Key Highlights

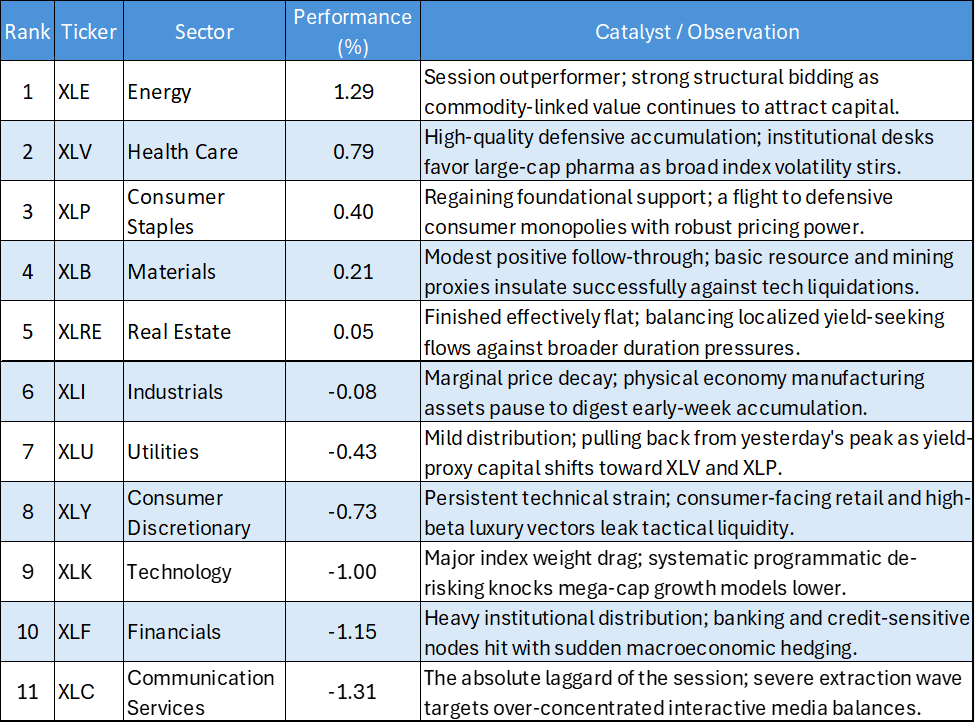

- Energy Powers to the Outright Lead: Defying broader benchmark headwinds, Energy (XLE) dominated the session, surging 1.29% as long-term institutional asset allocators aggressively added to structural value and Inflation-sensitive exposure.

- The High-Beta Growth Triad is Severely Punished: The secular mega-cap growth engine experienced a sweeping Capital extraction wave. Communication Services (XLC) plummeted -1.31%, Financials (XLF) slid -1.15%, and Information Technology (XLK) dropped -1.00% as institutional desks aggressively trimmed top-heavy index dependencies.

- Defensive Bunkers Recover Selective Bids: Active managers seeking safe-haven insulation pivoted back into non-Yield safety. Health Care (XLV) locked in a solid 0.79% gain, working in tandem with a steady 0.40% accumulation lift in Consumer Staples (XLP).

- Yield Proxies Face Intermittent Fatigue: Following yesterday's session-leading performance, interest-rate-sensitive Assets cooled off. Utilities (XLU) drifted lower to finish at -0.43%, proving that capital is migrating toward defensive balance sheets rather than pure Dividend duration.

The US Equity market session on June 3, 2026, executed a high-conviction, inverse-beta rotation that firmly penalized overextended growth balances. The absolute performance matrix reveals a disciplined zero-sum environment where programmatic models systematically drained Liquidity from the market's historical mega-cap pillars (XLC, XLF, XLK) to directly underwrite a robust defensive and old-economy value footprint.

Daily US Sector Performance Summary

The following table summarizes the day's performance across the 11 major US S&P 500 sectors, ordered from strongest to weakest:

Key Market Themes

The Growth Triad Unwind

The most actionable quantitative footprint on the June 3 tape is the unified collapse at the bottom of the board: Communication Services (XLC, -1.31%), Financials (XLF, -1.15%), and Information Technology (XLK, -1.00%). When these three highly concentrated, high-beta engines face synchronized, deep-red liquidations, it signals an intentional macro de-risking script. Programmatic trading desks are actively reducing single-stock concentration risk, treating the overextended growth complex as an index-wide ATM to reduce gross portfolio exposure.

The Commodity Value Standout

In stark contrast to the growth slaughter, Energy (XLE) re-established absolute dominance with a robust 1.29% advance, accompanied by a resilient green print in Materials (XLB, 0.21%). This performance proves that institutional appetite for Tangible Asset exposure remains structurally sound. Allocators are actively pairing their technology short-allocations with natural resource longs, exploiting structural Supply constraints to build an absolute value barbell that remains immune to multi-cap growth Rebalancing.

High-Quality Defensive Sorting

A clean technical reallocation developed across the market's defensive perimeters today. While duration-heavy yield proxies like Utilities (XLU, -0.43%) suffered localized exhaustion, asset managers funneled robust liquidity into cash-rich, high-Margin alternatives. Health Care (XLV, 0.79%) and Consumer Staples (XLP, 0.40%) served as the primary safe-haven hideouts, indicating that institutional risk parameters currently favor pristine corporate balance sheets over interest-rate-sensitive dividend duration.

Cyclical Momentum Hits a Speedbump

The marginal cooling seen in Industrials (XLI, -0.08%) demonstrates that while the physical economy rotation remains fundamentally supported, it lacks the speculative fast-money sponsorship required to climb vertically day after day. Algorithmic desks are executing this rotation with high-vetted patience, incrementally collecting cyclical components on minor intraday pullbacks rather than chasing absolute green tape into overhead technical resistance.

The empirical return data from June 3 demands an immediate, disciplined pivot toward value insulation and defensive quality. The session has forcefully exposed the vulnerability of passive, index-weighted portfolios that rely exclusively on mega-cap growth architectures. Active managers must rigorously realign with today's explicit cash migrations: scale down over-concentrated balances in Communication Services (XLC) and Technology (XLK), maintain an active long tilt in the structurally supported Energy (XLE) patch, and actively deploy defensive allocations into large-cap Health Care (XLV) and Staples (XLP) to anchor portfolios against ongoing index-level distribution.

Please wait processing your request...

Please wait processing your request...