_05_06_2026_03_41_01_537007.jpg)

Key Highlights

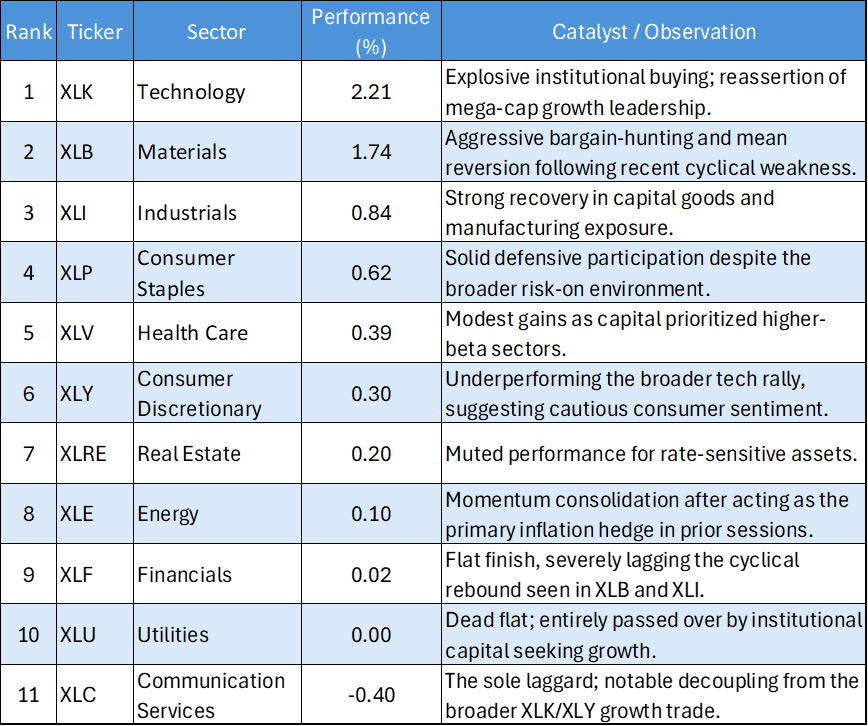

- Tech Reclaims the Tape: Information Technology (XLK) dominated the session with a massive 2.21% surge, signaling an aggressive return of capital into mega-cap growth and semiconductor leadership.

- Cyclical Rebound: After experiencing severe distribution in recent sessions, Materials (XLB) and Industrials (XLI) staged a sharp recovery, gaining 1.74% and 0.84% respectively.

- Communication Services Decouples: In a rare divergence from its tech-adjacent peers, Communication Services (XLC) was the sole sector to finish in the red, dropping 0.40%.

- Energy Takes a Breather: Following a period of explosive, decoupled momentum, the Energy sector (XLE) cooled off, finishing practically flat with a marginal 0.10% gain.

The US equity market session on May 5, 2026, was characterized by a powerful "risk-on" rally led squarely by the Technology sector. Unlike recent sessions defined by defensive rotations and hard-asset inflation hedges, capital flowed back into historical growth engines and beaten-down cyclical value. With 9 of the 11 major S&P 500 sectors closing in positive territory, the tape exhibited a healthy breadth that suggests an easing of immediate macroeconomic fears and a renewed appetite for risk.

Daily US Sector Performance Summary 05/05/2026

The following table summarizes the day's performance across the 11 major US S&P 500 sectors, ordered from strongest to weakest:

Key Market Themes

The Tech Engine Roars Back

The standout feature of May 5 was the absolute dominance of Information Technology (XLK), which gained 2.21%. This aggressive bid suggests that any recent weakness in the sector was viewed by institutional investors as a buying opportunity rather than a structural breakdown. When the market decides to take on risk, it continues to default to the secular growth and fortress balance sheets found within the tech complex.

The Cyclical Mean Reversion

Perhaps the most encouraging sign for the broader market was the sharp recovery in the physical economy sectors. Materials (XLB) surged 1.74% and Industrials (XLI) added 0.84%. This suggests that the severe liquidation seen in these sectors over the past few days may have been overextended. Investors stepped in to buy the dip, hinting at a refusal to completely abandon the narrative of economic resilience.

The Communication Services Anomaly

Usually, Information Technology (XLK), Consumer Discretionary (XLY), and Communication Services (XLC) move with a high degree of correlation as the market's "Growth Triad." However, XLC completely decoupled on Tuesday, falling 0.40% to become the worst performer on the board. This indicates highly specific, stock-level weakness within the mega-cap media or telecommunications space that dragged the broader sector down despite the tech euphoria.

Energy Consolidates

Energy (XLE), which had been the market's undisputed momentum leader and inflation hedge, took a back seat with a muted 0.10% gain. This isn't necessarily a sign of weakness, but rather a healthy consolidation. As capital rotated aggressively back into Tech and beaten-down Materials, the immediate urgency to hide in hard assets temporarily subsided.

Bottom Line

The tape from May 5 is a loud reminder of Technology's underlying gravity in the modern market. The massive outperformance of XLK dictates that active managers cannot afford to be structurally underweight on growth when risk appetite returns. However, the simultaneous bid in Materials (XLB) and Industrials (XLI) is what makes this session particularly constructive. If Tech can maintain its leadership while cyclicals participate in the upside, it points to a much healthier, broader market foundation than the defensive, stagflationary tape witnessed in recent days.

Please wait processing your request...

Please wait processing your request...