles.

Global Copper Supply Trends: Mine Disruptions Tighten the Market

Despite weaker demand signals, the supply side of the copper market remains constrained.

Several major mining operations have experienced operational disruptions that continue to limit global output growth.

Indonesia’s Grasberg mine, the world’s second largest copper operation, suffered a major mudslide in late 2025 that triggered force majeure conditions. The primary block cave mining section is expected to remain offline until at least the second quarter of 2026.

Meanwhile, production guidance for Chile’s Quebrada Blanca mine has been revised downward due to operational challenges.

As a result, global mine supply growth for 2026 is currently estimated at only around 1.4 percent, roughly 500,000 tonnes below earlier expectations.

Investment banks increasingly see the market moving into a structural deficit.

J.P. Morgan estimates a global refined copper deficit of around 330,000 tonnes for 2026. The bank expects copper prices to average approximately $5.48 per pound during the year, with potential peaks near $5.67.

Citigroup has presented a more bullish scenario, suggesting that if supply disruptions persist and inventories remain low, copper prices could eventually challenge $6.80 per pound.

Copper Price Action Analysis: Key Technical Levels and Momentum Signals

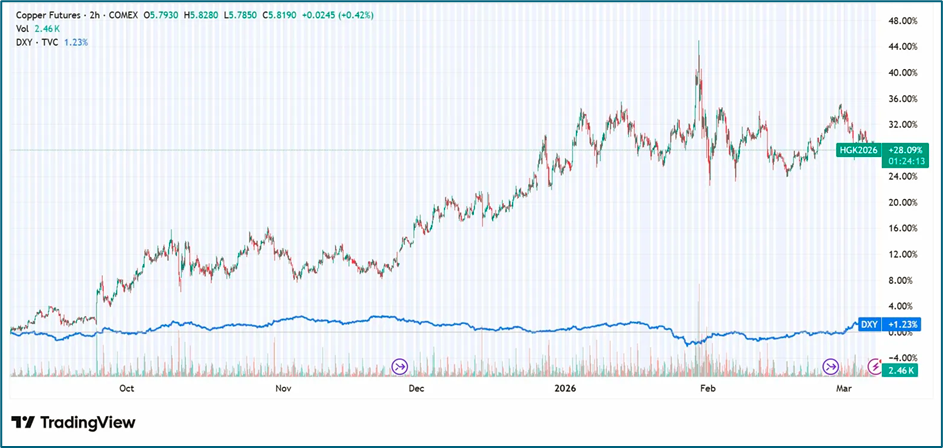

Figure 2: Copper Prices vs US Dollar Index (DXY), Source: tradingview.com

Price Trend Structure

Based on recent price action visible in the TradingView chart, copper futures experienced a sharp rally earlier in the year before entering a period of consolidation and heightened volatility.

A notable spike occurred in early February, followed by a rapid correction that pushed prices back into a broader trading range. Since then, copper has oscillated between approximately $5.45 and $5.95 per pound.

The recent rebound toward $5.80 suggests that buyers are attempting to stabilize the market near the middle of this range.

Support and Resistance Levels

Key support levels currently appear near:

- $5.45per pound

• $5.30 per pound

Resistance zones are visible around:

- $5.95 per pound

• $6.00 per pound

A sustained breakout above the $6.00 level could signal renewed bullish momentum and potentially trigger another leg higher.

Moving Average Structure

Short term price action appears to be fluctuating around the 21 day exponential moving average, indicating short term indecision among traders.

The 50 day moving average remains upward sloping, reflecting the strong rally that began in late 2025.

Meanwhile, the 200 day moving average continues to trend higher, confirming that the broader long term trend remains structurally bullish.

Momentum Indicators

Relative Strength Index readings appear to have cooled from overbought territory earlier in the quarter, suggesting that the market has entered a consolidation phase rather than a full trend reversal.

The MACD indicator likely reflects a weakening of bullish momentum during the recent pullback, though the signal line appears close to stabilization.

Volume Trends

Trading volume during the recent decline has not dramatically exceeded the 10 day and 30 day averages, indicating that the correction may represent a temporary pause rather than aggressive liquidation.

Overall, the technical structure suggests that copper remains in a consolidation pattern following a strong rally.

Long Term Copper Investment Strategy: Structural Demand Drivers Remain Intact

Despite near term uncertainty, the long term demand outlook for copper remains among the most compelling in the commodities sector.

The global transition toward electrification continues to create structural demand growth across several industries.

Electric vehicles require significantly more copper than traditional internal combustion vehicles. Renewable energy infrastructure such as wind turbines and solar farms relies heavily on copper wiring. Grid modernization efforts are also expanding copper usage as countries upgrade electricity networks to accommodate rising power demand.

Another emerging source of demand comes from artificial intelligence infrastructure.

Large scale data centres powering cloud computing and AI models require extensive electrical connectivity and cooling systems, both of which are copper intensive. Analysts estimate that AI data centre expansion alone could add hundreds of thousands of tonnes of incremental copper demand annually.

This structural demand growth contrasts sharply with the limited pace of new mine development globally, reinforcing expectations of tighter supply conditions over the coming decade.

Conclusion: Copper Balances Short Term Macro Risks with Strong Structural Demand

Copper’s recent volatility reflects the complex intersection of global macro forces and long term industrial demand trends.

Geopolitical tensions in the Middle East, rising oil prices, and a stronger US dollar have created short term headwinds for the metal. At the same time, slower Chinese growth expectations have added uncertainty to the demand outlook.

Yet the underlying structural narrative for copper remains intact.

Supply constraints, electrification trends, and expanding digital infrastructure continue to support a bullish long term investment thesis. For investors, the key question is not whether copper demand will grow, but how quickly global macro conditions will allow that growth story to translate into sustained price gains.

FAQs

Why are copper prices volatile in 2026?

Copper prices are experiencing volatility due to geopolitical tensions, rising oil prices, shifting inflation expectations, and uncertainty surrounding global economic growth, particularly in China.

How does the US dollar influence copper prices?

Copper is priced in US dollars globally. When the dollar strengthens, copper becomes more expensive for international buyers, which often reduces demand and places downward pressure on prices.

Why is China critical for the copper market?

China accounts for more than half of global copper consumption, driven by its construction, infrastructure, manufacturing, and renewable energy sectors. Changes in Chinese economic growth therefore significantly influence global copper demand.

What role do data centres play in copper demand?

The rapid expansion of AI and cloud computing infrastructure requires extensive electrical systems and cooling networks. These systems rely heavily on copper wiring, making data centres an increasingly important source of copper demand.

What is the long term outlook for copper prices?

Most analysts expect copper demand to grow due to electrification, renewable energy expansion, and digital infrastructure development. Combined with constrained mine supply, these trends support a positive long term price outlook.

_06_12_2026_23_00_13_327450.jpg)

Please wait processing your request...

Please wait processing your request...