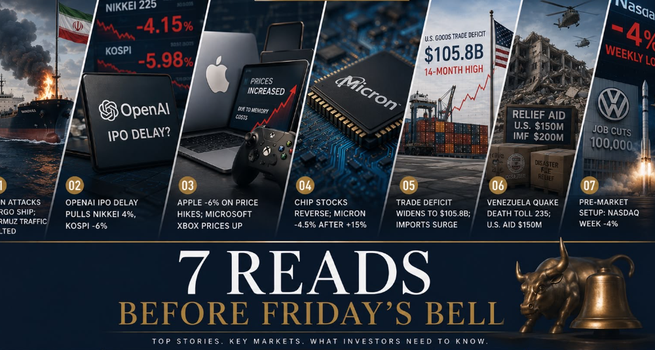

Iran attacked a Singapore-flagged cargo ship in the Strait of Hormuz, halting shipping and pushing WTI back below $70 after Thursday's wartime-premium unwind. A report that OpenAI is considering delaying its IPO sent SoftBank lower and pulled the Nikkei 225 down more than 4%; the Nasdaq is on track for a 4% weekly loss. Apple tumbled more than 6% Thursday on iPad and MacBook price hikes citing surging memory costs.

- IRAN/HORMUZ: Iran Attacks Singapore-Flagged Cargo Ship; Strait Shipping Halted; IMO Pauses Sailor Evacuation; WTI Falls Back Below $70

Iran attacked a Singapore-flagged cargo ship in the Strait of Hormuz, halting shipping in the waterway and directly challenging the MOU's toll-free passage provision signed at Versailles less than 2 weeks ago. The UN's International Maritime Organisation paused its plans to evacuate sailors stranded in the strait following the attack. Iran had earlier warned ships only to use routes it had approved, a position Rubio had explicitly rejected earlier this week. WTI trades at $69.55 (-3.30%) and Brent at $72.50 (-3.67%) pre-market, resuming losses after Thursday's brief recovery.

- The attack converts Iran's verbal warnings about unapproved transit into a physical enforcement action, making the Rubio red line a live test of U.S. deterrence credibility within the 60-day negotiating window.

- Shipping halted in Hormuz is an operational event that affects tanker scheduling, insurance rates, and LNG routing with immediate real-world consequences independent of where WTI settles.

- Risk note: if Iran escalates from a single cargo ship attack to broader interdiction of Hormuz traffic before the next formal negotiating session, the entire MOU framework comes under question and oil reprices sharply above $80.

- OPENAI: IPO Delay Report Pulls Nikkei Down 4%, KOSPI -6%; Trump Administration Gates GPT 5.6 to Government-Approved Partners

A report that OpenAI is considering delaying its IPO sent SoftBank lower, pulling the Nikkei 225 down more than 4% as investors repriced the Japanese conglomerate's AI lab exposure. South Korea's KOSPI dropped nearly 6%, led by Samsung Electronics and SK Hynix. Separately, the Trump administration asked OpenAI to restrict GPT 5.6 to a handful of government-vetted partners before any full public rollout, framing the request as an effort to make America the gatekeeper for frontier AI model releases. Chip stocks are lower across the board pre-market Friday, with the OpenAI delay report adding a sentiment layer on top of the Apple and Microsoft memory-cost selloff from Thursday.

- SoftBank's Nikkei-level influence means an OpenAI IPO delay reprices not just one stock but Japan's benchmark index; the concentration of a single AI investment in a major market index is the systemic risk the delay exposes.

- The GPT 5.6 government-gating request is structurally significant: if extended to other frontier labs, it inserts a federal approval layer into every major AI model release, changing the competitive dynamics between U.S. and non-U.S. AI developers.

- Risk note: if the IPO delay is confirmed as a formal decision, Anthropic and other AI labs that have signalled IPO intentions face a recalibrated market reception regardless of their own financial performance.

- APPLE/MICROSOFT: Apple -6% on iPad and MacBook Price Hikes; Microsoft -3.5% on Xbox Hikes; Both Cite Memory Costs; AI Chip Shortage Reaches Consumer Electronics

Apple (NASDAQ: AAPL) tumbled more than 6% Thursday, its worst single-day decline in more than a year, after announcing price hikes on iPads and MacBooks citing surging memory and storage costs; the stock is rebounding 0.5% pre-market Friday. Microsoft (NASDAQ: MSFT) shed 3.5% after raising prices on Xbox consoles, also citing soaring component costs. Both companies explicitly named memory as the driver, connecting the AI infrastructure buildout directly to consumer hardware pricing in a single session. The Nasdaq notched its fourth straight losing day Thursday, its longest such streak since February; the index is on track to close the week more than 4% lower.

- Apple and Microsoft pricing the same memory cost shock into consumer hardware on the same day establishes a category-level precedent: AI data center demand is now visibly taxing consumer electronics margins and being passed to end buyers.

- The Nasdaq's fourth straight loss combined with the largest market cap names announcing price hikes signals the AI infrastructure cycle has entered a phase where its costs are becoming broadly visible.

- Risk note: if consumers defer iPad and Xbox purchases in response to the price hikes, the revenue impact on Apple and Microsoft compounds the margin pressure rather than relieving it.

