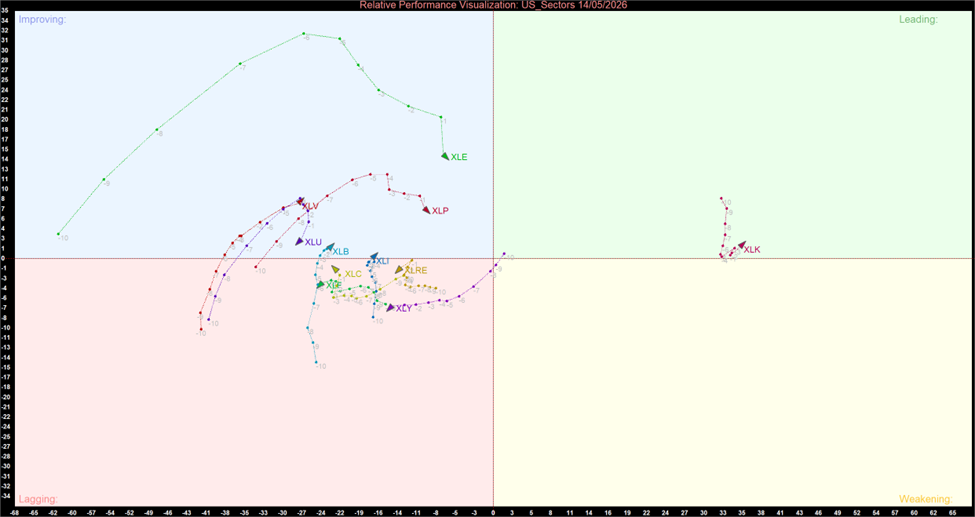

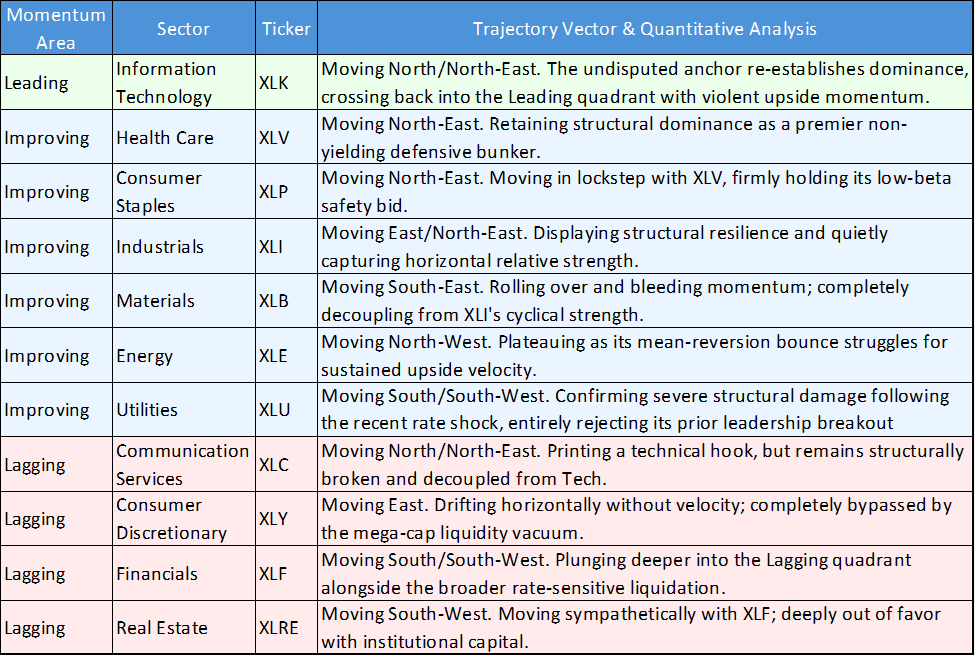

Key Momentum Highlights

- The Anchor Returns: Information Technology (XLK) printed a violent North/North-East hook, forcefully crossing back into the Leading quadrant. The market's primary structural anchor has officially re-established its mathematical dominance.

