An equity research deep-dive on Oracle Corporation (NYSE:ORCL), anchored on the April 25, 2026 close. The legacy database giant has spent 2026 doing the most improbable thing in enterprise software — turning into an AI-cloud growth story.

Key Highlights

- Oracle’s valuation reflects a structural shift toward AI-driven cloud infrastructure growth.

- OCI revenue and RPO backlog have become central to earnings visibility and market pricing.

- Elevated capital expenditure and free cash flow volatility introduce new financial risk dynamics.

Oracle Corporation (NYSE:ORCL) is one of the most storied enterprise software companies in history, with a portfolio that spans the Oracle Database (still one of the most mission-critical pieces of software in global enterprise computing), a sprawling applications business including Fusion ERP, NetSuite, Cerner-derived health-system software, and an Oracle Cloud Infrastructure (OCI) franchise that has become one of the most strategically important AI training and inference platforms in the public cloud market.

By 2026, the equity story has been fundamentally re-shaped. The narrative has moved from 'mature on-premises database vendor' to 'AI infrastructure provider with a database moat.' The reasons are concrete: large strategic AI training contracts, a build-out of GPU-dense data centers, multi-cloud relationships with the other hyperscalers, and a Stargate-type narrative around purpose-built AI capacity that has captured imagination among investors and customers alike.

Stock Performance in 2026 (YTD)

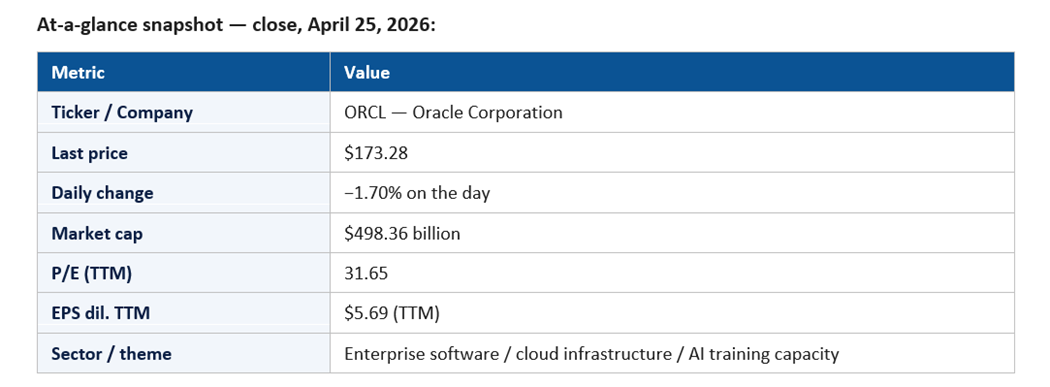

ORCL closed April 25, 2026 at $173.28, down 1.70% on the day, with a market capitalization of $498.36 billion. The trailing P/E of 31.65 on $5.69 of TTM diluted EPS reflects a company that has been re-rated by the market into the cloud-AI cohort while still generating substantial profit from the legacy database and applications businesses.

The implied YTD posture has been one of pronounced narrative volatility — Oracle has both rallied sharply on AI-infrastructure disclosures and pulled back on quarterly prints that did not fully meet the bar of expectations the new narrative demands. The −1.70% session sits inside that broader pattern of two-sided trading around a stock the market is still actively repricing.

Key Price Movements and Milestones

Three milestones define the 2026 tape. First, the move into and beyond the $150 zone, which marked the structural break from the legacy multi-decade trading range. Second, the persistent investor focus on remaining performance obligations (RPO) — the disclosed backlog of contracted but unbilled revenue — which has become the most-watched line item in each earnings cycle.

Third, the disclosure cadence around large strategic AI contracts has produced the most dramatic single-day moves of the year. Each major customer announcement, each capacity ramp disclosure, and each Stargate-type narrative event has been a discrete catalyst with sometimes outsized implications for the stock.

Major Catalysts: Why the Stock Moved

The dominant 2026 catalyst is OCI growth driven by AI training and inference workloads. Each quarter that OCI prints accelerating revenue with clear AI attribution validates the cloud-AI narrative. The challenge is that the demand has at times outpaced the capacity ramp, creating quarter-to-quarter timing mismatches that produce both upside and downside surprises.

The second catalyst is RPO disclosure. Oracle's commitment-backlog has reached levels that would have been unthinkable for the company a few years ago, and each step-change in RPO has been an immediate stock-mover. Investors increasingly model RPO conversion timing as the central variable in forward revenue.

The third catalyst is the multi-cloud strategy. Oracle's collaborations with Microsoft Azure, Google Cloud, and others — running Oracle Database inside other hyperscaler environments — have been a structurally important narrative shift. It re-positions Oracle from cloud competitor to cloud partner across a broader set of customer architectures.

The fourth catalyst is applications. Fusion ERP, NetSuite, and the broader applications portfolio continue to grow at a healthy pace and provide a profitable, recurring base of revenue underneath the more volatile OCI story.

Macro and Fed-rate sensitivity is moderate; geopolitics matter primarily through data-sovereignty and cloud-region build-out dynamics.

Sector Trends Influencing the Stock

Three sector trends underwrite Oracle's 2026 thesis. First, AI training and inference capacity remains a binding constraint on AI development globally. Any operator with the ability to bring meaningful, GPU-dense capacity online quickly is strategically advantaged, and Oracle has emerged as one of those operators.

Second, multi-cloud architectures are increasingly the default for large enterprise customers. Workload portability, data-sovereignty considerations, and procurement strategy have all pushed enterprises toward multi-vendor cloud setups, and Oracle's database-portable approach maps directly to that demand.

