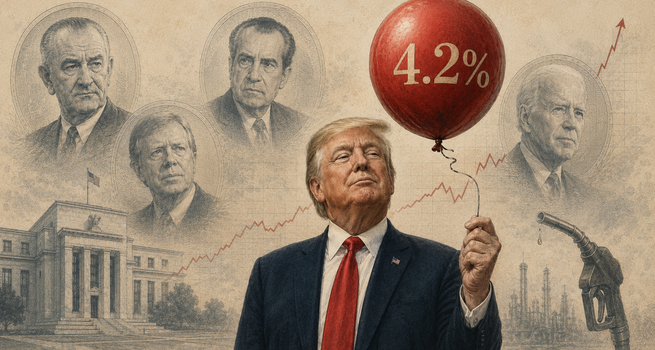

Trump celebrated May's 4.2% CPI print, a three-year high, predicting the Iran war's end will break inflation. History, from Nixon's wage-price spiral to Biden's transitory miscall, offers a sharply different verdict.

Key Highlights

- US headline CPI rose 4.2% annually in May 2026, a three-year high, with a 23.5% energy surge accounting for over 60% of the monthly increase.

- Core CPI came in at 2.9% annually and 0.2% monthly, below consensus, signalling that broad-based price pressure remains contained.

- Trump's "war ends, inflation falls" thesis repeats a structural error seen across four administrations: anchoring disinflation to one resolvable event while inflation quietly embeds into wages, services, and expectations.

- The Federal Reserve holds rates at 3.50 to 3.75%, with futures pricing zero cuts in 2026 and a new inflation-hawk chair taking the helm at the June 16 to 17 FOMC meeting.

- Republican lawmakers face material electoral risk heading into November, with every historical midterm above 4% CPI producing meaningful seat losses for the incumbent party.

An Oval Office Moment and What It Signals

"I love the inflation. You know why?", Donald Trump, Oval Office, June 10, 2026.

That question, posed to reporters after the Bureau of Labor Statistics confirmed US CPI at 4.2% year-over-year in May, went unanswered in any meaningful macroeconomic sense. The president's explanation, that the war with Iran is driving oil prices higher and that once the conflict ends inflation will come down "like a rock," is not an answer. It is a forecast architecture with a name: the Exogenous Fix Fallacy.

The Exogenous Fix Fallacy is the recurring presidential tendency to anchor disinflation expectations to one resolvable event, while the inflation already seeded by that event continues to migrate through freight costs, food prices, services pricing, and wage expectations. History has tested this thesis repeatedly. It has a poor track record. And the conditions under which it fails most severely are present in the current macro environment.

Reading the Data Correctly

Before the historical parallels, the data requires honest interpretation. The May print is not uniformly alarming, and intellectual honesty demands that be stated clearly.

While headline CPI rose 0.5% on a monthly basis, core commodities prices actually declined 0.1%. Energy prices jumped 3.9% for the month, accounting for over 60% of the overall CPI increase. Shelter costs, a closely watched component for Federal Reserve policymakers, rose 0.3% for the month, a meaningful deceleration from the 0.6% recorded in April. Services excluding energy services rose just 0.3%, down from 0.5% in April. Transportation services fell 0.6%.

The underlying structure of this inflation report is that of a supply shock, not a demand spiral. Core inflation is, for now, behaving. That is the analytically honest read.

But behavioural restraint in core inflation is conditional. It holds as long as energy inflation does not stay elevated long enough to reset wage and services expectations. Morgan Stanley's chief economic strategist noted that while numbers were not as bad as some feared, inflation remains well above target, with higher oil prices, AI-induced cost pressures, and tariffs creating a multi-variable environment the Fed must navigate carefully. That multi-variable point is precisely where the president's single-variable thesis is weakest. Removing the Iran war shock does not automatically reset tariff-driven goods inflation, AI demand pressures, or the shelter costs that have been structurally elevated for three years.

