April CPI lands at 6:00 p.m. ET Tuesday, the session's defining print, arriving against a backdrop of a ceasefire described by Trump as on "massive life support," WTI holding near USD 99, and a consensus that points to the largest annual Inflation increase since January 2024. The number will either validate or complicate the Fed's higher-for-longer stance heading into the Trump-Xi summit beginning Wednesday.

Key Highlights

- Trump called Iran's proposal "a piece of garbage"; ceasefire on "massive life support"; aides say resumption of combat operations under serious consideration

- April CPI due 6:00 p.m. ET: headline +3.7% YoY forecast, largest annual increase since January 2024; core +2.7% YoY; BofA and JPMorgan see no Fed cuts in 2026

- Trump-Xi summit begins Wednesday with Musk, Cook, Fink, Solomon, Schwarzman, and Fraser in the delegation; Iran, trade, and AI on the agenda

- S&P 500 and Nasdaq closed Monday at fresh record highs; S&P +0.19% at 7,412.85; VIX rose 6.92% to 18.38

Market Snapshot

U.S. Equity futures slipped in early Tuesday trading as investors positioned ahead of the CPI release and monitored Iran developments. The S&P 500 closed Monday at 7,412.84, up 0.19%, and the Nasdaq gained 0.10% to 26,274.125, with the Dow adding 0.19% to 49,704.47. The VIX rose 6.92% to 18.38, signalling that uncertainty is building ahead of CPI rather than dissipating. The 10-year Yield climbed to around 4.42% Tuesday, a one-week high, as the Iran ceasefire deterioration kept inflation risks in focus and Trump's national security team was reported to be evaluating a potential resumption of military operations. The DXY moved back above 98, up 0.28% to 98.180, firming on safe-haven Demand from the Hormuz uncertainty. WTI is at USD 99.20, up 1.15%, extending gains as Iran deal prospects dim. Gold is down 0.25% to USD 4,717.10 and silver is down 0.11% to USD 85.855, with precious metals retreating slightly as the dollar firms.

Macro Context

Monday's session delivered a clean equity rally despite the Iran backdrop, with the S&P 500 and Nasdaq both closing at record highs as AI-related chipmakers continued their advance and six of eleven S&P sectors finished in positive territory. The divergence between equity strength and rising geopolitical risk is the week's central tension: markets are pricing AI capex momentum and a potential trade deal from the Trump-Xi summit while simultaneously holding WTI near USD 99 and watching the 10-year yield push toward 4.42%.

The Iran situation continued to deteriorate. Speaking in the Oval Office on Monday, Trump called Iran's proposal a "piece of garbage" and said he did not even finish reading it, declaring the ceasefire on "massive life support." Trump aides told he is now more seriously considering a resumption of major combat operations than at any point in recent weeks, driven by frustration over the continued closure of the Strait of Hormuz and what he sees as division in Iranian Leadership preventing substantive nuclear concessions. The State Department separately announced sanctions targeting 12 companies and individuals allegedly helping Iran sell oil to China, a move that will add to tensions at the Trump-Xi table.

Trump-Xi discussions begin Wednesday, with the Iran war expected to crowd out progress on trade and rare earth Supply chains. Treasury Secretary Bessent visits Tokyo Tuesday to meet Japan PM Takaichi ahead of the summit.

Trump is also bringing one of the largest corporate delegations in recent memory to Beijing, including Elon Musk, Tesla (NASDAQ:TSLA); Tim Cook, Apple (NASDAQ:AAPL); Larry Fink, BlackRock (NYSE:BLK); David Solomon, Goldman Sachs (NYSE:GS); Stephen Schwarzman, Blackstone (NYSE: BX) and Jane Fraser, Citigroup (NYSE:C), with the White House hoping to secure Business deals and purchase agreements alongside the geopolitical agenda.

