Key Highlights

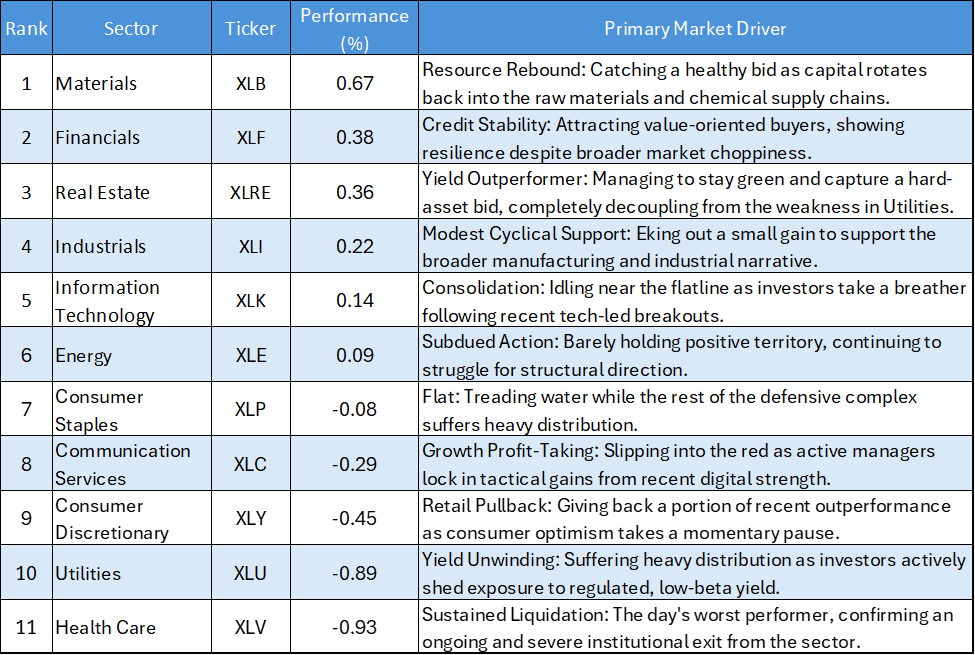

- Materials Take the Lead: Materials (XLB) paced the market with a solid 0.67% gain, signaling a renewed appetite for raw materials and hard assets.

- Financials Steady the Ship: Financials (XLF) posted a respectable 0.38% advance, indicating stabilizing sentiment in the banking and credit sectors.

- Tech Takes a Breather: The secular growth engine cooled off, with Information Technology (XLK) posting a muted 0.14% gain, while Consumer Discretionary (XLY) and Communication Services (XLC) slipped into the red.

- Defensive Liquidation Resumes: Traditional safety and yield proxies were aggressively sold off, with Health Care (XLV) and Utilities (XLU) finishing at the absolute bottom of the board, dropping 0.93% and 0.89%, respectively.

The US equity market session on April 20, 2026, showcased a subdued, fragmented, and highly rotational trading environment. Rather than a unified directional surge, institutional capital engaged in a quiet reshuffling—locking in recent gains from high-beta consumer and digital growth names to fund a measured rotation back into cyclical value and hard assets. Meanwhile, the aggressive purge of pure defensive sectors continued unabated.

Daily US Sector Performance Summary 20/04/2026

The following table summarizes the day's performance across the 11 major US S&P 500 sectors, ordered from the strongest to the weakest:

Key Market Themes

Cyclicals and Value Find a Floor

After suffering notable distribution late last week, the cyclical value complex managed to arrest its slide. The leadership of Materials (XLB) (+0.67%) and Financials (XLF) (+0.38%) suggests that value hunters are actively stepping in to support these sectors. When paired with the modest gain in Industrials (XLI), it indicates that institutional capital is not abandoning the economic expansion trade; they are simply demanding better entry points.

The Growth Engine Idles

The high-beta growth sectors that recently anchored the market took a collective pause. Information Technology (XLK) was virtually flat (+0.14%), while Consumer Discretionary (XLY) and Communication Services (XLC) suffered mild profit-taking. This price action does not indicate a structural breakdown in growth; rather, it reflects a healthy, quiet consolidation. Capital is taking a breather, digesting recent breakouts rather than blindly chasing momentum.

The Relentless Defensive Purge

The most definitive narrative on the tape remains the total avoidance of traditional safety assets. Health Care (XLV) and Utilities (XLU) were hammered, finishing deep in the red. The persistent liquidation in these areas confirms that investors are entirely uninterested in capital preservation strategies. Interestingly, Real Estate (XLRE) (+0.36%) managed to decouple from this trend, showing that capital prefers the hard-asset characteristics of property over the regulated yield of utilities or the demographic risks of pharmaceuticals.

Bottom Line

The price action on April 20 reflects a market in a state of healthy digestion. The lack of aggressive upward momentum in Tech is offset by the stabilizing bids in Materials and Financials, keeping the broader indices relatively insulated from violent swings. As long as the rotation remains constructive, moving from one risk-asset class to another rather than fleeing into cash or defensives, the underlying foundation of the market remains stable.

Please wait processing your request...

Please wait processing your request...