Key Highlights

- Nvidia unveiled RTX Spark at Computex 2026, a superchip merging CPU and GPU for personal computers

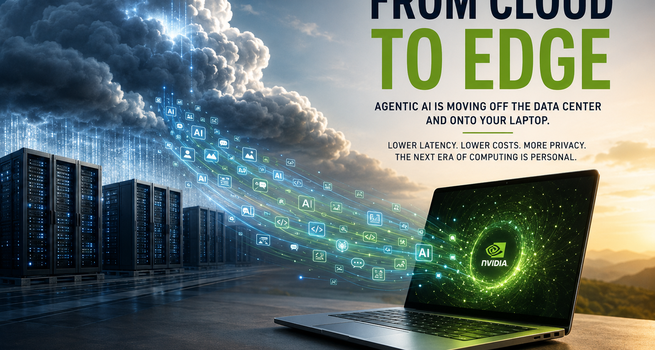

- Agentic AI workloads are structurally outgrowing cloud infrastructure, accelerating Demand for edge compute

- Intel faces its third major platform disruption in fifteen years, with no clear defensive response in personal computing

- Software compatibility and developer adoption remain the critical variables determining first-generation commercial success

- The launch signals a broader reallocation of AI infrastructure Investment from hyperscale data centres toward edge devices

A Quiet Announcement With Loud Implications

The most consequential technology shifts rarely announce themselves with fanfare. When Apple (Nasdaq:AAPL) replaced Intel processors with its own Silicon in 2020, the press release was unremarkable. The structural consequences were not. Nvidia's (NASDAQ:NVDA) unveiling of the RTX Spark chip at Computex on June 1st deserves the same sober reading. On the surface, it is a new PC processor. Beneath that, it is a direct challenge to the architecture of how AI gets delivered, who profits from it, and which hardware companies survive the next decade.

Nvidia's data-centre Revenue has grown from $11 billion to $194 billion in four years, pushing its Market Capitalisation past $5 trillion. That growth has been well understood and well priced. What the market is still calibrating is what happens when Nvidia stops being only a supplier to the cloud and becomes a competitor for the device in front of you.

The Real Driver: Agentic AI and Its Compute Appetite

The product exists because of a shift in how AI is being used, not merely how it is being built.

The dominant AI model of the past three years has been conversational: a user submits a prompt, a cloud server processes it, a response returns. The compute per interaction is bounded, the latency is tolerable, and the cloud delivery model is economically sound. Agentic AI breaks each of those assumptions.

An AI agent does not respond to a single prompt. It receives an objective, decomposes it into tasks, executes each step autonomously, evaluates the results, and iterates. Booking travel, managing a project, conducting research, and drafting communications are not discrete queries. They are continuous, multi-step workflows that generate token volumes orders of magnitude larger than a chatbot exchange.

Cloud infrastructure is already under measurable strain. Hyperscalers are spending aggressively to expand capacity, yet model developers report growing queues and latency constraints at peak demand. The economic case for processing a meaningful share of agentic workloads locally, on the device, rather than routing everything through a data centre thousands of miles away, is becoming difficult to ignore. Lower latency, reduced cloud costs, and data privacy that does not depend on contractual assurances rather than physical architecture all push in the same direction.

RTX Spark is Nvidia's answer to that demand.

What the Hardware Actually Delivers

The RTX Spark combines a 20-core ARM-based CPU with an RTX GPU containing 6,144 CUDA cores, supported by up to 128 gigabytes of unified memory. The chip delivers one petaFLOP of AI performance, enough to run large language models of up to 120 billion parameters entirely on-device.

The unified memory architecture is the detail that matters most strategically. Conventional PC designs maintain separate memory pools for the CPU and GPU, which creates data transfer overhead that is largely invisible in traditional computing tasks but becomes a meaningful bottleneck in AI workloads. Unified memory eliminates that constraint, allowing the full memory capacity to serve whichever processor needs it. The result is an architecture that behaves less like a PC with AI features bolted on and more like an AI system that also runs a PC.

Built on TSMC's (NYSE:TSM) 3-nanometre process, the chip is designed to power more than 30 laptop configurations and approximately 10 desktop systems. HP, Lenovo, Acer, Dell (NYSE:DELL), and Asus have committed to integrating it into devices due later this year.

