Key Highlights

- Growth Takes Command: Information Technology (XLK) and Consumer Discretionary (XLY) dominated the session, surging 1.60% and 1.49%, respectively, as investors aggressively chased high-beta secular growth.

- Financials Find Footing: Financials (XLF) posted a solid 0.75% gain, offering some relief to the credit space after recent underperformance.

- The Cyclical Reversal: Yesterday's leaders became today's laggards. Industrials (XLI) and Materials (XLB) suffered heavy distribution, dropping 1.25% and 1.21% as capital rotated out of hard assets.

- Defensive Liquidation: Pure yield and safety proxies were abandoned, with Utilities (XLU) and Health Care (XLV) shedding 0.97% and 0.71%, respectively.

The US equity market session on April 15, 2026, was defined by a highly polarized, aggressive rotation. Institutional capital definitively favored secular growth and consumer strength while rapidly unwinding exposure to both traditional defensive sectors and heavy manufacturing cyclicals. This targeted "risk-on" behavior suggests a market increasingly confident in tech-driven expansion but skeptical of the broader industrial supply chain's near-term momentum.

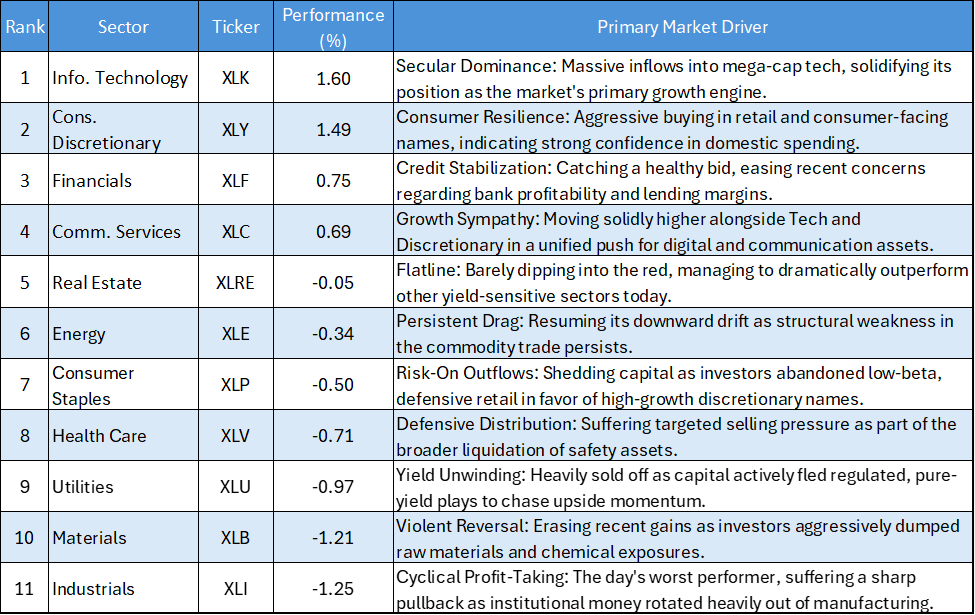

Daily US Sector Performance Summary 15/04/2026

The following table summarizes the day's performance across the 11 major US S&P 500 sectors, ordered from the strongest to the weakest:

Key Market Themes

The Growth Engine Roars

The defining narrative of April 15 is the undeniable dominance of the growth complex. When Information Technology (XLK) (+1.60%), Consumer Discretionary (XLY) (+1.49%), and Communication Services (XLC) (+0.69%) all cluster at the top of the leaderboard, it signals a forceful, unified bet on secular expansion. Buyers are actively prioritizing companies with high earnings multiples and consumer-facing business models, shaking off macro anxieties to chase pure momentum.

The Cyclical Trade Fractures

In a violent pivot from recent sessions, the industrial economy took a massive hit. Industrials (XLI) and Materials (XLB) finished dead last, tumbling 1.25% and 1.21%, respectively. This indicates severe profit-taking and a potential structural rotation away from the "hard asset" trade. Investors who had been hiding in manufacturing and raw materials suddenly used those sectors as a funding source to fuel their aggressive tech and discretionary purchases.

Defensives Left in the Dust

In a tape dominated by risk appetite, capital preservation became an active liability. Utilities (XLU), Health Care (XLV), and Consumer Staples (XLP) all suffered meaningful distribution. When the market decides to sprint, low-beta yield proxies are the first to be jettisoned. Interestingly, Real Estate (XLRE) (-0.05%) managed to tread water, showing that some pockets of the yield market are still retaining baseline institutional support despite the broader defensive purge.

Bottom Line

The price action on April 15 paints the picture of a market committing heavily to a "growth-first" paradigm. The synchronized surge in Tech and Discretionary, funded directly by liquidating Industrials, Materials, and Defensives, shows that active managers are no longer trying to balance the barbell, they are tilting it entirely toward risk. Until this momentum exhausts itself, fighting the tech-led tape remains a dangerous proposition.

Please wait processing your request...

Please wait processing your request...