The Four Historical Traps

Trap One: Biden's Transitory Call, 2021

The most structurally identical precedent is recent. In 2021, the Biden administration and the Federal Reserve characterised post-COVID inflation as transitory, anchored to supply chain normalisation. The logic was internally coherent: remove the exogenous shock, prices normalise. CPI hit 9.1% by June 2022 before decisive action was taken.

Trump's formulation follows the same architecture: end the war, remove the oil shock, watch inflation fall. What neither framework accounts for is the transmission lag. Energy inflation, if sustained long enough, passes through to freight, food, services, and wage expectations. By the time the exogenous shock resolves, the inflation it seeded has already migrated into broader price structures. The shock ends. The inflation does not.

Trap Two: Nixon's Pre-Election Dismissal, 1971 to 1972

Nixon's suppression of inflation concern before the 1972 election, including direct political pressure on the Federal Reserve to keep monetary conditions loose, produced short-term political calm and long-term structural damage. Wage-price controls were imposed and ultimately failed to contain the underlying pressure. The 1973 oil shock then hit an economy whose inflation defences had already been weakened by a period of deliberate complacency.

The result was a decade of stagflation that consumed two presidencies. The political calculus of declaring inflation benign ahead of an electoral cycle is not new. Neither are its consequences.

Trap Three: Johnson's Wartime Fiscal Overextension, 1965 to 1968

The Vietnam War, layered atop Great Society spending commitments, produced a fiscal structure incapable of absorbing an external shock without systemic price escalation. Federal outlays rose from $118 billion in fiscal 1965 to $178 billion by fiscal 1968, a 51% increase in three years, while the budget deficit widened from $1.4 billion to $25.2 billion over the same period. A government conducting a war on a structurally deteriorating fiscal balance sheet has limited shock-absorption capacity.

The Iran conflict is arriving in an environment of elevated US federal debt, tariff-driven goods inflation, and a labour market adding 172,000 jobs per month. The fiscal stress-multiplier that made LBJ's inflation so persistent is not absent from the current picture. Wars do not merely raise energy prices. They stress entire fiscal frameworks, and the inflationary tail of that stress outlasts the conflict itself.

Trap Four: Carter's Expectations Trap, 1979 to 1980

The 1979 Iranian Revolution cut global oil supply, drove CPI above 13%, and ultimately required the Federal Reserve under Paul Volcker to raise rates to 20% to break embedded inflation expectations. The critical lesson from the Carter period is not the scale of the shock. It is what the shock became over time.

Oil-driven inflation which runs long enough stops being energy inflation. It becomes generalised inflation, as businesses and workers reprice forward on the assumption that elevated costs are permanent. Once that repricing is underway, removing the original oil shock does not reverse it. Trump's prediction that inflation will sharply reverse once the Iran war ends assumes inflation expectations remain anchored throughout the conflict. That assumption has a weak historical foundation.

What the History Means for Today

The four historical traps are not isolated lessons. They form a chain of escalating risk conditions, each one compounding the next. Taken in sequence, they define the present moment more precisely than any single parallel can.

BIDEN: The Lag Is Already Running

The transmission lag is not a future risk. It is a current process. Energy inflation at 23.5% annually has been running for several months. The pass-through to freight contracts, food input costs, and services repricing is already underway. Whether it reverses depends not on when the Iran war ends but on how much of that repricing has already become embedded in business cost structures and wage negotiations. That question will take months of data to answer, well after the geopolitical moment has passed.

JOHNSON: The Fiscal Buffer Is Gone

The transmission lag is operating inside a fiscal framework that provides limited shock-absorption capacity. The United States is not conducting this war from a position of surplus. Tariffs, defence commitments, and structural entitlement spending mean the balance sheet entering this conflict is already under strain. The multiplier that amplified LBJ's inflation does not require a replay of the Great Society. It requires only that the fiscal framework remain stretched while the energy shock persists.

CARTER: Expectations Do Not Hold Forever

Core inflation at 2.9% annually is the single most important data point in the May report. It means the Carter scenario has not yet arrived. But inflation expectations are not fixed. They are shaped continuously by what households and firms observe. A president publicly celebrating 4.2% headline inflation while questioning the need for monetary restraint is an input into how businesses and workers set prices and wages going forward. The window between supply shock and generalised inflation is not permanently open.

