Key Highlights

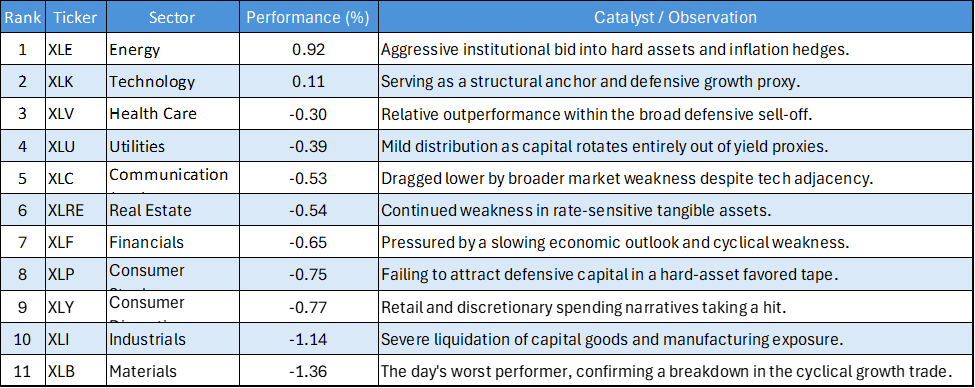

- The Energy Decoupling: Energy (XLE) stood out as the undisputed leader of the session, gaining 0.92% while the rest of the physical economy sectors suffered severe distribution.

- Cyclical Collapse: Materials (XLB) and Industrials (XLI) anchored the bottom of the tape, dropping 1.36% and 1.14% respectively, signaling a sharp halt to any economic expansion narratives.

- Tech as a Micro-Anchor: Information Technology (XLK) was the only other sector to finish in the green, scraping by with a 0.11% gain as investors used mega-caps as a zero-duration safety net.

- Broad Market Weakness: The breadth of the market was overwhelmingly negative, with 9 of the 11 major S&P 500 sectors closing in the red amid a pervasive "risk-off" tone.

The US equity market session on May 4, 2026, showcased a severely fractured tape characterized by a flight to hard assets and a rejection of cyclical growth. Capital actively fled traditional economic bellwethers, punishing manufacturing and raw materials, while simultaneously funneling into the Energy complex. This stark bifurcation suggests that the market is attempting to price in an environment of sticky inflation combined with slowing economic momentum, a classic stagflationary trade.

Daily US Sector Performance Summary 04/05/2026

The following table summarizes the day's performance across the 11 major US S&P 500 sectors, ordered from strongest to weakest:

Key Market Themes

Energy's Isolated Breakout

The defining feature of the session was the 0.92% rally in Energy (XLE). Crucially, this move happened in a vacuum. Normally, a booming global economy lifts all physical sectors—but on May 4, Materials (XLB) and Industrials (XLI) were heavily sold off. This decoupling confirms that the bid in Energy is not an "economic growth" trade; it is a defensive "inflation hedge" trade. Institutional capital is hiding in oil and gas to protect against sticky commodity pricing, completely abandoning the broader manufacturing base.

The Cyclical Wreckage

The industrial heartland of the market took severe damage. The 1.36% drop in Materials and the 1.14% drop in Industrials point to a sudden exhaustion of cyclical momentum. Investors are explicitly rejecting the narrative that a re-accelerating economy will boost demand for raw materials and heavy machinery, signaling concerns over global demand or squeezed corporate margins.

Tech Barely Holds the Line

In a sea of red, Information Technology (XLK) managed to keep its head above water, gaining 0.11%. While uninspiring on an absolute basis, this relative strength is critical. When defensive yield-proxies (Utilities, Staples) fail to provide safety, institutional capital defaults to the fortress balance sheets of mega-cap tech. XLK is currently being utilized not as a high-beta growth vehicle, but as a bunker.

Bottom Line

The tape from May 4 presents a highly defensive and bifurcated environment. The simultaneous collapse of Materials (XLB) and Industrials (XLI) against the aggressive outperformance of Energy (XLE) demands attention. The market is not rewarding broad economic participation; it is rewarding pure-play inflation hedges and the secular safety of mega-cap Technology (XLK). Active managers must respect this aggressive cyclical distribution and ensure they are not over-exposed to traditional manufacturing sectors until they can prove capable of catching a structural bid.

Please wait processing your request...

Please wait processing your request...