Key Highlights

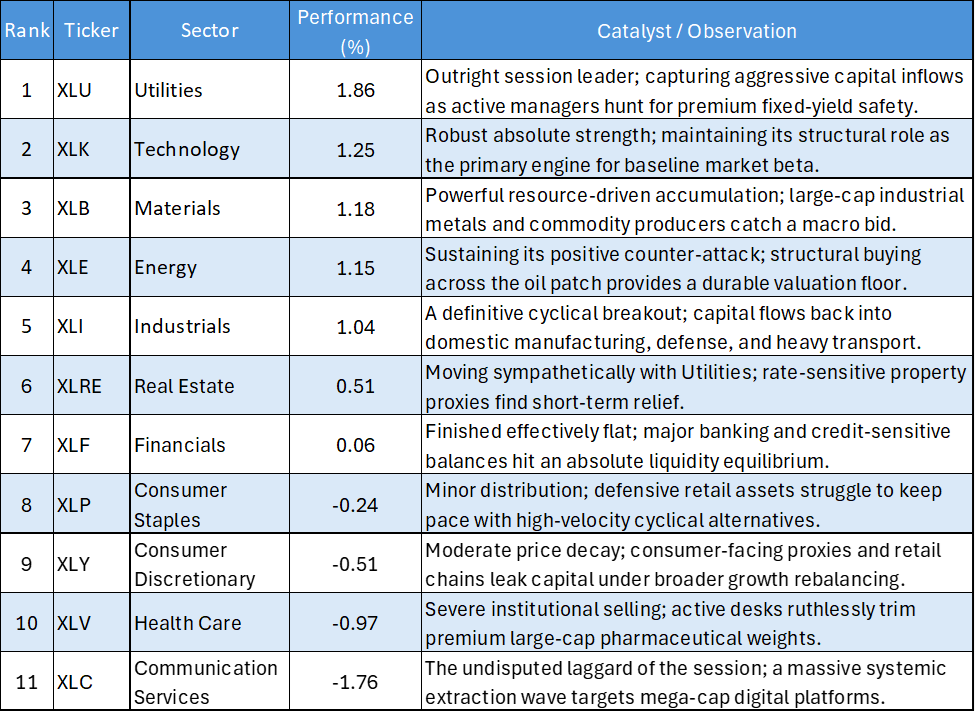

- Utilities Capture the Session Crown: Defying the broader risk-on undertone of the cyclical sectors, Utilities (XLU) led the absolute performance board with a robust 1.86% surge, catching an aggressive safety and Yield-seeking allocation bid.

- The Tech Heavyweight Retains Breadth: Information Technology (XLK) maintained its absolute upside velocity, gaining 1.25% as mega-cap tech continued to act as a primary destination for benchmark Liquidity.

- The Physical Economy Unifies in the Green: A highly synchronized Capital wave lifted the entire Commodity and Manufacturing complex. Materials (XLB, 1.18%), Energy (XLE, 1.15%), and Industrials (XLI, 1.04%) all expanded across a unified front, clearing the +1.00% threshold.

- Communication Services Aggressively Liquidated: In a sharp growth decoupling event, Communication Services (XLC) crashed to the absolute bottom of the board, plummeting -1.76% as institutional desks aggressively rotated out of major digital media and interactive segments.

The US Equity market session on June 2, 2026, printed a highly structured, non-correlated tape characterized by a robust revival across the physical economy and defensive yield proxies. The absolute performance matrix reveals a fascinating environment where institutional allocators simultaneously funded rate-sensitive duration anchors (XLU) and a powerful cyclical value block (XLB, XLE, XLI), directly using targeted liquidations in Communication Services (XLC) and Health Care (XLV) to finance the rotation.

Daily US Sector Performance Summary

The following table summarizes the day's performance across the 11 major US S&P 500 sectors, ordered from strongest to weakest:

Key Market Themes

The Fixed-Yield Flight

The absolute dominance of Utilities (XLU, 1.86%) accompanied by a supportive lift in Real Estate (XLRE, 0.51%) indicates that institutional models are selectively re-engaging with pure interest-rate-sensitive proxies. This targeted allocation into high-Dividend duration Assets suggests that bond-market yield structures may be flashing a short-term cooling signal, allowing programmatic systems to confidently rebuild defensive yield positions that were aggressively discarded earlier in the week.

The Physical Economy Barbell

The defining structural milestone of the June 2 session is the synchronized, +1.00% cross-the-board advance in Materials (XLB), Energy (XLE), and Industrials (XLI). When natural resources, heavy manufacturing, and energy infrastructure all surge in tight, positive correlation, it proves a broad-based, macro-driven commitment to the old-economy value blocks. Algorithms are no longer trading these sectors as choppy, isolated mean-reversion instruments; they are actively Underwriting a fundamental Diversification script across global cyclical assets.

The Great Growth Complex Fracture

A stark technical decoupling occurred within the growth triad today. While Technology (XLK) maintained a robust 1.25% gain, Communication Services (XLC) completely collapsed, diving -1.76%, while Consumer Discretionary (XLY) slid -0.51%. This aggressive split confirms that the mega-cap growth trade is no longer operating as a monolithic, positive-correlation monolith. Multi-strategy institutional desks ran a precise pairs-trade, ruthlessly extracting liquidity from digital media, Advertising, and interactive proxies to directly fund their fresh, high-velocity cyclical long exposure.

Defensive Safety Re-sorted

The absolute data reveals a continuing reorganization of the defensive perimeter. While Utilities thrived, Health Care (XLV) plummeted -0.97% and Consumer Staples (XLP) drifted lower at -0.24%. This targeted distribution confirms that active managers are explicitly separating defensive asset classes. They are thoroughly rejecting high-Margin pharmaceutical monopolies and expensive staple retailers, preferring instead to anchor portfolio Beta exclusively in pure fixed-yield entities like regulated utilities.

The empirical data from June 2 mandates a balanced, non-index-tracking allocation architecture. The session has forcefully broken the concentrated growth paradigm, replacing it with an active, multi-sector framework. Active managers must respect the clear directional signals written on the tape: maintain core exposure to the secular anchor in Technology (XLK), aggressively weight the unified physical economy block (XLB, XLE, XLI) to capture value Alpha, and fully utilize Utilities (XLU) for portfolio ballast while maintaining an explicit funding short or underweight stance on the severely damaged Communication Services (XLC) complex.

Please wait processing your request...

Please wait processing your request...