Key Highlights

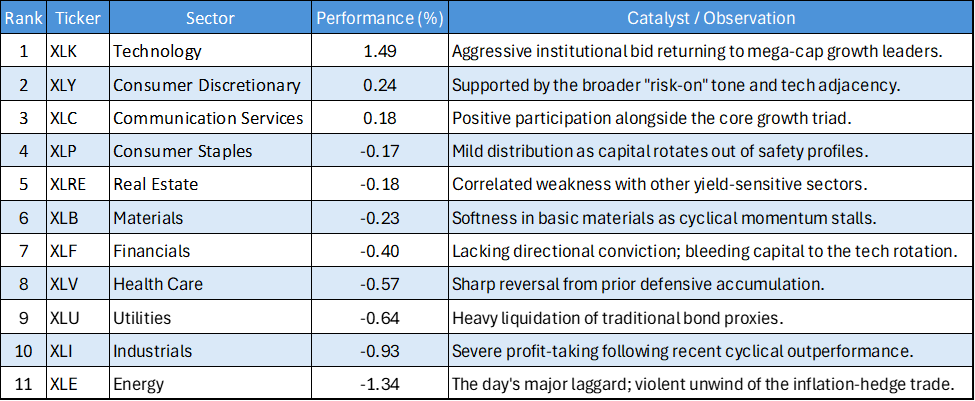

- Tech Reclaims the Throne: Information Technology (XLK) dominated the session, surging 1.49% in a powerful Reversal, re-establishing itself as the market's primary growth engine.

- The Growth Triad Leads: The only sectors to finish in positive territory were the traditional mega-cap growth pillars: Tech (XLK), Consumer Discretionary (XLY), and Communication Services (XLC).

- Defensive Liquidation: In a stark contrast to recent sessions, Yield proxies were aggressively sold. Utilities (XLU) dropped 0.64% and Health Care (XLV) fell 0.57%.

- Energy Pullback: After a period of structural bidding, Energy (XLE) was the day's worst performer, plunging 1.34% as investors rotated out of hard Assets and back into secular growth.

The US Equity market session on May 1, 2026, showcased a violent snapback in risk appetite, characterized by a massive rotation back into mega-cap technology and growth. The session was a mirror opposite of previous defensive-led tapes, with institutional Capital abandoning safety proxies and cyclical value in favor of the high-Beta tech trade. This price action suggests a market swiftly returning to its historical Leadership structure as investors deploy Capital into secular growth themes.

Daily US Sector Performance Summary 01/05/2026

The following table summarizes the day's performance across the 11 major US S&P 500 sectors, ordered from strongest to weakest:

Key Market Themes

The Re-emergence of the Growth Triad

The most glaring takeaway from May 1 is the absolute concentration of positive performance at the top of the risk spectrum. XLK, XLY, and XLC were the only sectors to survive the session in the green. The 1.49% gap-up in Tech (XLK) represents a forceful statement from institutional buyers that the secular growth narrative remains intact. When the market wants risk, it continues to find its highest conviction in Silicon Valley balance sheets rather than the broader economy.

The Defensive and Cyclical Unwind

Sectors that had recently enjoyed a renaissance as "safe havens" or value plays were systematically dismantled. Industrials (XLI), which had been showing strong Leadership, was slammed down 0.93%. Simultaneously, the defensive Yield-proxies, Utilities (XLU) and Health Care (XLV), suffered heavy distribution. This simultaneous selling of both cyclical Manufacturing and defensive safety indicates a pure, concentrated funding mechanism to fuel the tech rally.

Energy Exhaustion

After displaying severe vertical momentum in recent data, Energy (XLE) completely decoupled to the downside, dropping 1.34%. This sharp pullback suggests that the recent structural bid into energy as an Inflation hedge may have become overextended, triggering a wave of profit-taking. It serves as a reminder of the sector's high Volatility and susceptibility to rapid momentum shifts when the broader market pivots back to tech.

The tape from May 1 dictates a clear message: the tech-led growth trade is far from dead. The aggressive outperformance of XLK juxtaposed against the severe Liquidation of XLE, XLI, and XLU proves that when market sentiment flips to "risk-on," Capital flows are highly concentrated and unforgiving to off-trend sectors. Active managers must remain agile; while value and defensives had a moment in the sun, the underlying structural gravity of the market continues to pull Capital back toward mega-cap technology.

Please wait processing your request...

Please wait processing your request...