Key Highlights

- Sulfur prices have reached record highs as Middle East disruptions choke supply routes

- The Persian Gulf accounts for nearly half of global sulfur exports

- Fertilizer production faces constraints ahead of peak planting season

- Industrial demand from mining and semiconductors is intensifying competition

- Tight inventories are amplifying the risk of broader commodity inflation

A Quiet Commodity Moves to the Center of Global Markets

Commodity markets often reveal their importance only in moments of disruption. Sulfur, long treated as an abundant industrial by-product, has abruptly emerged as a critical pressure point in global supply chains. A sharp price surge driven by geopolitical tensions in the Middle East is now rippling across agriculture, mining, and technology sectors.

What makes the current episode notable is not only the scale of the price move, but the structural vulnerabilities it has exposed. Sulfur is not mined in response to demand. It is recovered through refining processes tied to oil and gas production. This dependency creates a rigid supply system that struggles to respond when disruptions occur.

The result is a market shock with implications far beyond a single commodity. As prices surge past record levels, sulfur is revealing how deeply interconnected modern industrial systems have become.

Global Commodity Market Trends: The Cost of Geographic Concentration

The sulfur market reflects a broader pattern seen across global commodities. Supply chains have become increasingly concentrated in regions offering cost efficiency and scale. In sulfur’s case, that concentration is firmly anchored in the Persian Gulf.

Countries such as Saudi Arabia and the United Arab Emirates dominate export volumes due to their extensive refining infrastructure. This concentration has historically supported stable pricing and reliable supply. However, it has also embedded systemic risk.

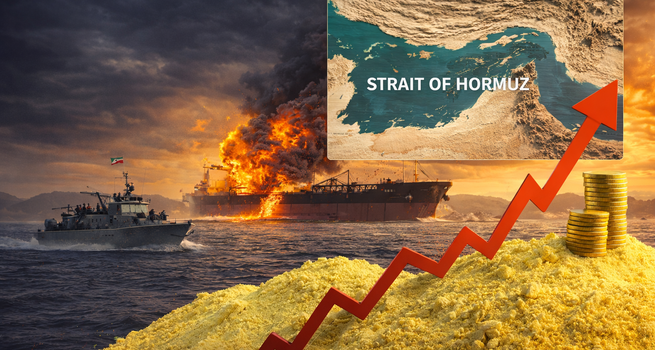

Approximately 40 to 45 percent of global sulfur exports transit through the Strait of Hormuz. This narrow shipping corridor has now become a critical vulnerability. Disruptions in this region have an immediate and disproportionate impact on global availability.

Import-dependent economies such as China, India, and Morocco have built procurement strategies around Gulf supply. These strategies assumed continuity. The current disruption has challenged that assumption, forcing markets to confront the limits of geographic concentration.

Industrial Supply Chain Analysis: From By-Product to Strategic Input

Sulfur occupies a unique position in industrial ecosystems. Unlike metals or energy commodities, it is not produced independently. Its availability is tied to refining throughput, which is itself influenced by energy demand rather than sulfur demand.

This structural characteristic creates a mismatch between supply and consumption dynamics. When demand rises in downstream industries, sulfur supply cannot adjust quickly. Conversely, supply shocks cannot be offset through increased production.

The critical transformation step lies in sulfuric acid production. Sulfur is converted into sulfuric acid, which serves as a foundational input across multiple sectors.

In agriculture, sulfuric acid is essential for producing phosphate fertilizers. These fertilizers underpin global crop yields, particularly for staple crops such as corn, wheat, and soybeans.

In mining, sulfuric acid enables the extraction of copper, nickel, and cobalt from lower-grade ores. These metals are central to electrification and battery supply chains.

In semiconductors, high-purity sulfuric acid is used in wafer cleaning processes. This connects sulfur directly to advanced manufacturing and digital infrastructure.

These overlapping demand channels create a competitive environment where sectors with very different economic profiles compete for the same constrained input.

Fertilizer Market Impact: A Timing Problem with Systemic Consequences

The agricultural implications of sulfur disruption are particularly acute due to timing. Fertilizer demand is highly seasonal, with the northern hemisphere planting season representing a critical procurement window.

Phosphate fertilizer production depends directly on sulfuric acid. Any disruption in sulfur supply translates quickly into reduced fertilizer output. Producers have already begun adjusting operations in response to rising input costs and limited availability.

