Markets open Wednesday with two sequenced shocks from Tuesday: April CPI printed 3.8% year-on-year, above the 3.7% consensus and the highest since May 2023, confirming that the Iran war energy shock is passing through to broader consumer prices. Within hours, stock futures turned higher as attention shifted to the Trump-Xi summit beginning in Beijing today, with markets pricing the possibility of trade and AI deals that could offset the Inflation headwind. PPI at 8:30 a.m. ET is the day's primary domestic data point; Cisco reports after the bell.

Key Highlights

- April CPI +3.8% YoY (consensus +3.7%); core +0.4% MoM and +2.8% YoY, both above consensus; real wages fell 0.5% MoM for the first time in three years

- Markets pricing 35% probability of a December rate hike; Fed cuts fully priced out; 10-year Yield at 4.46%, near 11-month high

- Trump-Xi summit begins today in Beijing; Trump says trade takes precedence over Iran; China holds Leverage as Iran's largest trade partner

- WTI at $100.92, Brent at $106.43; S&Amp;P 500 closed -0.16% at 7,400.96; Nasdaq -0.71%; futures broadly higher ahead of summit

Market Snapshot

U.S. Equity futures are broadly higher in early Wednesday trading as markets look past Tuesday's CPI beat toward potential summit outcomes. The S&P 500 closed Tuesday at 7,400.96, down 0.16%, and the Nasdaq fell 0.71% to 26,088.203 as the hot CPI print weighed on rate-sensitive Growth Stocks. The Dow bucked the trend, adding 0.11% to 49,760.56, with energy and value stocks providing support. The Russell 2000 fell 0.97% to 2,842.831. The VIX eased to 17.99, down 2.12%, as the CPI reaction was orderly rather than panicked. The 10-year yield firmed around 4.46% Wednesday, approaching its highest level since June last year, as the hot CPI print reduced expectations for Fed rate cuts and markets began pricing a 35% probability of a December rate hike. The DXY held above 98, supported by the same inflation dynamics. WTI is at $100.92, down 1.23%, and Brent at $106.43, down 1.24%, with oil pulling back slightly from overnight highs as the ceasefire holds tenuously. Gold is up 0.42% to $4,706.60 and silver up 1.85% to $87.175, with precious metals recovering on safe-haven Demand as the summit introduces a new binary.

Macro Context

Tuesday's CPI print confirmed the pessimistic scenario that markets had been partially pricing but hoping to avoid. Headline CPI rose 0.6% MoM, pushing the annual rate to 3.8%, the highest since May 2023. Core CPI rose 0.4% MoM and 2.8% YoY, both above Wall Street expectations, with the monthly core reading the highest since January 2025. Energy rose 3.8% in April, accounting for over 40% of the monthly increase. The core acceleration reflected the spread of higher energy costs into broader consumer categories: shelter rose 0.6% (vs. 0.3% in March), transportation services +0.3%, and apparel +0.6%. Airline fares rose 20.7% over the past 12 months and beef prices rose 14.8% year-on-year. Indexes that declined included new vehicles, communication, and medical care. For the first time in three years, real average hourly wages fell, declining 0.5% for the month and 0.3% annually, meaning the Iran war energy shock is now directly eroding purchasing power. The October 2025 Government Shutdown created a statistical suppression of rent and OER data that unwound in April as expected, lifting the core reading further.

Separately, the New York Fed reported increased consumer Loan delinquency rates, particularly on student loans.

The rate market reaction was the session's most consequential development. Markets have largely priced out any Fed rate cuts in 2026; expectations for a quarter-point rate hike in December climbed to 35% following the CPI release, a significant shift from the "hold" consensus that prevailed as recently as last week.

The 10-year yield firmed around 4.46%, approaching its highest level since June last year. CME FedWatch futures traders now see no cuts and a growing probability of hikes.

The equity market's post-CPI reaction was notable for its restraint. After an initial leg lower, futures stabilised and turned higher as attention shifted to the Trump-Xi summit, which begins today in Beijing. Trump indicated before departing that trade talks will take precedence over the Iran situation at the summit, a signal that markets read constructively: purchase agreements and trade framework announcements are the primary positive catalysts being priced. China holds a degree of leverage heading in, as Beijing is Iran's largest trade partner and the top buyer of its oil, giving Xi a card to play on the conflict. The agenda covers trade, AI regulation and chip export controls, Taiwan, and rare earth Supply chains, though Trump's own framing places trade first.