Today's CPI release is the session's centrepiece. Headline inflation is forecast at +3.7% year-on-year, which would be the largest annual increase since January 2024 and a sharp acceleration from March's 3.3%. The primary driver is energy: gas prices are expected to show a 6% monthly rise. A technical adjustment to rent and owners' equivalent rent data, which was suppressed in October by the Government Shutdown, will also lift the core reading. Core CPI is forecast at +0.3% MoM and +2.7% YoY, up from +0.2% and +2.6% in March. Bank of America no longer expects any Fed rate cuts in 2026. JPMorgan has laid out three scenarios:

- Pessimistic: peak inflation breaks 5% if oil surges past $120, with the conflict entering militarised control of Hormuz and Middle East infrastructure damaged

- Neutral: inflation peaks near 4% before retreating, following a path similar to the 2022 Russia-Ukraine energy shock

- Optimistic: a diplomatic resolution brings inflation back toward 3% by year-end, though still above the Fed's 2% target until early 2027 in all three scenarios

A print above 3.8% YoY reinforces the higher-for-longer consensus heading into the Trump-Xi summit. A print at or below 3.5% would be the session's positive surprise and the only realistic catalyst for a rate-cut repricing.

Economic Data

6:00 p.m. ET: CPI, April Headline MoM consensus: +0.6% · Prior: +0.9% · Headline YoY consensus: +3.7% · Prior: +3.3% · The session's defining print. See One Number to Watch.

6:00 p.m. ET: Core CPI, April MoM consensus: +0.3% · Prior: +0.2% · YoY consensus: +2.7% · Prior: +2.6% · Core strips out food and energy; the rent and OER technical adjustment will mechanically lift this reading. Watch for the ex-shelter core print, which is the cleanest read on whether Iran war energy costs are bleeding into broader services inflation.

12:45 p.m. ET: Fed Williams speech Williams is among the most influential voices on the committee. Any pre-CPI framing of the Fed's reaction function to a hot print is the session's early market-moving signal.

10:30 p.m. ET: Fed Goolsbee speech Post-CPI. Goolsbee has historically leaned dovish; his interpretation of today's print sets the tone for how the committee's moderate wing is processing the inflation data.

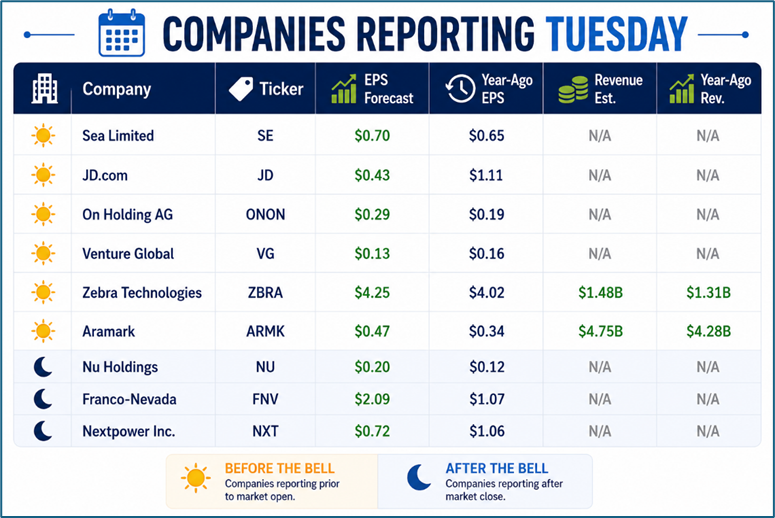

Tuesday's earnings slate is light relative to last week. No single BMO reporter carries sufficient market cap or narrative weight to Warrant an individual write-up against today's CPI and Iran backdrop.

Companies Reporting Tuesday

Source: Kalkine

One Number to Watch

3.7% is the April CPI YoY consensus, and it is the most consequential inflation print of 2026 so far. A result at or above 3.8% confirms the Iran war energy shock is passing through to broader consumer prices at a pace that removes any remaining argument for Fed rate cuts this year, reinforces the 10-year yield's move toward 4.42%, and hands Trump a complicated domestic backdrop as he sits down with Xi on Wednesday.

A print at or below 3.5% would be the session's positive surprise: evidence that energy pass-through is less severe than feared, and the only realistic catalyst for a rate-cut repricing and equity upside from here. The core reading matters equally: if core CPI comes in above 0.35% MoM, it signals the inflation is no longer confined to energy and that the rent adjustment is masking a broader re-acceleration. The number lands at 6:00 p.m. ET, after the equity market close, setting the tone for Wednesday's open.

Please wait processing your request...

Please wait processing your request...