AI's Insatiable Electricity Appetite Revives Coal and Nuclear Energy Stocks

The artificial intelligence boom is quietly rewriting America's energy playbook. As hyperscalers pour unprecedented Capital into Data Center construction, the electricity grid is straining under a Demand surge that analysts say fossil fuels and nuclear power are uniquely positioned to meet. Jim Cramer of CNBC's "Mad Money" has repeatedly flagged this intersection — pointing out that coal stocks like Peabody Energy and Core Natural Resources, long written off by ESG-focused investors, are finding a second act as baseload power suppliers for AI infrastructure. The story is no longer just about semiconductors or cloud software. It begins, literally, at the power outlet.

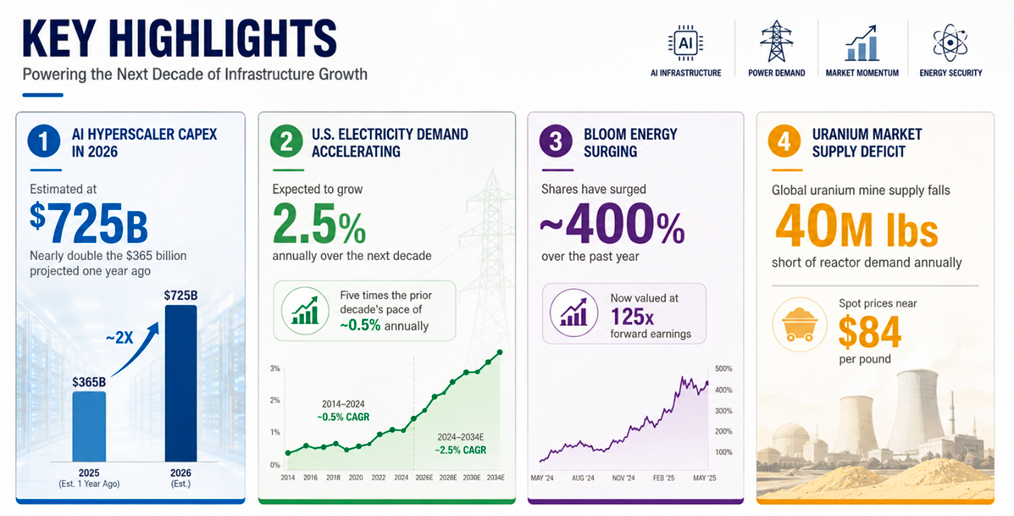

AI Hyperscaler Capex Has Nearly Doubled to $725 Billion in 2026

The numbers driving this energy narrative are staggering. According to BNP Paribas, consensus estimates for AI hyperscaler Capital Expenditure in 2026 now stand at approximately $725 billion — nearly double the $365 billion projected just one year ago in mid-2025. Capital spending is rising faster than Operating Cash Flow across the major cloud and AI players, driving significant funding needs. The magnitude of this build-out means electricity demand is no longer a secondary concern for investors — it is the primary constraint. The U.S. electricity grid, which grew at roughly 0.5% annually over the past decade, is now expected to expand at 2.5% per year over the next ten years, five times the prior growth rate, according to the Bank of America Institute. That gap between legacy infrastructure and surging demand is where the Investment opportunity lies.

Coal and Nuclear Stocks Emerge as Unlikely AI Winners

Cramer's investment thesis centers on what Nvidia CEO Jensen Huang calls the "five-layer cake" of AI Economics — a stack of industries all feeding the same build-out. At the base of that cake is power. Cramer has highlighted Vistra, GE Vernova, and Constellation Energy as utilities benefiting directly from data center electricity demand. But he has also pointed investors toward more contrarian plays: Peabody Energy and Core Natural Resources for coal exposure, and Alliance Resources for a 9.5% Dividend Yield with coal-backed cash flows. These aren't momentum trades — they are baseload power plays in a world where renewables alone cannot guarantee the 24/7 uptime that AI data centers require. The White House has separately asked PJM Interconnection, the nation's largest grid operator, to run an emergency auction allowing tech companies to bid on new power contracts, with a stated goal of building $15 billion in new baseload generation.

Bloom Energy's 400% Rally Signals Fuel Cell Moment

Perhaps the most dramatic illustration of AI's energy hunger is Bloom Energy, which has surged roughly 400% over the past year. The company, which went public at $15 per share in 2018 and traded near that level as recently as April 2025, now carries a valuation of 125 times forward Earnings. Bloom deploys solid oxide fuel cells as on-site, always-on alternatives to strained public Utility grids. It currently has 1.5 gigawatts of fuel cells deployed globally, with over 400 megawatts serving data centers. Its flagship customer Equinix alone has more than 100 megawatts deployed across 20 sites. Bloom is scaling its lone Manufacturing Facility in Fremont, California, from 1 gigawatt of annual capacity to 2 gigawatts by December 2026. A recently approved 1.8 GW Wyoming data center project, which includes 900 MW of Bloom fuel cells, is expected to generate approximately $3 billion in Revenue over coming years, per a Morgan Stanley analysis.

Uranium Gap of 40 Million Pounds Annually Signals Nuclear Squeeze

The nuclear angle adds another layer of urgency. Microsoft, Amazon, Google, and Oracle have collectively contracted roughly 6.4 gigawatts of nuclear power through announced deals as of May 2026 — the equivalent of six full-scale reactors, all earmarked for AI workloads. Yet the U.S. has not broken ground on a new full-scale reactor in over a decade. The uranium Supply picture is equally tight: global reactor demand for U3O8 in 2026 is approximately 195 million pounds, while mine supply is only around 155 million pounds — leaving a structural gap of 40 million pounds per year. Kazatomprom, which controls roughly 43% of global primary uranium production, has missed its output guidance for four consecutive years. Uranium spot prices have responded, rising from under $30 per pound in the 2010s to approximately $84 today. Bank of America analysts see prices potentially exceeding $130 before the end of next year.

Please wait processing your request...

Please wait processing your request...