Intel's Third Disruption and Its Shrinking Options

Intel's (NASDAQ:INTC) competitive position requires more than a passing mention. The company dominated PC processors for four decades, supported by Manufacturing scale, software ecosystems built around x86 architecture, and relationships with every major device manufacturer. That dominance has eroded across three distinct waves.

The first was mobile. Intel failed to secure meaningful share in smartphone chips, a market that ARM-based designs captured almost entirely. The second was Apple Silicon. When Apple transitioned its Mac lineup to proprietary ARM-based processors in 2020, it demonstrated that x86 was not structurally necessary for premium personal computing. Apple now holds approximately 15 percent of the global PC market, and its M-series processors set the performance-per-watt benchmark for consumer laptops.

Nvidia represents the third disruption, and in some respects the most direct. Unlike Apple, which operates within a closed hardware and software ecosystem, Nvidia is targeting the Windows PC market in Partnership with Microsoft (NASDAQ:MSFT). Intel and AMD (NASDAQ:AMD) together Supply over 80 percent of PC processors by Volume, but that figure reflects installed base and existing supply chain inertia rather than a durable competitive moat against a well-capitalised entrant with a purpose-built AI architecture and $200 billion in projected annual free cashflow.

Intel's response, outlined at Computex by CEO Lip-Bu Tan, centres on a new AI-oriented data-centre chip. Whether that addresses the competitive pressure in personal computing is a separate question, and the answer so far is not obvious.

Where the Thesis Can Break Down

Analytical credibility requires engaging seriously with the risks.

Nvidia is entering a CPU market without an established commercial track record at scale. Hardware capability is necessary but not sufficient. The Windows PC ecosystem is built on decades of software optimised for x86 architecture. Migrating enterprise applications, developer toolchains, and system integrations to an ARM and CUDA-native environment requires time, investment, and ecosystem coordination that no single launch event can guarantee.

Microsoft's deep involvement reduces this risk materially. The company has spent over two years co-developing software compatibility for the platform, and its incentives to make Windows on ARM succeed are well established following earlier failed attempts. But first-generation architectures routinely carry compatibility friction that suppresses adoption among enterprise buyers, who represent the highest-value segment of the PC market and whose purchasing cycles are measured in years, not quarters.

Consumer adoption introduces a separate variable. Agentic AI is not yet a mainstream workflow. The value proposition of an AI-native PC depends on agents becoming genuinely embedded in daily professional and personal computing within a timeframe that aligns with the product launch. If that adoption curve is slower than Nvidia's narrative implies, near-term unit volumes may disappoint relative to current expectations.

A Capital Allocation Signal Worth Reading

The most structurally significant aspect of this launch may not be the product itself but what it implies about the direction of AI infrastructure investment.

For the past three years, capital has flowed overwhelmingly toward hyperscale data centres. Microsoft, Amazon (NASDAQ:AMZN), Google (NASDAQ:GOOGL), and Meta (NASDAQ:META) have committed hundreds of billions of dollars to centralised compute infrastructure, operating on the assumption that AI delivery would remain cloud-centric. That assumption is now being tested.

As agentic AI scales, the Economics of routing every workload through a centralised data centre face structural pressure. Latency, cost, privacy, and capacity constraints all create incentives for distributing compute closer to the point of use. RTX Spark is an early but credible signal that Nvidia, which has more visibility into AI infrastructure demand than almost any other company, believes that distribution is coming.

Investors tracking AI infrastructure spending, semiconductor capital allocation, and platform ecosystem risk should treat this not as a consumer electronics story but as an early indicator of where the next phase of AI buildout is heading.

Conclusion

The PC market has been structurally stagnant for a decade. Nvidia is not launching RTX Spark because it believes the PC market will recover on its prior terms. It is launching because it believes the PC market is about to be redefined by a different set of requirements, driven by AI agents that need local compute, low latency, and memory architectures that existing designs cannot efficiently provide.

Whether Nvidia executes successfully against competitors with entrenched software ecosystems and manufacturing relationships remains to be demonstrated. What is no longer speculative is that the competitive dynamics of personal computing have materially shifted. The data-centre boom created Nvidia's current valuation. The Edge Computing cycle, if it develops as the RTX Spark launch implies, may define what comes next.

Please wait processing your request...

Please wait processing your request...