Summary

- UBS raised its price target on construction firm Flour to US$47, as it believes that Flour’s potential has been underappreciated by investors.

- As per data available on EODHD/Others, FLR has a mean recommendation rating of 2.3 on five and a consensus mean price target of US$42.

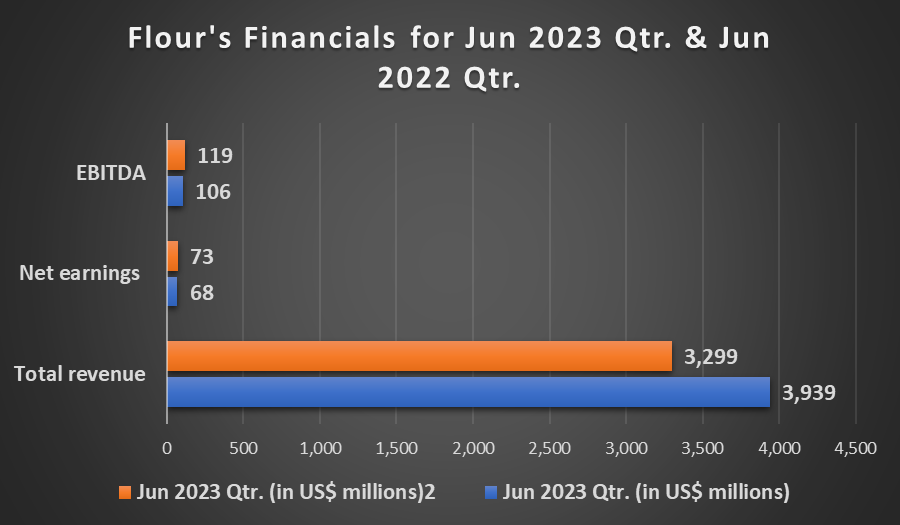

- Flour reported US$3.9 billion in revenue for Q2 2023.

Broker UBS raised its rating on Flour Corp. (NYSE: FLR), to ‘buy’ from ‘neutral’. UBS elevated its price target on the construction firm by US$12 to US$47, which marks an upside potential of 36% over FLR’s closing price on Wednesday.

UBS believes that Flour’s potential has been underappreciated by investors, leading the broker to up its rating and price target on FLR.

Fluor is a leading engineering and construction services provider. Its clientele spans diverse industries such as energy, mining, chemicals, metals, and transportation.

As per data available on EODHD/Others, FLR has a mean recommendation rating of 2.3 on five. Here, one indicates a ‘strong buy’ rating and five stands for a ‘strong sell’ rating. The consensus mean price target on FLR stands at US$42, a potential increase of 18% over Wednesday’s closing price.

FLR Price Chart; Source: EODHD/Others

FLR closed at US$35.46 on Wednesday, October 4, 2023.

UBS analyst states that Flour has reached an inflection point

According to UBS analyst Steven Fisher, Fluor has reached a turning point regarding concerns about legacy risks and is nearing a point where it may return to margins that are closer to or even better than what is considered normal. This improvement comes after experiencing several years of below-average performance, and there is additional potential for growth due to positive cash flow.

Flour’s adjusted EBITDA is expected to grow by 41% from 2023-2025. The growth was majorly caused by 160 basis points of margin expansion.

The broker also mentioned that FLR currently possesses a promising lineup of potential opportunities compared to previous years, with both greater quantity and higher quality prospects. This positive outlook is underpinned by a strong array of available opportunities.

Flour is expected to see increased prospects in chemicals, mining and metals, data centers and even the government, as per UBS.

Flour Reports increased revenue in Q2 2023

In Q2 2023, the company reported US$3.9 billion in revenue, with net earnings attributed to Fluor amounting to US$61 million, equivalent to US$0.35 per diluted share.

The total segment profit for the quarter was US$191 million, showing an improvement from the US$108 million profit recorded in the second quarter of 2022.

Image Source: ©2023 Kalkine®; Data Source: Company Reports

The company believes that the favorable outcomes in this quarter further validate their strategic path and affirm the robust demand for their engineering and construction services.

Additionally, the company expects to be on the verge of a turning point that will lead to the creation of greater value for shareholders. Fluor raised its annual adjusted diluted earnings per share (EPS) outlook from US$1.50 to US$1.90 to a new range of US$2.00 to US$2.30.

Additionally, Flour is upgrading its annual adjusted EBITDA guidance, narrowing it down from the previous range of US$450 to US$600 million to a revised range of US$500 to US$600 million.

Please wait processing your request...

Please wait processing your request...