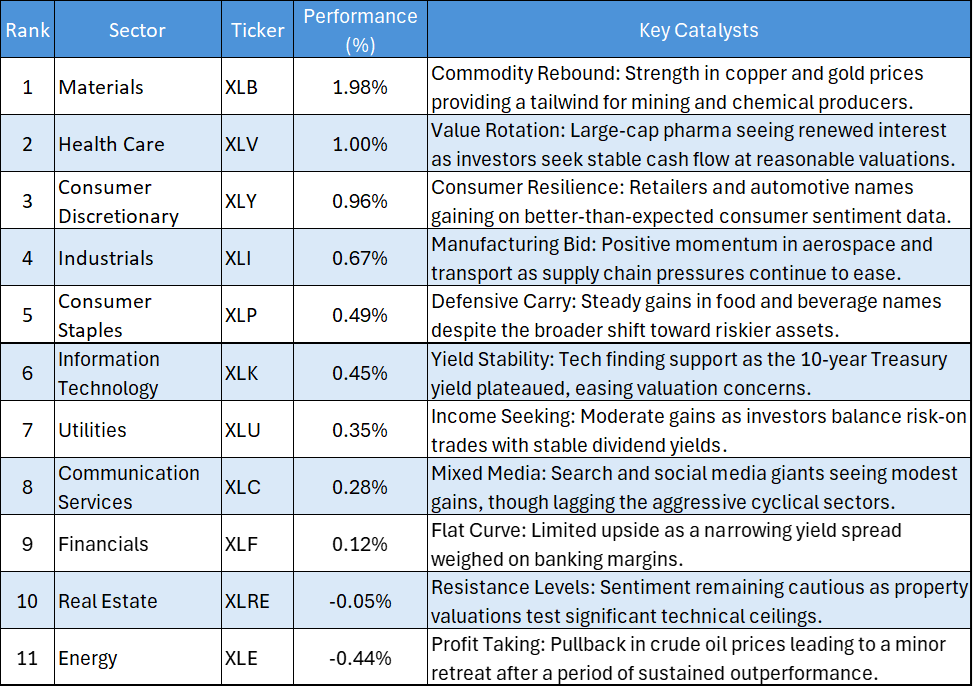

Key Highlights

- Materials Breakout: XLB dominated the session with a 1.98% surge, driven by a rebound in industrial commodity prices.

- Broad-Based Gains: Ten out of eleven sectors finished in positive territory, signaling a shift toward risk-on sentiment.

- Health Care & Discretionary Strength: Both XLV (+1.00%) and XLY (+0.96%) outperformed the broader market, reflecting a balanced mix of defensive and growth bidding.

- Energy Lagging: XLE was the day's primary detractor, falling 0.44% as geopolitical risk premiums began to cool.

The US equity market on March 25, 2026, experienced a robust "relief rally," with cyclical sectors leading the charge. After a period of defensive posturing, investors rotated back into "real economy" plays, buoyed by stabilizing treasury yields and a momentary pause in the dollar's recent climb.

Sector Performance & Key Catalysts

The following table summarizes the daily performance and the fundamental drivers behind today's price action:

Daily S&P 500 Sector Performances – 25/03/2026

Key Market Themes

The "Real Economy" Resurgence

The standout performance of Materials (XLB) and Industrials (XLI) suggests that the market is beginning to price in a "soft landing" or a re-acceleration of industrial activity. The 1.98% jump in Materials indicates a shift in capital toward raw materials and basic resources, often a precursor to broader economic expansion.

Balanced Risk Appetite

Unlike previous sessions where gains were concentrated in a single theme (like AI or Geopolitics), today’s move was remarkably balanced. The simultaneous rise of Health Care (XLV) and Consumer Discretionary (XLY) suggests that institutional investors are adding exposure across the board rather than chasing a single narrow trend.

Energy’s Brief Reprieve

After weeks of acting as the market's primary hedge, Energy (XLE) took a breather. This -0.44% decline appears to be a technical correction rather than a change in long-term sentiment, as investors lock in profits following the price spikes seen earlier in the month.

Bottom Line

The session on March 25 marks a constructive day for the S&P 500, with market breadth improving significantly. The leadership shift from Energy to Materials indicates a broadening of the rally, though the slight weakness in Real Estate serves as a reminder that the market remains sensitive to the long-term interest rate outlook.

Please wait processing your request...

Please wait processing your request...