_05_15_2026_03_36_36_115717.jpg)

Key Highlights

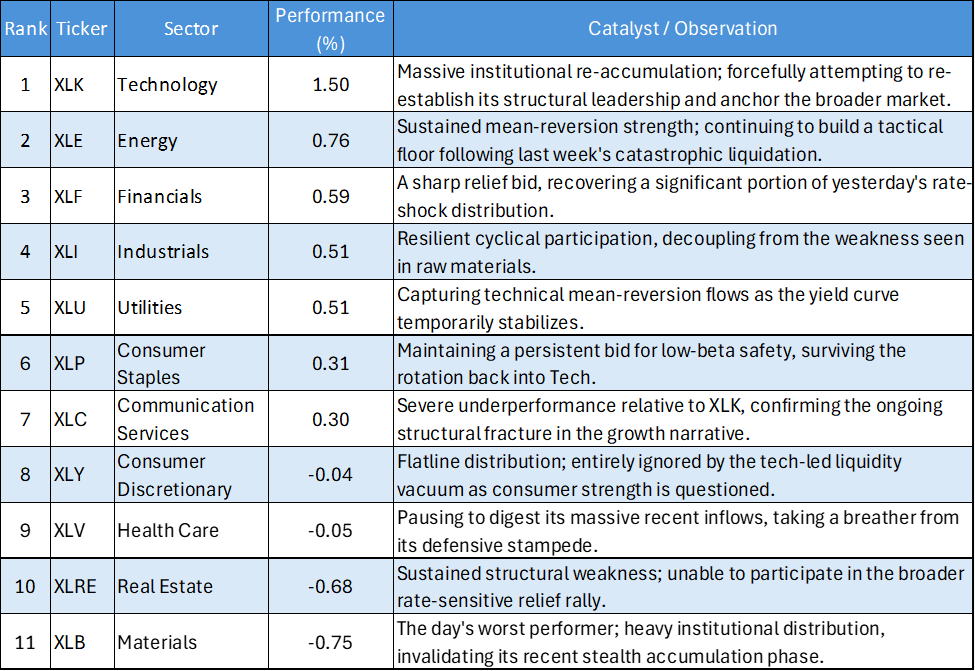

- Tech's Solitary Resurgence: Information Technology (XLK) reasserted its dominance with a commanding 1.50% surge. After a brief period of structural weakness, institutional Capital forcefully re-engaged the market's primary mega-cap anchor.

- The Growth Triad Remains Broken: Despite XLK's explosive move, the broader growth complex failed to follow. Communication Services (XLC) managed a tepid 0.30% gain, while Consumer Discretionary (XLY) actually closed in the red at -0.04%, cementing a massive divergence within mega-cap growth.

- Rate-Shock Relief Bid: Following yesterday's violent, Yield-driven Liquidation, rate-sensitive sectors caught a stabilizing bid. Financials (XLF) recovered 0.59% and Utilities (XLU) bounced 0.51%, though Real Estate (XLRE) continued to bleed at -0.68%.

- Cyclical Bifurcation: The physical economy split cleanly in two. While Industrials (XLI) posted a solid 0.51% gain, Materials (XLB) was aggressively distributed, finishing as the worst performer on the board at -0.75%.

The US Equity market session on May 14, 2026, was characterized by a distinct narrowing of institutional risk appetite. Rather than a broad-based "risk-on" rally, the empirical data points to highly concentrated, stock-specific accumulation. Capital flowed aggressively back into the perceived fortress balance sheets of pure-play technology, creating a Liquidity vacuum that starved consumer-facing growth and raw materials of participation. The tape reflects a market attempting to stabilize its structural foundation, but refusing to underwrite a synchronized economic expansion.

Daily US Sector Performance Summary 14/05/2026

The following table summarizes the day's performance across the 11 major US S&P 500 sectors, ordered from strongest to weakest:

Key Market Themes

The Return of the Solitary Anchor

After plunging into the Weakening quadrant earlier in the week, Information Technology (XLK) engineered a critical Reversal. A 1.50% single-day gain requires massive, sustained institutional buying. This indicates that active managers, spooked by the Leadership void and the recent rate-shock Volatility, have once again decided that pure-play tech is the only durable hiding place in the S&P 500. XLK is currently acting as a liquidity sponge, draining capital from the rest of the tape to fund its own velocity.

The Permanent Fracture of Mega-Cap Growth

The most mathematically glaring feature of the May 14 tape is the massive 154-basis-point spread between Tech (XLK, +1.50%) and Consumer Discretionary (XLY, -0.04%). In previous market regimes, these sectors moved in near-perfect lockstep. The empirical data now proves that the "Growth Triad" is permanently fractured. Institutional algorithms are ruthlessly differentiating between semiconductor/enterprise-software strength and the fragility of the consumer discretionary wallet. Buying generic "mega-cap growth" ETFs is no longer a viable proxy for capturing tech's Alpha.

Rate-Shock Stabilization

The aggressive selling that decimated yield proxies and banks yesterday found an immediate floor. The synchronized bounces in Financials (XLF, +0.59%) and Utilities (XLU, +0.51%) suggest that the Bond Market panic was a transient shock rather than the start of a sustained structural repricing. However, the continued bleeding in Real Estate (XLRE, -0.68%) warns that highly leveraged, capital-intensive balance sheets remain squarely in the crosshairs of macro risk managers.

Cyclical Bifurcation

The physical economy trade is sending mixed signals. Industrials (XLI) posted a respectable 0.51% gain, suggesting continued faith in domestic Manufacturing or aerospace/defense resilience. Conversely, Materials (XLB) was heavily liquidated, dropping -0.75%. This divergence indicates that while final-stage manufacturing is holding its structural bids, the market is actively betting against global raw material and Commodity Demand, effectively unwinding the stealth accumulation phase spotted last week.

The empirical data from May 14 demands extreme tactical precision. The tape confirms that Information Technology (XLK) is the only sector possessing true, market-moving velocity, while the broader growth complex (XLY, XLC) is suffering from severe relative decay. Portfolios must be aligned with this hyper-concentrated tech leadership while recognizing the extreme fragility of the consumer narrative. Furthermore, the sharp divergence within the cyclical space dictates that active managers should isolate long exposure to Industrials (XLI) while aggressively cutting losses in the deteriorating Materials (XLB) complex.

Please wait processing your request...

Please wait processing your request...