Key Highlights

- 33% Dividend Yield — One of the highest yields among S&P 500 blue-chip stocks, with a quarterly payout of $1.64/share ($6.56 annualized), more than 4x the S&P 500 average yield.

- 'Better Not Bigger' Strategy — CEO Carol Tome's margin-focused approach is driving operating efficiency, automation investments, and a shift toward high-value healthcare logistics — reducing dependence on low-margin volume.

- Discounted Valuation — Trading at a P/E of 15.80x and well below its 52-week high of $122.41, UPS offers a potentially compelling entry point for value-oriented income investors.

As inflationary pressures and market volatility reshape investor priorities, income-seeking investors are increasingly turning to dividend-paying stocks for stability and predictable cash flow. United Parcel Service, Inc. (NYSE:UPS) has long been regarded as one of the most dependable dividend payers in the S&P 500 — currently offering a dividend yield of approximately 6.33%, placing it among the highest-yielding blue-chip stocks in the index. This comprehensive article examines UPS through the lens of an income shareholder, covering the company's overview, recent stock performance, financial fundamentals, dividend history, management guidance, and frequently asked questions.

Company Overview

Founded in 1907 and headquartered in Atlanta, Georgia, United Parcel Service is the world's largest package delivery company and a leading provider of supply chain management solutions. With operations spanning more than 220 countries and territories, UPS delivers over 25 million packages and documents per day. The company operates through three core business segments: U.S. Domestic Package, International Package, and Supply Chain Solutions.

UPS's global network encompasses approximately 127,000 delivery vehicles, a fleet of over 570 aircraft, and a workforce of roughly 500,000 employees worldwide. The company serves both business-to-business (B2B) and business-to-consumer (B2C) markets, with e-commerce fulfillment representing a growing share of volume.

In recent years, UPS has pursued a 'better not bigger' strategy under CEO Carol Tome, focusing on improving profit margins by prioritizing high-value, high-margin packages over pure volume growth. This has included disciplined pricing, targeted investments in automation, and a strategic retreat from low-margin volume — including renegotiating its relationship with Amazon.

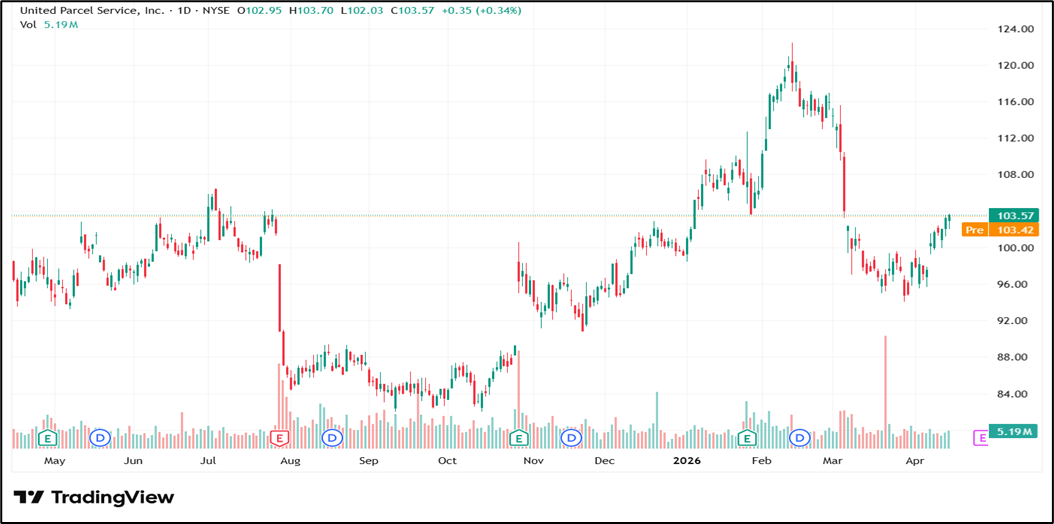

Stock Performance — April 2026

As of April 15, 2026, UPS shares closed at $103.57, up 0.34% on the day (+$0.35). After-hours trading saw additional modest gains of +$0.070 (+0.068%), bringing the after-hours price to $103.64. The stock opened the session at $102.95, reached an intraday high of $103.70, and touched a low of $102.03 during the trading day.

|

Price (Apr 15, 2026) $103.57 |

Daily Change +0.34% / +$0.35 |

After Hours $103.64 |

|

Open $102.95 |

Day High $103.70 |

Day Low $102.03 |

|

52-Week High $122.41 |

52-Week Low $82.00 |

Market Cap $8.80KCr |

|

P/E Ratio 15.80 |

Dividend Yield 6.33% |

Quarterly Div. $1.64 |

The 52-week range of $82.00 to $122.41 underscores significant volatility over the past year, driven by macroeconomic concerns, labor cost pressures, and ongoing normalization of e-commerce volumes following pandemic-era peaks. At current levels, the stock trades well below its 52-week high, which many analysts view as a potential value opportunity given the company's strong dividend and cash flow profile.

Financial Overview

UPS's financial profile reflects the dual pressures of volume normalization and cost management. The company generates substantial free cash flow, which underpins its dividend commitment. In fiscal year 2025, UPS reported revenues of approximately $89 billion, though this represented a modest year-over-year decline as the company shed low-margin volume in pursuit of its margin improvement strategy.

Operating margins have improved meaningfully since 2022 as the 'better not bigger' strategy took hold, with management targeting adjusted operating margins in the high-single to low-double-digit range. Capital expenditure discipline has been a hallmark of the Tome era, with UPS targeting approximately $4 billion in annual capex to modernize its network while preserving cash returns to shareholders.

The company's balance sheet carries meaningful debt — common for capital-intensive logistics businesses — but UPS maintains investment-grade credit ratings, reflecting its strong cash generation ability. With a P/E ratio of 15.80, the stock trades at a discount to many S&P 500 peers, making it attractive for value-oriented income investors.

Dividend History and Analysis

UPS has a proud history of dividend payments stretching back decades. The company is considered a 'Dividend Aristocrat' candidate due to its consistent track record of maintaining and growing its dividend. The current quarterly dividend of $1.64 per share implies an annualized payout of $6.56 per share.

At a stock price of approximately $103.57, this translates to a dividend yield of approximately 6.33% — one of the highest among S&P 500 components. For context, the S&P 500's average dividend yield typically hovers around 1.2–1.5%, making UPS's yield more than four times the index average.

Historically, UPS has grown its dividend at a mid-single-digit annualized rate. However, the pace of dividend growth has moderated in recent quarters as management prioritizes debt management and financial flexibility in a higher-rate environment. The dividend payout ratio, while elevated relative to earnings, is supported by the company's robust free cash flow generation, which typically exceeds reported net income.

Management Outlook and Guidance

CEO Carol Tome and the UPS management team have maintained a cautious but constructive tone heading into 2026. The company's key strategic priorities include accelerating automation of its network (which reduces per-package handling costs), growing its healthcare logistics business (a high-margin vertical), and expanding its SMB (small and medium business) customer base — which typically generates higher yields per package than large-shipper contracts.

For fiscal year 2026, management has guided toward revenue stabilization as volume declines abate and pricing initiatives take hold. Adjusted operating margin improvement remains a core KPI, with the company targeting a return to double-digit margins as the cost reduction program matures. The company has also signaled continued commitment to its dividend and share repurchase program, subject to macroeconomic conditions.

Key risks flagged by management include slowing global trade volumes (amplified by tariff uncertainties and geopolitical tensions), fuel cost volatility, labor cost pressures from union agreements, and the potential impact of a U.S. or global recession on package volumes.

Please wait processing your request...

Please wait processing your request...