With AMD and Arista both beating expectations after Tuesday's close, markets open Wednesday in a risk-on posture, but the ADP employment print at 8:15 a.m. ET will test whether the labour market is holding ahead of Friday's nonfarm payrolls. Walt Disney and AppLovin report after the bell, carrying the session's highest earnings stakes.

Key Highlights

- AMD beat EPS (USD 1.37 vs. USD 1.27) and revenue (USD 10.3B vs. USD 9.84B); data centre up 57% year-on-year; Q2 guidance above consensus

- Arista beat revenue at USD 2.709B (consensus USD 2.62B), non-GAAP EPS USD 0.87, up 35.1% year-on-year

- ISM Services 53.6 in April (consensus 53.7); new orders fell 7.1 points, sharpest drop in three years; prices paid held at 70.7

- Trump paused Project Freedom; Rubio confirmed Operation Epic Fury's offensive phase has ended; Iran FM heads to Beijing Wednesday

- S&P 500 closed up 0.81% at 7,260 ; Nasdaq up 1.31%; DXY down 0.47% to 98.

Market Snapshot

U.S. equity futures are higher in early Wednesday trading, extending Tuesday's rally on the back of AMD and Arista beats. S&P 500 futures (ES1!) closed Tuesday's session at 7,254.50, up 0.34%, with the cash index finishing at 7,259.21 (+0.81%). Nasdaq closed up 1.31% at 28,015.06 and the Dow gained 0.73% to 49,298.25. The VIX eased to 17.38, down 4.98%, as risk sentiment improved. The DXY softened to 98.021, down 0.47%, its lowest level in several sessions. The 10-year yield pulled back to approximately 4.43%, down from Monday's 4.456% high, as oil retreated and inflation fears eased slightly. WTI slipped further to USD 100.28, down 2.33%, and Brent is trading near USD 110. Gold surged to USD 4,647.29, up 2.01%, and silver climbed 3.93% to USD 75.685, lifted by the dollar's 0.47% slide to 98.

Macro Context

Tuesday's session delivered a broadly constructive data set with one embedded warning. ISM Services held firmly in expansion at 53.6, confirming the services sector is absorbing elevated energy costs without demand destruction; the "one number to watch" threshold of 52 was never tested. However, the new orders subindex fell 7.1 points to 53.5, its sharpest single-month drop in three years, and the prices paid index held at 70.7, still at its highest level since 2022. The combination signals that demand deceleration is beginning, even as cost pressures remain entrenched. JOLTS came in above consensus at 6.9 million, matching February's revised figure; the labour market is not yet cracking.

After the close, AMD delivered the session's decisive print. Data centre segment revenue was USD 5.8 billion, up 57% year-on-year, driven by strong demand for EPYC processors and the continued ramp of Instinct GPU shipments. Q2 guidance of USD 10.9 to USD 11.5 billion was above the USD 10.5 billion consensus estimate. Arista followed with revenue of USD 2.709 billion, up 35.1% from Q1 2025, and a net promoter score of 89. Both prints validate the AI infrastructure capex thesis heading into Disney and AppLovin tonight.

On the geopolitical front, the most significant overnight development is the de-escalation in the Strait of Hormuz. Late Tuesday, Trump announced the pause of Project Freedom, the two-day-old U.S. operation to escort commercial vessels through the strait, citing progress in diplomatic talks. Secretary of State Rubio separately confirmed that Operation Epic Fury, the major offensive campaign against Iran, has ended. The U.S. naval blockade of Iranian ports remains in place. Iranian Foreign Minister Araghchi arrives in Beijing Wednesday for talks with Wang Yi, the first direct diplomatic meeting since the war began, with Trump scheduled to visit China next week. The crude pullback already visible in WTI at USD 100.28 (-2.33%) reflects markets pricing in some probability of a negotiated exit; any positive signal from the Beijing talks would extend that move. Wednesday's ADP print at 8:15 a.m. ET is the session's pivotal domestic number, framing the labour market ahead of Friday's nonfarm payrolls, where consensus sits at 55,000, a sharp deceleration from March's 178,000.

Economic Data

8:15 a.m. ET: ADP Employment, April Consensus: 84,000 · Prior: 62,000 · The private payroll read that frames Friday's nonfarm payrolls. A beat above 100,000 would complicate the soft-landing narrative; a miss below 60,000 accelerates growth concerns and changes the backdrop for Disney's conference call tonight.

9:30 a.m. ET: St. Louis Fed President Musalem speech Musalem has been among the more hawkish voices on the committee. Any framing of the ISM Services prices component or the Hormuz energy pass-through into core inflation is the operative signal for rate path expectations.

