_05_12_2026_03_54_54_419559.jpg)

Key Highlights

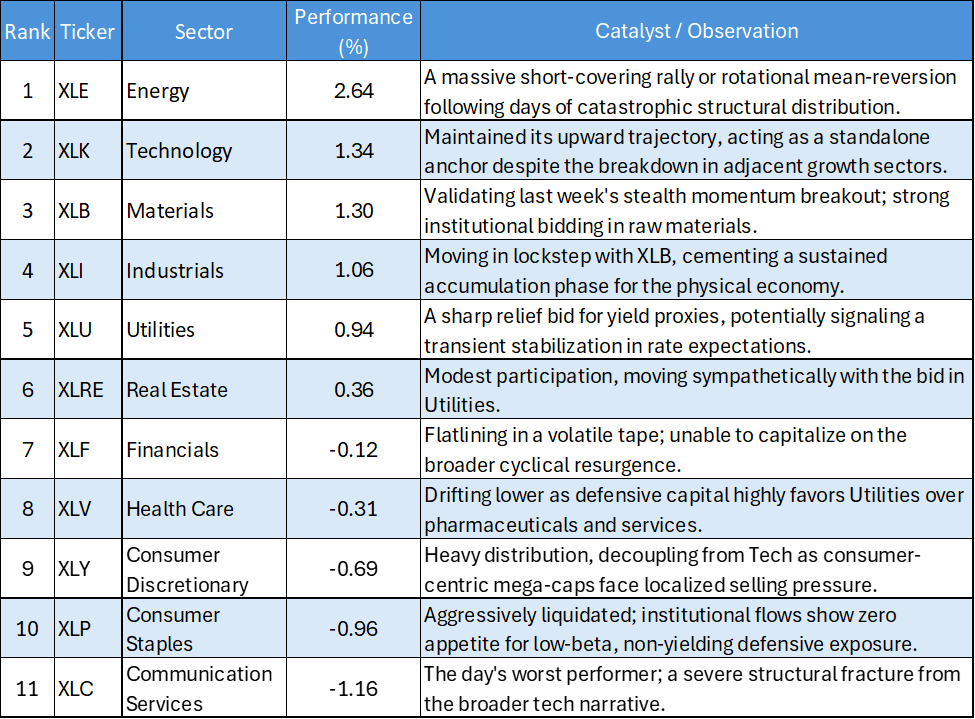

- Energy's Violent Mean Reversion: After suffering days of unrelenting structural Liquidation, Energy (XLE) exploded for a 2.64% gain. This massive counter-trend surge highlights extreme rotational Volatility in the Inflation-hedge trade.

- Cyclical Breakout Validated: The stealth quantitative accumulation spotted late last week is bearing fruit. Materials (XLB) and Industrials (XLI) posted robust gains of 1.30% and 1.06%, respectively, confirming institutional conviction in the physical economy.

- The Growth Triad Fractures: Mega-cap growth decoupled severely. While Technology (XLK) maintained its structural gravity with a 1.34% advance, Communication Services (XLC) plunged -1.16% and Consumer Discretionary (XLY) dropped -0.69%, signaling highly localized, stock-specific distribution.

- Defensive Bifurcation: Yield proxies caught a significant bid, with Utilities (XLU) jumping 0.94%. Conversely, traditional safety staples were actively sold, leaving Consumer Staples (XLP) anchoring the bottom of the tape at -0.96%.

The US Equity market session on May 11, 2026, delivered a highly bifurcated and structurally complex tape. Following the hyper-concentrated tech Liquidity vacuum of the previous session, institutional Capital rotated aggressively. The empirical data points to a market environment characterized by violent mean-reversion in heavily shorted or recently liquidated sectors (Energy), paired with a definitive fracturing of the mega-cap growth alliance.

Daily US Sector Performance Summary 11/05/2026

The following table summarizes the day's performance across the 11 major US S&P 500 sectors, ordered from strongest to weakest:

Key Market Themes

Energy's Dead-Cat Bounce or Structural Bottom?

The most glaring data point on the May 11 tape is the 2.64% explosion in Energy (XLE). For the last three sessions, the empirical data confirmed a catastrophic institutional unwinding of the oil patch. A violent, single-day surge of this magnitude is historically characteristic of aggressive short-covering rather than the immediate resumption of a primary uptrend. Active managers must heavily scrutinize the upcoming momentum data to determine if this is a tradable structural bottom or simply a mechanical mean-reversion trap.

The Cyclical Breakout is Confirmed

Late last week, quantitative momentum tools (like the RRG) flagged a "stealth breakout" in the cyclical complex, even as their absolute performance lagged. The May 11 tape empirically validated that signal. The synchronized more than 1% surges in both Materials (XLB) and Industrials (XLI) prove that the underlying structural accumulation was genuine. Institutional capital is actively Underwriting an economic re-acceleration narrative, entirely bypassing the Financials (XLF) sector in the process.

The Growth Triad is Broken

Historically, XLK, XLY, and XLC move with a high degree of mathematical correlation, acting collectively as the market's "Growth Triad." The May 11 session shattered that correlation. While Tech (XLK) surged 1.34%, Communication Services (XLC) imploded by -1.16%, creating a massive 250-basis-point spread between two supposedly adjacent mega-cap sectors. This divergence indicates that passive index flows are no longer lifting the entire growth complex; active managers are ruthlessly differentiating between semiconductor/hardware strength and Social Media/telecom weakness.

Defensive Rotational Whiplash

The defensive complex experienced intense internal bifurcation. Capital aggressively exited Consumer Staples (XLP, -0.96%) and Health Care (XLV, -0.31%), but violently accumulated Utilities (XLU, +0.94%). This rotational whiplash suggests a highly specific macroeconomic bet being placed on falling yields or regulatory stability, rather than a broad-based, panic-driven flight to safety.

The empirical data from May 11 demands tactical agility. The tape proves that assuming homogeneous sector performance is currently a mathematically flawed strategy, as evidenced by the severe XLK/XLC decoupling. Portfolios must align with the confirmed structural breakouts in the physical economy (XLI, XLB) while treating the violent surge in Energy (XLE) with strict risk-management protocols until secondary quantitative confirmation establishes a true momentum floor.

Please wait processing your request...

Please wait processing your request...