Key Highlights

- The Tech Liquidity Vacuum: Information Technology (XLK) delivered a market-skewing 3.44% surge. This massive influx of Capital effectively drained liquidity from the rest of the tape, creating an extreme performance divergence.

- Fractured Market Breadth: Despite the explosive move in tech, the broader market showed an alarming lack of participation. Only four other sectors managed to close in the green, none exceeding a fractional 0.37% gain.

- Defensive Distribution Accelerates: Capital actively fled traditional Yield proxies and safety sectors, leaving Utilities (XLU) and Health Care (XLV) anchoring the bottom of the board with -0.89% and -0.85% declines, respectively.

- Cyclical Stagnation: The physical economy remains devoid of sustained institutional conviction. Industrials (XLI) fell -0.46%, while Materials (XLB) managed only a muted 0.37% bounce, confirming the absence of a broad economic re-acceleration trade.

The US Equity market session on May 8, 2026, was defined by hyper-concentration. Institutional capital bypassed the broader market entirely, forcefully allocating into the secular growth and fortress balance sheets of the mega-cap tech complex. When a single sector posts a +3.44% gain while six major sectors close in the red, the empirical data points to a tape driven by passive flows and FOMO (Fear Of Missing Out) within a highly isolated pocket of the market, rather than a fundamentally sound, broad-based economic expansion.

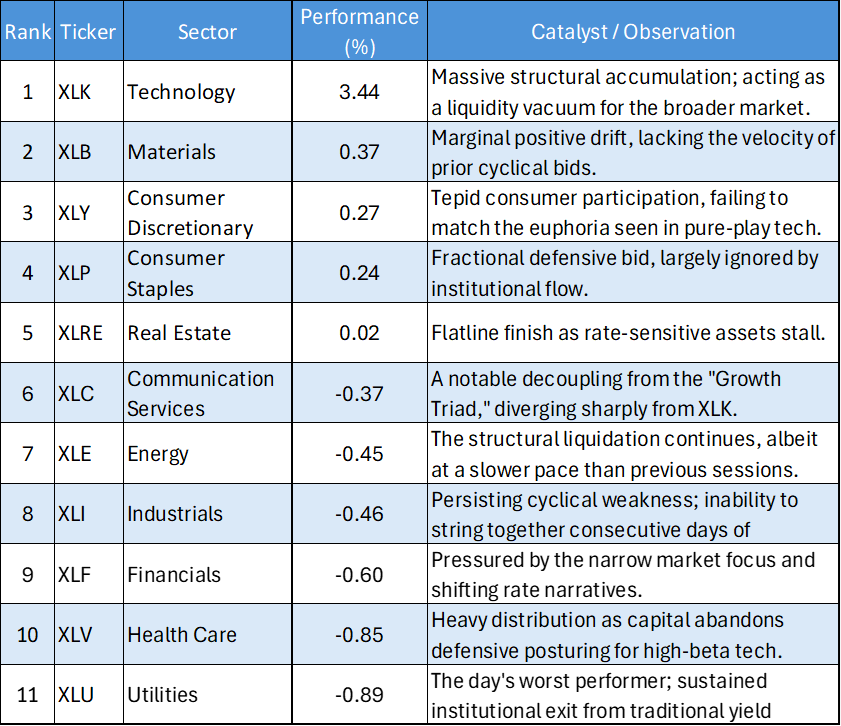

Daily US Sector Performance Summary 08/05/2026

The following table summarizes the day's performance across the 11 major US S&P 500 sectors, ordered from strongest to weakest:

Key Market Themes

Tech's Extreme Hyper-Concentration

- A 3.44% single-day move in a mega-cap sector like Information Technology (XLK) is a statistical outlier. This price action suggests aggressive institutional buying, likely driven by semiconductor momentum or AI-adjacent hardware. However, this magnitude of outperformance often acts as a liquidity vacuum. Capital isn't entering the market to lift all boats; it is actively being harvested from other sectors to fund the concentrated tech bid.

The Communication Services Anomaly

- In a session where XLK exploded by over 3%, the negative finish for Communication Services (XLC) at -0.37% is a critical quantitative divergence. Typically, these mega-cap sectors move in tandem as the market's primary growth engines. This decoupling indicates highly specific, stock-level weakness within the Social Media or telecom heavyweights that make up XLC, preventing it from catching the broader tech tailwind.

The Unrelenting Defensive Bleed

- The market is explicitly rejecting yield proxies. The bottom of the tape was firmly anchored by Utilities (XLU) and Health Care (XLV). When investors are aggressively chasing a 3.4% tech rally, the Opportunity cost of holding slow-growth, Dividend-paying defensive sectors becomes too high. The data confirms a sustained unwinding of the safety trade.

Cyclical Conviction Evaporates

- Following the violent rotational whiplash seen earlier in the week, the physical economy sectors failed to mount a meaningful recovery. Industrials (XLI) bled another -0.46%, and Materials (XLB) barely scraped together a 0.37% gain. The statistical footprint of the Manufacturing and value trade shows an environment completely devoid of structural momentum, leaving cyclical breakout traders stranded.

The empirical data from May 8 demands that active managers recognize the tape for what it is: a one-sector market. The explosive +3.44% surge in Technology (XLK) masks deep underlying breadth issues, as the majority of the S&P 500 sectors either flatlined or suffered distribution. While fighting the tech momentum is mathematically dangerous, aggressively expanding exposure into cyclicals or defensives right now lacks statistical justification. Portfolios must ensure they have sufficient exposure to the XLK liquidity vacuum, while maintaining strict risk management on the lagging physical economy and yield-proxy sectors.

Please wait processing your request...

Please wait processing your request...