Key Highlights

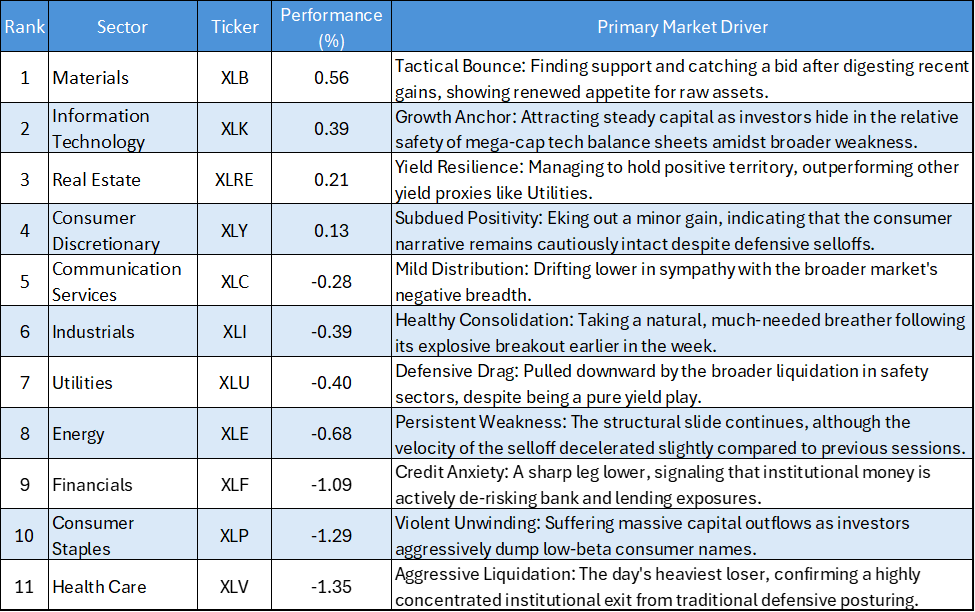

- Defensive Distribution: Traditional safety sectors suffered severe liquidation, with Health Care (XLV) and Consumer Staples (XLP) plunging 1.35% and 1.29%, respectively, finishing as the day's worst performers.

- Financials Take a Hit: The Financials (XLF) sector broke downward with a notable 1.09% drop, suggesting underlying concerns regarding credit or shifting yield curve dynamics.

- Materials Catch a Bid: After a recent cooling-off period, Materials (XLB) led the market higher, advancing 0.56% as buyers stepped back into raw metals and chemicals.

- Tech Anchors the Green: Information Technology (XLK) provided crucial stability at the top of the board, gaining 0.39% to prevent a deeper broader market slide.

The US equity market session on April 10, 2026, was characterized by targeted distribution and a decidedly mixed rotational undercurrent. Market breadth leaned negative, with seven of the eleven S&P 500 sectors closing in the red. Institutional capital aggressively abandoned traditional low-beta defensive sectors and large-cap financials, while rotating modestly into hard-asset cyclicals and secular tech growth.

Daily US Sector Performance Summary 10/04/2026

The following table summarizes the day's performance across the 11 major US S&P 500 sectors, ordered from the strongest to the weakest:

Key Market Themes

The Great Defensive Dump

The most defining feature of the April 10 session is the outright collapse of the market's defensive pillars. When Health Care (XLV) and Consumer Staples (XLP)—two sectors historically utilized for capital preservation—drop well over 1% in a single session, it signals a forceful structural realignment. Investors are decidedly stripping risk-averse, low-beta equities from their portfolios, opting instead to either raise cash or reallocate into growth and selective cyclicals.

Financials Flash a Warning Sign

While the defensive unwinding is notable, the 1.09% drop in Financials (XLF) is perhaps the most structurally concerning metric on the board. The banking and credit sector is the engine of the broader economy; a sharp selloff here often implies that bond market volatility or shifting rate expectations are compressing margins. If XLF cannot find a near-term floor, it will act as a heavy gravitational drag on the S&P 500.

A Divergent Cyclical Landscape

The cyclical trade has officially fractured into highly specific sub-narratives. Industrials (XLI) took a well-deserved -0.39% breather after its recent tear, which looks like routine profit-taking. Meanwhile, Materials (XLB) stepped up to lead the market (+0.56%), and Energy (XLE) continued its miserable streak of structural distribution (-0.68%). This divergence proves that the "buy everything cyclical" macro trade is over; investors are now demanding rigorous, sector-specific catalysts before committing capital.

Bottom Line

The price action on April 10 highlights a market actively digesting crosscurrents. The violent rejection of Health Care and Consumer Staples suggests that institutions are not positioning for a recession, yet the simultaneous weakness in Financials prevents a full-blown cyclical breakout. With Information Technology and Materials serving as the market's temporary lifeboats, investors are navigating a highly selective, stock-picker's environment where broad sector ETFs are increasingly masking severe underlying volatility.

Please wait processing your request...

Please wait processing your request...