The consequence is a tightening supply environment just as farmers prepare for planting. Unlike other inputs, fertilizer shortages cannot be easily deferred. Crop yields are determined during planting, not after.

This creates a direct transmission mechanism from sulfur markets to food prices. Rising fertilizer costs increase farm input expenses, which are eventually reflected in agricultural commodity pricing.

Given the scale of global food systems, even modest disruptions can have outsized effects on inflation and food security.

Mining and Technology Sector Pressures: Competing for Scarce Inputs

While agriculture dominates the immediate narrative, other sectors are equally exposed. Mining operations, particularly those focused on copper and nickel, rely heavily on sulfuric acid for leaching processes.

Demand for these metals has been rising due to electrification and energy transition initiatives. This has already placed upward pressure on sulfur consumption prior to the current disruption.

At the same time, semiconductor manufacturing introduces a high-value demand segment. Chip fabrication requires ultra-pure chemicals, including sulfuric acid, for precision cleaning processes.

The convergence of these industries creates a structural imbalance. Supply was not designed to accommodate simultaneous growth across agriculture, mining, and technology.

As a result, allocation decisions are becoming more complex. Higher-value industries may outbid agricultural users, intensifying supply constraints in food production.

Market Dynamics and Pricing: China’s Central Role

China plays a pivotal role in shaping sulfur market dynamics. As the world’s largest importer, it effectively sets the marginal price through its procurement activity.

This explains why sulfur futures are often priced in yuan. Chinese demand patterns influence global inventory cycles and price signals.

When disruptions occur, price movements typically emerge first in Chinese markets before spreading globally. This pattern is evident in the current surge, where futures have reached unprecedented levels.

Compounding the situation are policy factors. China has implemented export controls on sulfur to prioritize domestic industrial needs. This has reduced the volume available to international markets.

At the same time, Russian supply has been constrained by sanctions and logistical challenges. These factors have tightened global supply even before the Middle East disruption.

Inventory Dynamics: Thin Buffers Amplify Volatility

Commodity markets rely on inventory buffers to absorb shocks. In the sulfur market, these buffers were already limited prior to the current disruption.

Years of efficient supply chains and just-in-time procurement have reduced the need for large stockpiles. While this improves cost efficiency, it increases vulnerability to disruption.

With inventories already thin, the current supply shock has triggered a sharp price response. Market participants are now competing for limited available volumes, driving further volatility.

Estimates suggest that inventory depletion could become critical within weeks if supply disruptions persist. This creates a feedback loop where rising prices encourage hoarding, further tightening availability.

Investment Strategy and Market Implications

For investors, the sulfur shock offers several important signals. First, it highlights the importance of supply chain resilience in commodity markets. Concentration risk is increasingly being priced into valuations.

Second, it underscores the interconnected nature of modern industries. A disruption in a relatively obscure commodity can have cascading effects across sectors.

Third, it points to inflationary pressures that may extend beyond traditional energy markets. Fertilizer and food prices are likely to reflect the impact of sustained sulfur shortages.

Equity markets may respond unevenly. Fertilizer producers with secure supply chains could benefit from higher prices. Conversely, industries reliant on sulfur inputs may face margin compression.

From a strategic perspective, diversification of supply sources and investment in alternative production pathways may become priorities for both companies and policymakers.

Strategic Outlook: Structural Adjustments Ahead

Looking forward, the sulfur market is unlikely to return quickly to previous equilibrium. The current disruption has exposed structural weaknesses that will take time to address.

Potential responses include increased investment in alternative supply regions such as Canada and Central Asia. However, scaling these sources will require significant capital and time.

Another avenue lies in improving recycling and recovery technologies. While promising, these solutions are not yet capable of offsetting large-scale supply disruptions.

Geopolitical considerations will also play a central role. Stability in the Middle East remains a key determinant of supply continuity.

More broadly, the episode may prompt a reassessment of global supply chain design. Efficiency has long been the dominant objective. Resilience is now emerging as an equally critical priority.

Conclusion: A Small Commodity with Systemic Importance

The sulfur price surge is more than a temporary market anomaly. It is a reflection of deeper structural tensions within global supply chains.

By linking agriculture, mining, and technology, sulfur has become a focal point for understanding how interconnected modern economies have become. Disruptions in one region can now propagate rapidly across multiple sectors.

For investors and policymakers alike, the lesson is clear. Commodities that appear peripheral can hold systemic importance. Ignoring them can lead to unexpected and far-reaching consequences.

Please wait processing your request...

Please wait processing your request...