1:00 p.m. ET: Chicago Fed President Goolsbee speech Goolsbee has historically leaned dovish. Divergence from Musalem's tone would reinforce the committee fracture narrative established at last week's FOMC. Watch for any update on how the Fed is weighing the energy shock against slowing demand.

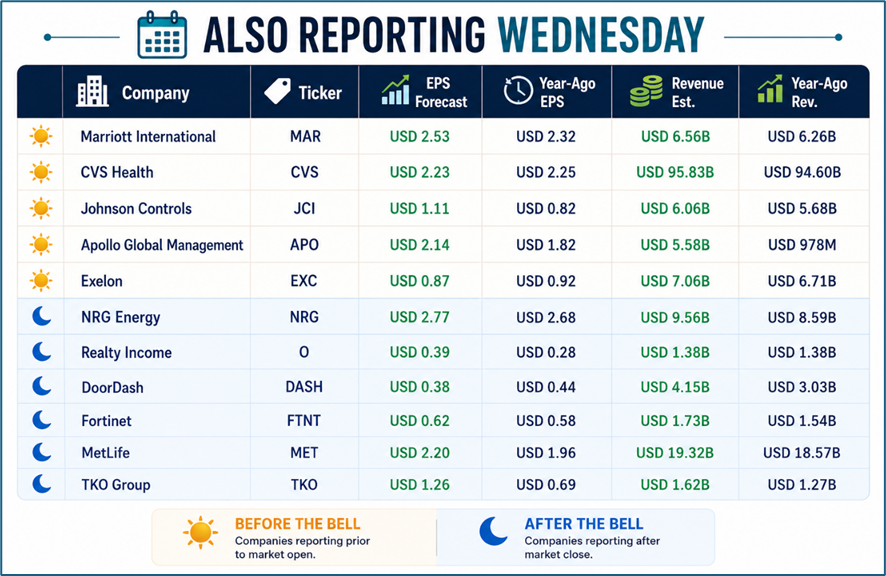

Earnings: Before the Bell

Walt Disney (NYSE:DIS) EPS consensus USD 1.50 against a year-ago USD 1.45, on revenue of USD 24.94B. Disney is the session's most watched BMO reporter. The operative metrics are streaming profitability at Disney+ (whether it has sustained the margin expansion from Q1), domestic parks attendance against the energy-price squeeze on consumer discretionary spending, and any guidance commentary on the summer season. The year-on-year comparison is modest; what moves the stock is whether management raises full-year guidance or signals caution on consumer demand in H2.

Uber (NYSE:UBER) EPS consensus USD 0.69 against a year-ago USD 0.83, on revenue of USD 13.33B. The year-on-year EPS decline against strong revenue growth flags margin compression, likely from driver incentive costs and insurance. Gross bookings growth and take-rate trajectory are the operative signals. Autonomous vehicle partnership commentary, particularly any update on the Waymo relationship, has become the structural story that lifts this beyond the headline.

Earnings: After the Bell

AppLovin (NASDAQ:APP) EPS consensus USD 3.41 against a year-ago USD 2.26, on revenue of USD 1.77B. The session's highest-stakes AMC report. AppLovin has been one of the market's standout performers, and the consensus implies 51% EPS growth year-on-year. The operative question is whether the AXON 2.0 ad-tech platform is continuing to take share in mobile advertising, and whether management can sustain guidance that has consistently exceeded expectations. Any commentary on AI-driven monetisation and advertiser retention in a high-inflation environment is the catalyst.

Warner Bros. Discovery (NASDAQ:WBD) EPS consensus -USD 0.07 against a year-ago -USD 0.18, on revenue of USD 8.9B. An expected loss, but the direction of travel is the story. Max streaming subscriber growth and the pace of debt reduction are the two metrics the market is watching. Any signal that the balance sheet trajectory is improving, or that content investment is generating subscriber leverage, would be a positive catalyst on an otherwise modest beat.

Source: Kalkine

One Number to Watch

84,000 is the ADP employment consensus for April. A print at or above that level signals the private labour market is absorbing elevated energy costs without meaningful job loss, keeping the stagflation risk asymmetric rather than bilateral. A miss below 60,000, arriving on the same morning that new orders in ISM Services just posted their sharpest three-year decline, shifts the interpretive frame toward demand destruction and gives AppLovin's and Disney's conference calls a materially weaker consumer backdrop than the AMD-fuelled risk-on open currently suggests. Friday's nonfarm payrolls at 55,000 consensus are already priced for deceleration; ADP below 60,000 would suggest even that bar may be too high

Please wait processing your request...

Please wait processing your request...