Key Highlights

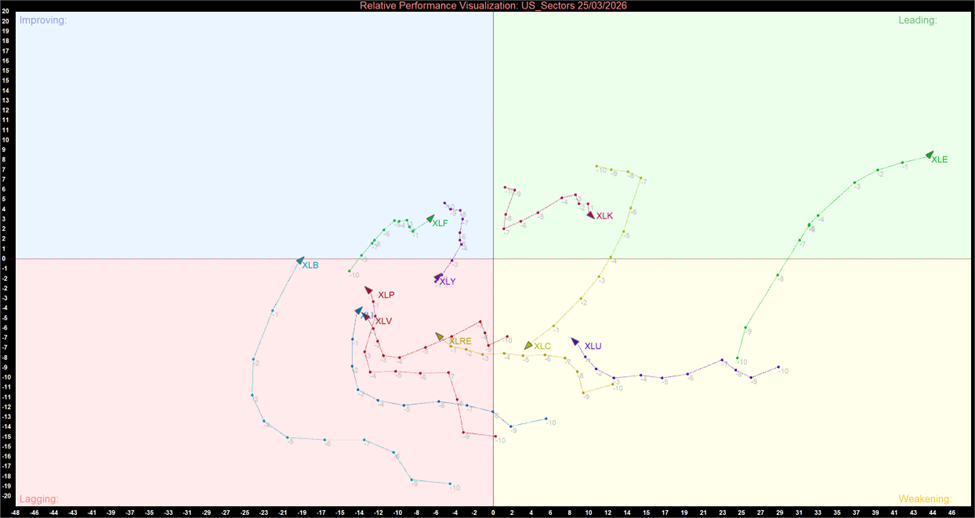

- Growth and Power Leadership: Both Information Technology (XLK) and Energy (XLE) are firmly positioned in the Leading quadrant, demonstrating strong relative strength and positive momentum.

- Defensive Breakdown: Utilities (XLU) has dropped into the Weakening quadrant, joining Communication Services (XLC). Meanwhile, Consumer Staples (XLP) is stuck in the Lagging quadrant, confirming a distinct rotation away from traditional safe-haven assets.

- Narrowing Cyclical Recovery: Materials (XLB) and Industrials (XLI) are the only two sectors advancing through the Improving quadrant, signaling a highly concentrated shift into "hard asset" cyclicals.

The US sector rotation on March 25, 2026, reveals a highly aggressive and confident market posture. The momentum chart illustrates a clear preference for growth and raw cyclicals, with capital aggressively rotating out of defensive sectors as economic confidence builds.

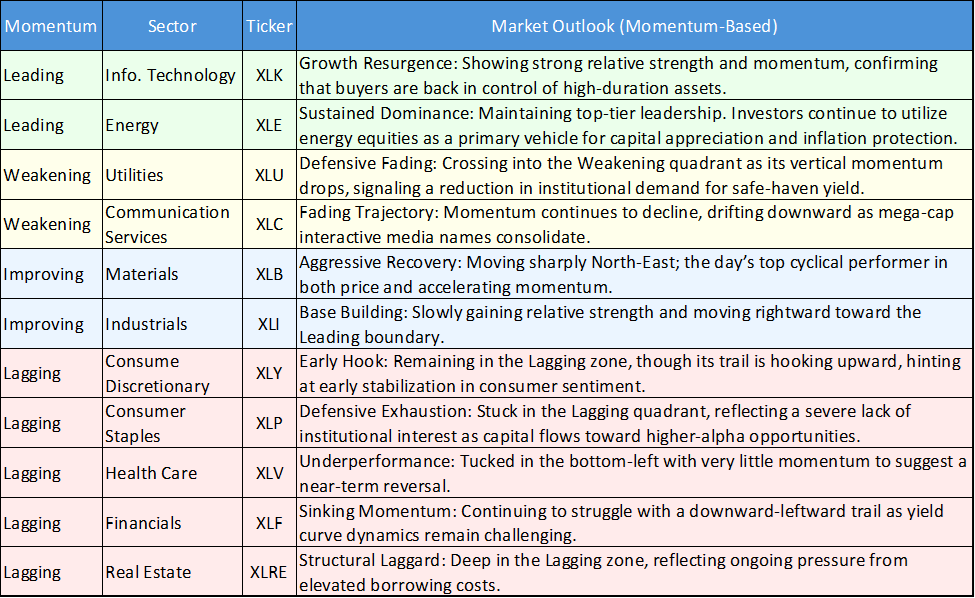

Daily US Sector Momentum Summary

The following table summarizes the updated momentum trajectory, categorizing all 11 sectors into their confirmed momentum quadrants:

Daily US Sector Relative Momentum Chart – 25/03/2026

US Sector Relative Momentum Chart (at the closing price of 25th March 2026). Powered by: amibroker.com

Daily US Sector Momentum Summary Table

Key Market Themes

The "Barbell" Leadership Strategy

The presence of both Information Technology (XLK) and Energy (XLE) in the Leading quadrant indicates a classic "barbell" market environment. Investors are confidently buying high-duration growth assets (Tech) driven by structural tech demand, while simultaneously hedging against sticky inflation by holding supply-constrained assets (Energy). This dual leadership limits the broader market's downside, as capital cycles between these two heavyweights rather than fleeing the market entirely.

The Exodus from Defensives

The degradation of defensive sectors is the most telling technical signal on the chart. With Utilities (XLU) dropping into the Weakening quadrant and Consumer Staples (XLP) languishing in Lagging, the "flight to safety" trade has effectively unwound. This underperformance suggests that institutional managers are not fearful of an imminent economic recession, opting instead to chase yield and growth in more aggressive areas of the market.

A Concentrated Industrial Bid

The Improving quadrant is exclusively populated by Materials (XLB) and Industrials (XLI). The absence of consumer-facing sectors (like XLY) in this zone indicates that the cyclical recovery trade is currently highly concentrated in raw materials and manufacturing. This specific rotation implies that investors are pricing in a re-acceleration of global industrial production rather than a broad-based consumer spending boom.

Bottom Line

The momentum landscape as of March 25 is unambiguously bullish for risk assets. With Tech and Energy firmly in the driver's seat, industrial cyclicals accelerating, and defensives like Utilities and Staples being left behind, the market is signaling high confidence in corporate earnings growth and a resilient underlying economy.

Please wait processing your request...

Please wait processing your request...