Third, enterprise applications continue their long migration to cloud delivery. Fusion ERP and NetSuite have benefited from this secular shift, with each cohort of cloud migrations adding to the recurring-revenue base.

Competitive Positioning

Oracle's competitive position in 2026 is best described as differentiated within a four-player cloud-infrastructure market (AWS, Azure, GCP, OCI). OCI's strategic edge is twofold: first, the integrated database-and-cloud architecture that makes running Oracle Database in OCI a uniquely cost-effective option for enterprise customers; second, the willingness to partner aggressively with other hyperscalers rather than treat them as zero-sum competitors.

In AI infrastructure specifically, Oracle has differentiated through purpose-built GPU clusters, network architecture optimized for AI workloads, and specific customer relationships that have defined the cloud-AI narrative of the past 18 months. The company is unlikely to displace AWS or Azure in scale, but it does not need to in order to deliver the equity story the market has come to expect.

In applications, Oracle competes with SAP in ERP, with Workday in HCM, and with various pure-play vendors in CRM and other categories. The competitive picture is mature but stable, with Oracle holding meaningful share in core enterprise back-office functions.

Financial Highlights

TTM diluted EPS of $5.57 on a $173.28 share price gives Oracle a P/E of 31.11. Revenue mix has continued to shift toward cloud — both OCI and cloud applications — with the implied gross margin trajectory constructive as the cloud businesses scale.

Capex has expanded substantially to support OCI capacity buildout, and that capex profile has been one of the principal points of investor debate. The bull case is that capex is being deployed against contracted demand at attractive returns; the bear case is that capex is running ahead of cash-collected revenue and could pressure free cash flow in the near term.

Capital return through buybacks and a steady dividend continues to be part of the equity story, though it has been somewhat de-emphasized as the company has pivoted capital toward cloud capacity investment.

Key Risks and Challenges

The first risk is execution on capacity. The OCI buildout requires consistent delivery of data-center capacity, GPU supply, network architecture, and operations at scale. Any meaningful slip would compress the multiple sharply.

The second risk is concentration. A meaningful share of the cloud-AI narrative has been driven by a small number of very large strategic contracts, and any disruption — commercial or relationship-based — to those contracts would be a material narrative event.

The third risk is competitive intensity. AWS, Azure, and GCP are formidable competitors with deeper scale and broader product portfolios, and any acceleration in their AI-infrastructure offerings could compress Oracle's relative growth.

The fourth risk is capital intensity. The shift in capex profile makes free cash flow more volatile and more dependent on customer collections timing, which introduces a level of financial-statement variability that the legacy Oracle did not have.

Institutional and Investor Sentiment

Institutional positioning in Oracle has shifted meaningfully constructive over the past 18 months. The combination of the AI-infrastructure narrative, the RPO trajectory, and the multi-cloud strategy has brought new institutional buyers into the name. Sell-side coverage has been increasingly bullish, with the bear case primarily focused on capex/free-cash-flow tension and on competitive risk.

The options market reflects elevated implied volatility relative to historical Oracle norms, consistent with a stock that has been re-rated into a more dynamic cohort and that still has more re-rating in front of it depending on execution.

Signals to Watch in the Coming Quarters

Six concrete signals will define how the Oracle narrative evolves through the rest of 2026. The first is OCI revenue growth and any disclosed AI-attribution. Each quarter the market wants visible evidence that the AI training and inference workload pipeline is converting into recognized revenue, with commentary on capacity utilization and customer concentration.

The second signal is RPO. Total remaining performance obligations, the cloud-only sub-metric, and the implied conversion timing collectively determine the trajectory of forward revenue. RPO has been the central narrative variable; any meaningful step-change in either direction is an immediate stock-mover.

The third signal is capacity ramp. Each disclosed data-center activation, each major GPU procurement update, and each network architecture milestone determines whether Oracle is bringing capacity online fast enough to convert demand into revenue. Capacity has been the binding constraint; the market is calibrating the unblock.

The fourth signal is multi-cloud progress. Disclosed Azure, GCP, and other hyperscaler partnerships — including customer adoption, region expansion, and revenue contribution — are increasingly important. The strategy positions Oracle as a partner rather than a competitor across most enterprise architectures, and each milestone reinforces that positioning.

The fifth signal is applications. Fusion ERP and NetSuite revenue growth, customer adds, and the mix shift between cloud and license/support determine the steady-state recurring revenue base. Applications has been the underwriter of investor patience while OCI scales.

The sixth signal is free cash flow. The capex profile has stretched FCF in some quarters; the market wants to see a path to FCF re-acceleration as customer collections catch up to capacity build. Any commentary on the timing and shape of that re-acceleration will move the multiple.

Outlook for the Rest of 2026

The base case is continuation: OCI prints accelerating revenue; RPO continues to expand; applications grows steadily; capex remains elevated but defensible; cloud margin trajectory continues to improve over time. In that scenario, the market grows more comfortable with the new financial profile and the multiple holds.

The bull case is a step-change in OCI revenue conversion of the RPO backlog — particularly if AI training capacity scales as planned and customer commitments translate into recognized revenue faster than the consensus model assumes. The bear case is a capex-versus-cash-flow disconnect that pressures free cash flow combined with execution issues on capacity ramp.

Oracle in 2026 has staged the most surprising re-rating in megacap software: a 47-year-old database company that the market now treats as a credible AI-cloud growth story. Whether the re-rating sustains depends on the next four quarters of execution.

For now, the −1.70% session is the kind of routine pullback that has framed the year — modest moves around an underlying narrative that the market is still actively pricing. Oracle remains one of the most-watched names in enterprise software, and that attention is likely to persist as long as the AI-infrastructure story continues to deliver.

Please wait processing your request...

Please wait processing your request...