With Disney and AppLovin both beating after Wednesday's close, and ADP printing 109,000, the fastest private-sector hiring pace since January 2025, and markets open Thursday on a broad risk-on footing. Initial jobless claims and U.S. productivity at 8:30 a.m. ET will test whether the labour market strength in ADP carries through to the government's weekly read, ahead of Friday's U.S. Employment Report.

Key Highlights

- Disney Q2 adjusted EPS USD 1.57 (consensus USD 1.50), Revenue USD 25.17B (consensus USD 24.85B); SVOD Operating Income up 88% to USD 582M

- AppLovin Q1 EPS USD 3.56 (consensus USD 3.44), beating for the fourth consecutive quarter; AXON platform and E-commerce expansion remain the primary growth drivers

- ADP April private payrolls +109,000 (consensus 84,000 to 99,000, prior 61,000); fastest pace since January 2025; services led at +94,000; mid-size firms the only soft spot

- S.-Iran diplomatic talks advancing; Iranian FM Araghchi met Wang Yi in Beijing Wednesday; Trump heads to China next week; WTI slides to USD 95.5.

- S&P 500 closed Wednesday up 1.46% at 7,365.11; Nasdaq up 2.08% at 28,599.17; VIX at 17.39; DXY flat at 98.004

Market Snapshot

U.S. Equity futures are holding Wednesday's gains in early Thursday trading. The S&P 500 cash index closed at 7,365.11, up 1.46%, and the Nasdaq surged 2.08% to 28,599.17, driven by the Disney and AppLovin beats alongside continued semiconductor strength. The Dow gained 1.24% to 49,910.59. The VIX is steady at 17.39, up just 0.06%, signalling that the risk-on move is orderly rather than reactive. WTI has slipped further to USD 95.57, down 0.65%, as U.S.-Iran diplomatic progress in Beijing continues to deflate the energy risk premium. Gold is up 0.33% at USD 4,700 and silver up 0.81% at USD 77.89, both moving in line with the softer dollar. The DXY is flat at 98.004.

Macro Context

Wednesday delivered a clean sweep: Disney and AppLovin beat on the Earnings side, ADP beat on the macro side, and Iran diplomacy progressed on the geopolitical side. The combination drove the S&P's largest single-session gain since the post-FOMC rally, with the Nasdaq's 2.08% advance reflecting the disproportionate weight of tech and media in the index.

The ADP print is the session's most consequential data point heading into Thursday. Private sector employment increased by 109,000 jobs in April, the fastest pace since January 2025, with services leading at 94,000 and goods-producing sectors adding 15,000. The soft spot was mid-size firms; small and large employers both added jobs. Pay growth for Job-stayers eased to 4.4%, while job-changers held at 6.6%, still solid, not accelerating. However, ADP's historically weak correlation with the BLS Payroll report means Friday's U.S. Employment Report (consensus 55,000, prior 178,000) remains genuinely open.

On the diplomatic front, the most significant overnight development is the state of U.S.-Iran negotiations. Iran is actively reviewing the latest U.S. peace proposal, with Tehran's Foreign Ministry confirming it would convey its position to Pakistani intermediaries after finalising its response. The proposal, the result of weeks of back-and-forth led by Islamabad, covers freedom of navigation through the Strait of Hormuz, Iran's nuclear and ballistic missile programme, reconstruction, and sanctions. Trump warned Wednesday on Truth Social that Iran would face strikes "at a much higher level and intensity" unless it agrees to terms, while Rubio separately declared Operation Epic Fury "concluded" and said Washington now seeks a "memorandum of understanding for future negotiations", precisely what Iran has been demanding for weeks.

The nuclear question remains the sticking point: the U.S. position has shifted from full dismantlement of Natanz, Isfahan, and Fordow to a softer framing, but Iran has not yet accepted. On the China side, Wang Yi pressed Araghchi in Beijing for an immediate end to hostilities and prompt Hormuz reopening, and said Beijing is willing to play a larger role in peace talks ahead of the Trump-Xi summit on May 14 to 15. The WTI slide from above USD 107 on Monday to USD 95.57 Thursday morning, a USD 12-per-barrel Deflation in four sessions, reflects markets pricing a rising probability of a negotiated exit before the Trump-Xi meeting. Three Fed speakers today, Kashkari at 1:00 p.m., Hammack at 2:05 p.m., and Williams at 3:30 p.m., give the committee its first opportunity to respond publicly to a materially different macro picture than last week's FOMC: energy deflating, labour market re-accelerating, equities at six-week highs.

Economic Data

8:30 a.m. ET: Initial Jobless Claims, week ending May 2 Consensus: 206,000 · Prior: 189,000 · The weekly labour market read ahead of Friday's Employment Report. A print above 220,000 would complicate the ADP beat narrative and raise questions about whether private payrolls translate to government data. Below 200,000 reinforces the labour market resilience story.

8:30 a.m. ET: U.S. Productivity, Q1 Preliminary Consensus: 1.1% · Prior: 1.8% · A deceleration is expected. The operative question is whether unit labour costs, the flip side of productivity, are rising fast enough to sustain the Fed's Inflation concern. Watch for the unit labour cost print alongside the headline.

