Key Highlights

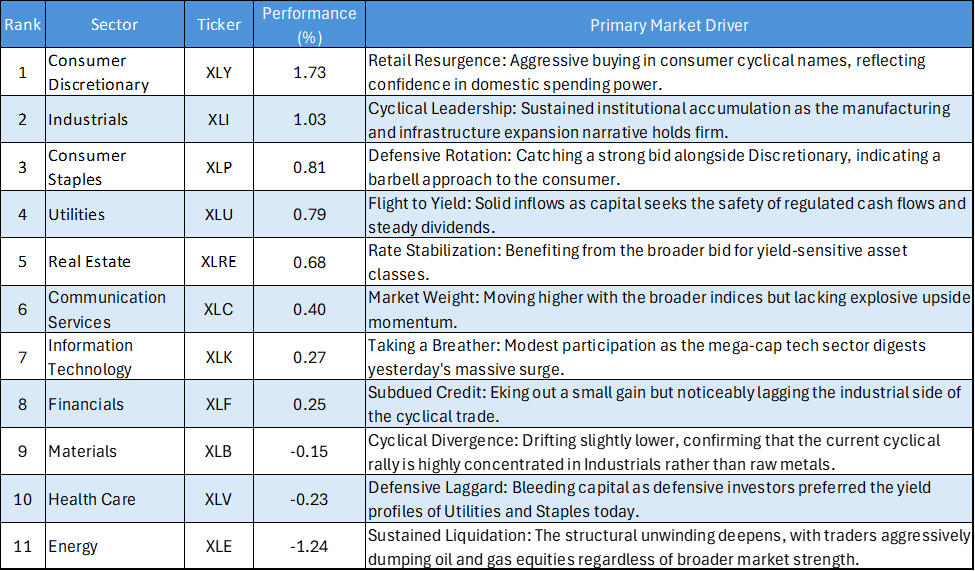

- The Consumer Flex: Consumer Discretionary (XLY) took the top spot, surging 1.73% and confirming that buyers are eagerly defending retail and consumer-facing equities after recent volatility.

- The Industrial Engine: Industrials (XLI) continued its dominant streak, advancing 1.03% to cement its status as the market's premier cyclical growth engine.

- Defensive Yield Catch a Bid: A notable rotation into safety and yield took place, with Consumer Staples (XLP), Utilities (XLU), and Real Estate (XLRE) all posting solid gains.

- Energy’s Relentless Unwinding: Energy (XLE) was the worst performer by a wide margin, dropping another 1.24% as institutional capital continues to aggressively liquidate the commodity trade.

The US equity market session on April 9, 2026, showcased a measured and highly selective "risk-on" environment. Rather than a broad-based explosion, capital flowed specifically toward consumer spending narratives and domestic manufacturing. At the same time, a healthy underlying bid for defensive sectors signaled that investors are balancing their cyclical bets with reliable yield, all while continuing to fund these moves by unwinding the Energy sector.

Daily US Sector Performance Summary 09/04/2026

The following table summarizes the day's performance across the 11 major US S&P 500 sectors, ordered from the strongest to the weakest:

Key Market Themes

The Discretionary Rebound

After a choppy few days, Consumer Discretionary (XLY) flexed its muscles with a market-leading 1.73% advance. This indicates that Wall Street is unwilling to abandon the consumer narrative. When investors aggressively buy Discretionary equities, they are essentially betting that employment will remain robust and that inflation is cooling enough to leave Americans with healthy disposable income.

Industrials Become the Chosen Cyclical

Industrials (XLI) posted another impressive more than 1% gain today. However, the rest of the cyclical complex did not follow suit, with Financials (XLF) mostly flat and Materials (XLB) closing in the red. This divergence is critical. It shows that institutional money is not blindly buying "economic recovery" stocks; rather, they are highly focused on the specific fundamental tailwinds of domestic manufacturing, defense, and infrastructure, anointing XLI as the undisputed cyclical leader.

The Bottomless Pit in Energy

The pain trade in Energy (XLE) is relentless. While the broader market was largely constructive, Energy shed another 1.24%. Over the past week, we have seen this sector transition from a mild cool-down into a full-blown structural liquidation. The "inflation hedge" era that dominated previous quarters is being aggressively unwound, and it appears value hunters are still hesitant to try and catch this falling knife.

Bottom Line

The price action on April 9 paints the picture of a sophisticated, functioning market. Investors are rewarding areas of genuine economic expansion, Consumer Discretionary and Industrials, while actively maintaining risk management through defensive allocations in Staples and Utilities. The major takeaway remains the total isolation of the Energy sector; until the selling pressure in XLE exhausts itself, investors should expect capital to continue rotating smoothly out of commodities and into the physical domestic economy.

Please wait processing your request...

Please wait processing your request...