- CHIPS REVERSAL: Micron -4.5% After Thursday's +15%; Arm -4%, AMD -3.5%, Intel -3%; On Semi -15% on $7B Synaptics Acquisition

The memory and semiconductor complex is reversing Thursday's Micron-driven surge. Micron Technology (NASDAQ: MU) is down more than 4.5% pre-market after jumping nearly 16% on Thursday; Sandisk fell the same amount, Seagate Technology and Western Digital each declined about 3.5%. The broader selloff extends across the sector: Arm Holdings (NASDAQ: ARM) and Marvell Technology (NASDAQ: MRVL) both down about 4%, Advanced Micro Devices (NASDAQ: AMD) off 3.5%, Intel (NASDAQ: INTC) down 3%, Broadcom off 1.5%. On Semiconductor (NASDAQ: ON) is the session's largest decliner, falling more than 15% after announcing an all-stock acquisition of Synaptics at nearly $7 billion, its largest deal ever; the company estimates the deal expands its total addressable market by $30 billion. Synaptics rose 2.5%.

- Micron's 4.5% pre-market reversal after a 16% single-day gain is technically orderly, but the OpenAI IPO delay report is adding a sentiment layer on top of the normal post-earnings giveback.

- On Semi's -15% reaction to its largest-ever acquisition reflects market scepticism about all-stock deal premiums in a high-rate environment; the $30 billion TAM expansion argument requires years of execution to validate.

- Risk note: if the OpenAI IPO delay is confirmed, the AI infrastructure investment thesis faces a confidence shock that extends the chip sector's four-day losing streak into next week.

- TRADE DATA: Goods Deficit Widens to $105.8B, 14-Month High; Imports Rise to $313.4B Despite Tariffs; Exports Fall 5.4%

The U.S. goods trade deficit widened to $105.8 billion in May from $83 billion in April, the widest gap in over a year and sharply missing the $85 billion forecast. Imports rose 3.6% to $313.4 billion, the highest level in 14 months despite the tariff regime; consumer goods imports rose 5.7% to $59.5 billion, industrial supplies 4.8% to $55.9 billion. Exports fell 5.4% to $207.7 billion, with industrial supplies declining 7% to $82.7 billion and consumer goods exports falling 9.2% to $20.7 billion. Wholesale inventories rose 0.3% to $943.9 billion in May, a fourth consecutive monthly increase, beating the 0.2% forecast.

- Imports rising to a 14-month high despite tariffs directly contradicts the stated policy objective; the $105.8 billion deficit against an $85 billion forecast is the largest single-month miss in recent data.

- Exports falling 5.4% while imports rise 3.6% in the same month is a simultaneous deterioration on both sides of the trade account, pointing to domestic demand absorbing foreign goods faster than U.S. producers can expand foreign sales.

- Risk note: if the May trade pattern persists into June, the current account deterioration becomes a quarterly-level story that complicates the dollar's near-term path and adds to inflationary pressure via import prices.

- VENEZUELA: Earthquake Death Toll 235; U.S. Sends Multi-Agency Task Force and $150M; IMF Commits $200M; USAID Gap Complicates Relief

The confirmed death toll from Wednesday's earthquakes in Venezuela reached 235, with rescuers continuing to search through rubble of hundreds of collapsed buildings. The 2 quakes were Venezuela's largest and possibly deadliest in over a century. The Trump administration is sending a multi-agency task force coordinated by the State Department with a $150 million assistance programme; 2 navy ships and transport planes are already en route. The IMF committed $200 million to rebuild infrastructure. Critics noted that the dismantling of USAID, which previously led most international disaster responses, has complicated relief coordination.

- The $150 million U.S. programme and the $200 million IMF commitment together represent a $350 million initial relief package for a country whose infrastructure was already severely strained before the earthquakes.

- The USAID gap is the operational story beneath the headline numbers: the agency that coordinated logistics, local partnerships, and supply chains for disaster response no longer exists at its prior capacity.

- Risk note: Venezuela's political situation under acting president Delcy Rodriguez introduces governance uncertainty into the relief distribution process; misallocation of international aid funds in a politically contested environment is a documented risk in prior Venezuela crises.

- PRE-MARKET SETUP: DJIA +0.14% Thursday; Nasdaq Week -4%; Rocket Lab +1.5% on NASA Contracts; VW Reports 100K Job Cuts; Energy Stocks Lower

Thursday closed mixed: DJIA +0.14% at 51,920.62, S&P 500 -0.01% at 7,357.49, NASDAQ -0.47% at 25,358. The Nasdaq is on track to close the week more than 4% lower. Rocket Lab (NASDAQ: RKLB) rose 1.5% pre-market after NASA awarded it launch contracts for 2 missions: a Sun energy input research mission and an ice cloud study. Energy stocks are lower as oil drops back below $70: APA Corporation -1.5%, Diamondback Energy -1%, Constellation Energy and Occidental Petroleum both off 1%. German media reports Volkswagen is planning to cut up to 100,000 jobs, double prior estimates, and shut factories; VW has not confirmed; unions have vowed to fight, citing Chinese competition and Trump tariffs as the demand headwinds.

- Rocket Lab's dual NASA contract win positions it as the operational alternative to SpaceX for government science missions, a market that becomes more accessible as SpaceX's post-IPO valuation rises above government contract economics.

- Volkswagen's reported 100,000 job cut figure, if confirmed, would be one of the largest single-company workforce reductions in European industrial history; Chinese EV competition combined with U.S. tariffs represents a structural rather than cyclical demand problem.

- Risk note: energy stocks declining on oil's return below $70 while Hormuz shipping is halted creates a contradiction; if the Hormuz disruption persists, oil rebounds sharply and today's pre-market energy moves become a fade.

_06_27_2026_21_16_35_168117.jpg)

Please wait processing your request...

Please wait processing your request...