Key Highlights

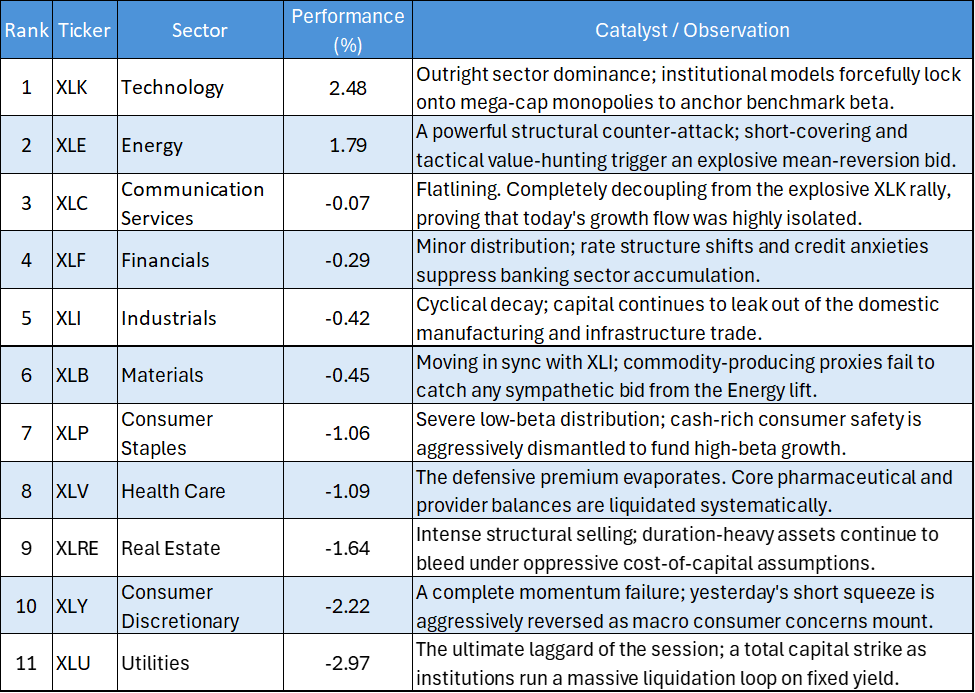

- The Tech Anchor Surges Dominantly: Information Technology (XLK) completely hijacked the tape, exploding for a massive 2.48% gain. Programmatic models aggressively concentrated Liquidity back into mega-cap tech, treating it as the ultimate shelter for broad-market Beta.

- Energy Ignites a Powerful Counter-Rally: Reversing its recent multi-day distribution, Energy (XLE) staged a violent mean-reversion move, surging 1.79% to claim the number two spot on the leaderboard.

- The High-Beta Consumer Complex Capitulates: Following its short-lived mechanical squeeze, Consumer Discretionary (XLY) was ruthlessly liquidated, plunging -2.22% as active managers aggressively unwound retail and consumer exposure.

- Defensive and Yield Bunkers Decimated: The premium on absolute safety completely collapsed. Utilities (XLU) suffered a catastrophic -2.97% flushing, while Real Estate (XLRE, -1.64%), Health Care (XLV, -1.09%), and Consumer Staples (XLP, -1.06%) were heavily used as funding sources.

The US Equity market session on June 1, 2026, kicked off the new trading month with a highly concentrated, zero-sum rotational whiplash. The absolute performance matrix reveals a market that has aggressively narrowed its Leadership profile. Institutional algorithms ruthlessly hollowed out the defensive, rate-sensitive, and consumer footprints across the S&P 500 to fund a highly aggressive, dual-pronged allocation into secular Technology monopolies and a resurrected Energy complex.

Daily US Sector Performance Summary

The following table summarizes the day's performance across the 11 major US S&P 500 sectors, ordered from strongest to weakest:

Key Market Themes

The Absolute Tech Concentration

The defining feature of the session is the sheer insulation of Information Technology (XLK, 2.48%). While 9 out of 11 sectors closed firmly in the red, mega-cap tech acted as a giant liquidity vacuum. When programmatic trading desks face a fragmented macroeconomic landscape, they consistently consolidate risk into the most liquid, cash-rich sector on earth. This extreme narrowness suggests that broad index health is highly artificial, relying entirely on a singular technology engine to mask deep underlying rot across the rest of the market.

The Energy Counter-Attack

Following deep structural damage and severe Capital extraction last week, Energy (XLE) executed a high-velocity 1.79% counter-rally. Given the massive damage previously inflicted on the sector, this move bears the unmistakable mathematical footprint of institutional short-covering blended with systematic value-hunting at validated technical floors. Crucially, because the materials sector (XLB) failed to participate, this energy bid remains isolated to oil and gas pricing metrics rather than a broad-based endorsement of the physical economy.

The High-Beta Consumer Collapse

Any structural thesis backing a consumer turnaround was utterly crushed today. Consumer Discretionary (XLY) plummeted -2.22%, completely wiping out its recent short-squeeze gains. This rapid Reversal confirms that long-term institutional capital is completely absent from the retail complex. Programmatic systems treated the brief bounce as a highly efficient entry point to reload macro short positions, viewing consumer balance sheets as highly vulnerable to ongoing cyclical deceleration.

The Complete Defensive Demolition

The traditional defensive playbook was not just broken today; it was entirely demolished. The synchronized flushing of Utilities (XLU, -2.97%), Real Estate (XLRE, -1.64%), Health Care (XLV, -1.09%), and Consumer Staples (XLP, -1.06%) confirms a massive, coordinated capital extraction program. Institutional allocators did not seek safety in low-beta or fixed-yield Assets. Instead, they treated these sectors as ATMs, stripping away defensive protection to aggressively underwrite the massive momentum surges inside XLK and XLE.

The performance data from June 1 mandates a highly concentrated, non-diversified approach to asset allocation. The tape has forcefully rejected cyclical value, defensive income, and consumer growth proxies, locking itself into a highly polarized framework. Active managers must rigorously align with this brutal zero-sum reality: maintain direct, heavy exposure to the secular anchor in Technology (XLK), treat the sharp rebound in Energy (XLE) with immediate tactical parameters, and ruthlessly avoid the catching of falling knives across the shattered defensive and discretionary complexes.

Please wait processing your request...

Please wait processing your request...