Today's PPI at 8:30 a.m. ET is the session's primary domestic data point, arriving the morning after a hot CPI print. If producer prices are still accelerating, it signals more consumer inflation is in the pipeline. Cisco reports after the bell as the session's most significant Earnings name.

Economic Data

8:30 a.m. ET: Producer Price index, April MoM consensus: +0.5% · Prior: +0.5% · Expected to hold flat month-on-month. Coming the morning after a 3.8% CPI print, a PPI beat would signal that Upstream cost pressures remain entrenched and that further consumer inflation pass-through is likely in May and June.

8:30 a.m. ET: Core PPI, April MoM consensus: +0.3% · Prior: +0.2% · YoY prior: +3.6% · Core PPI strips out food and energy; an acceleration here would tell you the inflation is not purely an energy story and has embedded itself in services and Manufacturing inputs.

11:30 a.m. ET: Boston Fed President Collins speech Collins has been in the moderate camp on the committee. Her framing of the CPI print and any signal on how the Fed is weighing the growth-inflation trade-off is the operative market signal ahead of the equity open.

7:00 p.m. ET: Dallas Fed President Logan speech Logan dissented at last week's FOMC against the easing bias. Post-CPI, her tone is the most important hawkish read on how the committee is processing a 3.8% print alongside a 10-year yield at 4.42%.

Earnings: Before the Bell

Wednesday's BMO slate is light.

Alibaba (NYSE: BABA) is the one name worth watching, reporting Q1 results against a year-ago EPS of $1.57 with consensus at $1.02. The year-on-year EPS decline reflects the competitive pressure from Pinduoduo and ByteDance in domestic Chinese E-commerce. Cloud Revenue growth from Alibaba Cloud and any commentary on AI infrastructure spending in China is the operative signal heading into the Trump-Xi summit; Alibaba's capex posture under potential new export controls is the forward-looking variable.

Earnings: After the Bell

Cisco Systems (NASDAQ:CSCO) EPS consensus $0.86 against a year-ago $0.78, on revenue of approximately $14B. The session's most consequential earnings report. Cisco is the read on enterprise networking demand and, increasingly, on AI data centre infrastructure spending. Order Backlog, product revenue growth, and any commentary on hyperscaler networking buildouts are the operative signals. Cisco has been a direct beneficiary of the same AI capex cycle that drove Arista's beat last week; whether that demand is accelerating or plateauing is the key question. Any guidance commentary on the impact of export controls or supply chain disruption from the Iran-related energy and logistics shock would be an additional market mover.

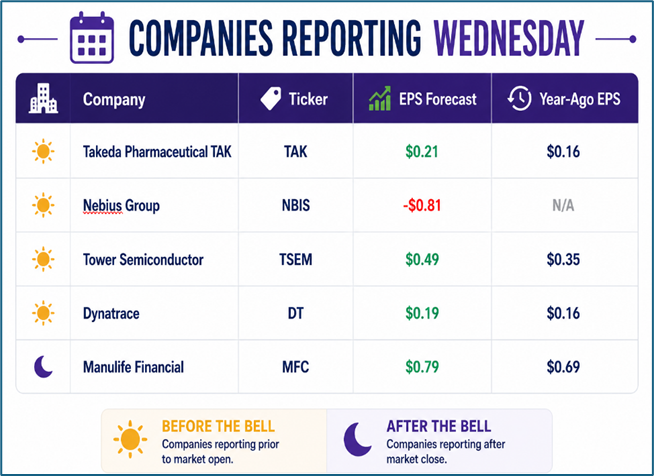

Also Reporting Wednesday

Source: kalkine

One Number to Watch

$100 is the WTI level that WTI crossed back above overnight, and it is the session's most watched psychological threshold. Tuesday's CPI print confirmed the energy shock is passing through to consumer prices at 3.8% annually.

If WTI holds above $100 through today's session and the Trump-Xi summit produces no concrete signal on Iran, the market's JPMorgan neutral-case scenario of inflation peaking near 4% before retreating moves toward the base case, not the optimistic one.

A summit outcome that includes a concrete Chinese commitment to pressure Iran on the Hormuz closure, or any indication of direct U.S.-Iran talks resuming, would be the catalyst to push WTI back below $100 and give the Fed room to breathe. The direction of oil and the summit headlines are the two variables that will set the tone for the rest of the week.

Please wait processing your request...

Please wait processing your request...