10:00 a.m. ET: Construction Spending, February (delayed) and March Feb consensus: 0.1% · Feb prior: -0.3% · March consensus: 0.3% · Housing and construction data is a lagging indicator at this rate level. The sequential gap between the two prints tells you whether the energy-price spike in Q1 has begun to bite Capital spending.

1:00 p.m. ET: Minneapolis Fed President Kashkari speech Kashkari dissented at last week's FOMC, opposing the easing bias. With energy deflating and ADP beating, his framing of the updated macro picture is the operative signal for whether the committee's hawkish flank is softening.

2:05 p.m. ET: Cleveland Fed President Hammack speech Hammack also dissented at the FOMC. Convergence or divergence with Kashkari's tone sets the committee fracture narrative for the week.

3:30 p.m. ET: New York Fed President Williams speech Williams is among the most influential voices on the committee. Any signal that the post-ADP, post-Iran data shift is changing his rate path view would be the day's most significant market-moving statement.

Earnings: Before the Bell

McDonald's (NYSE:MCD) EPS consensus USD 2.77 against a year-ago USD 2.60, on revenue of USD 6.49B. McDonald's is the session's consumer barometer. Same-store sales growth in the U.S. and international operated markets are the operative metrics; in an environment where core PCE is running at 3.2%, value positioning and digital ordering penetration are the structural tailwinds. Any commentary on consumer trade-down behaviour, customers choosing McDonald's over casual dining, is the catalyst for the broader consumer discretionary read.

Vistra Corp (NYSE:VST) EPS consensus USD 1.32 against a year-ago USD 0.45, on revenue of USD 5.57B. The session's most striking year-on-year comparison: nearly a 3x EPS expansion driven by power generation Demand from AI data centres and the energy price environment. Capacity additions, hedging posture under the current Commodity backdrop, and any guidance on nuclear asset utilisation are the operative signals. With WTI pulling back, whether Vistra's power pricing holds is the key question.

Earnings: After the Bell

Airbnb (NASDAQ:ABNB) EPS consensus USD 0.31 against a year-ago USD 0.24, on revenue of USD 2.62B. Nights and experiences booked and average daily rate trajectory are the two metrics that drive the stock. In a high-inflation, high-energy-cost environment, whether consumers are still committing to travel spend, and whether Airbnb is seeing international booking recovery as Hormuz tensions ease, determines the forward guidance tone. Any commentary on summer 2026 booking pace would be a direct read on consumer discretionary resilience.

Gilead Sciences (NASDAQ:GILD) EPS consensus USD 1.90 against a year-ago USD 1.81, on revenue of USD 6.91B. HIV Franchise durability (Biktarvy) and the oncology pipeline (notably the CLL and breast cancer programmes) are the operative metrics. A modest beat is expected; what moves the stock is any update on the cell therapy pipeline or any revision to full-year guidance that signals confidence in the back half.

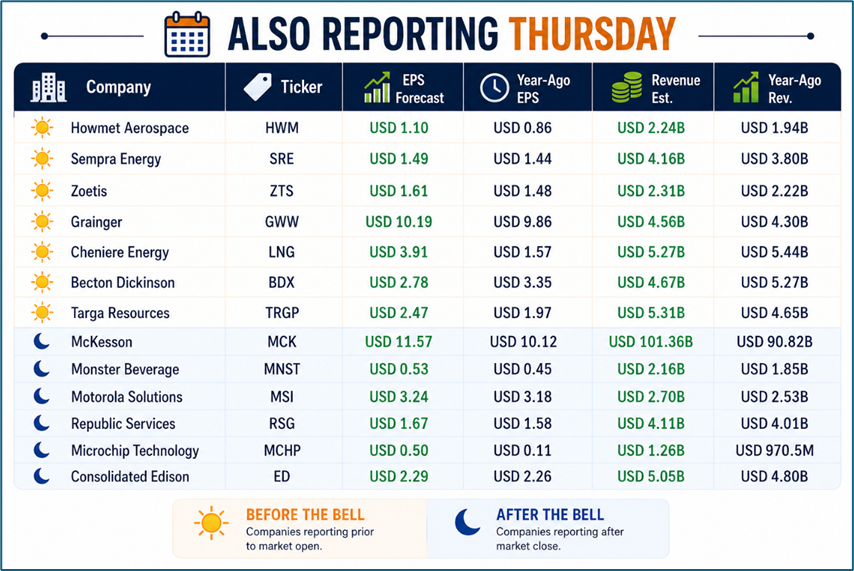

Also Reporting Thursday

Source: Kalkine

One Number to Watch

206,000 is the initial jobless claims consensus for the week ending May 2. A print at or below that level, arriving the morning after ADP's 109,000 beat, would deliver back-to-back labour market confirmations and set up Friday's U.S. Employment Report (consensus 55,000, prior 178,000) as a potential upside surprise. A print above 220,000 breaks the narrative, raises questions about whether ADP's private payroll strength is translating to the broader economy, and gives Kashkari and Hammack ammunition to hold the hawkish line in their afternoon speeches. The number lands at 8:30 a.m. ET, 90 minutes before markets open.

Please wait processing your request...

Please wait processing your request...