NIXON: The Electoral Bet Has a Long Fuse

Declaring inflation benign before an electoral cycle produces short-term political calm by design. The structural damage arrives later, when the weaknesses created by complacency meet the next shock. Nixon's dismissal in 1971 took two years to reach its consequences. The "I love inflation" soundbite is already in circulation seven months before the midterms. The fuse is shorter this time.

The Standard the Current Moment Requires

The three conditions above share one common feature: none of them are under monetary control. The lag is already running. The fiscal buffer is gone. Expectations are live and shapeable. These are the constraints. What remains is the question of whether the administration chooses to work within them or against them. History offers one instructive answer.

Reagan did not architect the disinflation. Volcker's appointment was Carter's, and the cycle was already underway when Reagan took office. His fiscal deficits complicated the picture further. What he did that mattered was narrower: when unemployment hit 10.8% in late 1982 and electoral losses were mounting, he did not force Volcker to ease. He gave the institution the space to finish what it had started.

That is the precise capability the current moment requires. The Fed cannot control oil prices, end the war, or reverse tariffs. What it can do, if given that same institutional space, is defend expectations before the tipping point is reached. That is the only lever the current administration still holds. Whether it is extended is a decision made in the Oval Office, not the FOMC.

The Federal Reserve's Constrained Position

The June 16 to 17 FOMC meeting will be the first under Warsh, a known inflation hawk who has written critically about the risks of central bank credibility erosion. The analytical tension is not trivial. Central bank credibility, the degree to which households and firms believe the Fed will defend its 2% target, is itself an anti-inflation tool. When political signals undermine that credibility, the Fed must work harder, and at higher cost to growth, to produce the same anchoring effect.

The immediate decision is a near-certain hold at the 3.50 to 3.75% target range. Goldman Sachs has shifted expectations toward no rate cuts in 2026, with possible removal of easing bias language at the June meeting. The structural constraint, however, is more important than the meeting outcome. The Fed cannot fight a war-driven oil shock with rate hikes without triggering a demand recession. If energy inflation embeds into wages and services pricing, the central bank faces a choice between accepting above-target inflation and engineering a deliberate slowdown. Oxford Economics has noted that May could represent the CPI peak if gas prices remain lower in June, but that core inflation is likely to stay elevated regardless.

The operative variable is geopolitical, not monetary. The Federal Reserve does not control it. The president who does control it has declared he loves the current outcome.

The Political Arithmetic

Consumer inflation expectations are a stronger predictor of electoral outcomes than actual CPI readings, and Republicans defending slim majorities in both chambers understand this. Every historical midterm in which the incumbent party faced headline CPI above 4% produced meaningful seat losses. The "I love inflation" clip is already in Democratic circulation and will not leave the political environment before November. For a party whose congressional majority rests on a handful of competitive districts, a soundbite that equates presidential indifference with household pain carries material electoral cost regardless of what the core CPI data actually shows.

Conclusion

Trump's thesis may yet prove correct. The Iran conflict may end. Oil prices may fall. Core inflation may stay contained. That window remains open, and the May data does not close it.

But the Exogenous Fix Fallacy has a poor historical base rate, and the conditions under which it fails most severely are present: a fiscally stretched government, a multi-variable inflation environment, a new Fed chair whose credibility depends on demonstrating institutional independence, and an electorate that experiences inflation through fuel costs and grocery bills rather than index readings.

History does not reward declarations. It rewards the discipline to let institutions work, absorb the short-term cost, and let the data do the talking over time. That is what Reagan, in the narrow but important sense, understood. It is what Nixon, Johnson, and Biden, each in their own way, did not.

The cure for "I love inflation" has never been a soundbite. It has always been time, institutional credibility, and the willingness to absorb the price of getting it right. History is watching to see which of those this administration is prepared to provide.

Please wait processing your request...

Please wait processing your request...