- The Permanent Growth Fracture: The historical Growth Triad is structurally shattered. While XLK reclaims Leadership, Consumer Discretionary (XLY) and Communication Services (XLC) remain deeply trapped in the Lagging quadrant, entirely decoupled from the tech-led Liquidity vacuum.

- Defensive Bunkers Hold Firm: Despite the aggressive return of "risk-on" Capital into Tech, Health Care (XLV) and Consumer Staples (XLP) did not Yield. Both continue to print aggressive North-East trajectories high within the Improving quadrant, maintaining their status as premier structural bunkers.

- Cyclical Bifurcation Confirmed: The physical economy trade has split. Industrials (XLI) continues to accumulate relative strength within the Improving quadrant, but Materials (XLB) has rolled over, printing a South-East vector that invalidates its prior breakout.

The empirical momentum data from the May 14, 2026, session captures a market desperately establishing a bifurcated equilibrium. The Relative Rotation Graph (RRG) illustrates an environment where institutional capital is unwilling to underwrite broad economic expansion. Instead, flows are hyper-concentrated into two distinct extremes: the fortress balance sheets of pure-play technology and the non-yielding safety of traditional defensives. Everything else—from consumer growth to raw materials—is being systematically starved of relative momentum.

Sector Momentum and Trajectory Summary

The following chart and table details the momentum quadrant positioning and visual trail vectors for the 11 major US S&P 500 sectors based on the May 14 close:

US Sector Relative Momentum Chart (at the closing price of 14/05/2026). Powered by: amibroker.com

Quantitative Momentum Themes

The Return of the Solitary Anchor

The transition of Information Technology (XLK) back into the Leading quadrant is the most significant structural development of the week. After a brief period of momentum decay that threatened to leave the broader market without a safety net, XLK's aggressive North/North-East hook mathematically confirms a resumption of structural leadership. This signals that active managers have abandoned the search for new cyclical leadership and defaulted back to the secular certainty of semiconductors and enterprise software.

The Growth Triad is Dead

The RRG visually proves that buying generic "mega-cap growth" is mathematically flawed in the current regime. While XLK breaks out to the upside, Consumer Discretionary (XLY) is drifting horizontally (East) deep in the Lagging quadrant, completely devoid of upward velocity. Communication Services (XLC) is printing a tepid technical hook but remains structurally broken below the zero-line. The data confirms that institutional algorithms have permanently decoupled the tech anchor from the increasingly fragile consumer narrative.

The "Tech & Safety" Barbell

Typically, when Technology breaks out, defensive sectors begin to lose relative momentum. The May 14 data defies this historical correlation. Health Care (XLV) and Consumer Staples (XLP) continue to print powerful North-East trajectories high within the Improving quadrant. This "Tech + Safety" barbell dictates that capital is not becoming broadly risk-on. Instead, institutions are using XLK for Alpha generation while simultaneously utilizing XLV and XLP for Beta reduction, effectively preparing for continued macroeconomic turbulence.

The Cyclical Divorce

The physical economy trade has officially bifurcated. Earlier in the week, Industrials (XLI) and Materials (XLB) moved in lockstep. The May 14 data breaks that correlation. XLI continues to drift East/North-East, quietly accumulating relative strength (likely supported by aerospace/defense and specialized Manufacturing). However, XLB's trail has rolled over into a South-East vector, actively bleeding vertical momentum. This divergence suggests the market is willing to back domestic, final-stage manufacturing, but is actively liquidating exposure to global raw Commodity Demand.

The RRG momentum data from May 14 provides a highly specific blueprint for portfolio construction. The market is violently punishing homogenization. Active managers must embrace the "Tech + Safety" barbell, utilizing Information Technology (XLK) as the sole aggressive anchor, while maintaining maximum defensive ballast in Health Care (XLV) and Consumer Staples (XLP). Furthermore, the structural decoupling within growth and cyclicals demands ruthless stock-picking; exposure to Consumer Discretionary (XLY) and Materials (XLB) carries severe relative-strength risk, as both are actively being starved of institutional capital.

Please wait processing your request...

Please wait processing your request...