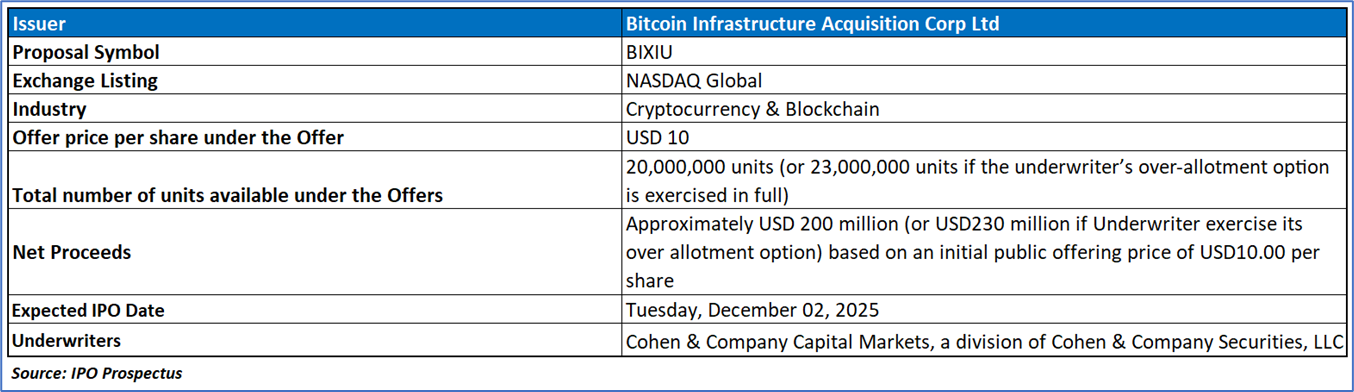

The Offer

Company Overview

Bitcoin Infrastructure Acquisition Corp Ltd (BIXIU) is a Cayman Islands–incorporated blank-check company, formed in June 2025 and renamed in August 2025, with no operational activities of its own and established for the purpose of pursuing a merger or similar business combination. While sector-agnostic in principle, the Company intends to focus on digital-asset-aligned industries, including blockchain infrastructure, Web3 technologies, financial services infrastructure, decentralized finance, custody and wallet solutions, exchanges, tokenized financial instruments, and blockchain-enabled payment and cross-border systems—leveraging the management team’s deep investment experience across crypto and technology ecosystems. The Sponsor, Samara Acquisition Sponsor V Ltd., wholly controlled by Vikas Mittal, is affiliated with Meteora, an investment adviser with extensive SPAC expertise and broad sector reach, providing strategic support, networks, SPAC lifecycle experience, and access to a substantial pipeline of private companies.

Key Highlights

Primary Offering:

20,000,000 units (or 23,000,000 units if the underwriter’s over-allotment option is exercised in full)

Use of proceeds:

- Allocation of Gross Proceeds: Bitcoin Infrastructure Acquisition Corp Ltd (BIXIU) expects to raise USD 207 million (or USD 238.05 million if the over-allotment option is exercised) from the IPO and private unit sales, with USD 200–230 million placed into a U.S.-based trust account as required under Nasdaq rules. The trust will invest exclusively in short-term U.S. Treasuries or qualifying money-market funds and will remain locked until a business combination is completed, the Company liquidates after 24 months, or shareholders approve amendments affecting redemption rights. Net proceeds outside the trust—USD 2.22 million to USD 2.67 million—will be retained for operating needs during the search and negotiation process.

- Use of Funds Outside the Trust: The capital retained outside the trust is earmarked for essential administrative and transactional expenses, including legal and accounting costs related to regulatory filings (USD 150,000), due-diligence and business-combination work (USD 400,000), administrative services and office space fees under a USD 20,000-per-month agreement with the Sponsor (USD 480,000), D&O insurance (USD 250,000), Nasdaq and regulatory fees (USD 85,000), and general working-capital purposes (USD 858,000–1.308 million). The Company may also obtain loans from the Sponsor or affiliates to cover additional transaction costs, with up to USD 1.5 million convertible into private units if a merger closes.

- Trust Mechanics, Redemption Rights, and Business Combination Funding: Funds in the trust may be used as consideration for an eventual business combination, with any unused amounts available for general corporate needs of the acquired entity, including expansion, debt servicing, or further acquisitions. Public shareholders may redeem their shares for trust proceeds upon a merger vote, failure to complete a deal within 24 months, or certain charter amendments. Sponsor-affiliated shareholders will waive redemption and liquidation rights on founder and private shares, ensuring that trust assets primarily protect public investors. However, excessive redemptions could jeopardize the ability to meet minimum cash or net-tangible-asset requirements for closing a business combination, potentially requiring alternative financing or pursuit of an alternate target.

Dividend policy:

The Company has never paid cash dividends and does not intend to do so before completing its initial business combination, with any future dividend decisions dependent on post-combination earnings, liquidity needs, and overall financial condition, and ultimately subject to the discretion of the board of directors. The board does not currently anticipate issuing share dividends, except in the event of an offering-size increase under Rule 462(b), which would require a pre-closing share dividend to ensure the Sponsor maintains at least a 25% ownership position—an action that would materially dilute other shareholders. Moreover, the Company notes that any debt incurred in connection with a future business combination may impose covenants that further restrict its ability to declare dividends thereafter.

Proposed Business Strategy for BIXIU: A Comprehensive Overview

- Strategic Mandate and Focus: Bitcoin Infrastructure Acquisition Corp Ltd. (“BIXIU”) is a newly formed Cayman Islands exempted SPAC established to pursue a merger, share exchange, asset acquisition, or similar business combination with a target operating in the rapidly evolving digital asset ecosystem. While sector-agnostic in principle, the Company intends to prioritize opportunities in financial infrastructure, Web3 technologies, and blockchain-driven business models, leveraging the extensive digital-asset, technology, and DeFi expertise of its management and board. With decades of investing and operational experience across crypto infrastructure—including wallets, custody, exchanges, lending protocols, tokenized assets, and blockchain-enabled payments—the Company aims to identify high-quality businesses positioned at the forefront of global financial digitization.

- Role of Meteora and Sponsor Affiliation: The Company’s Sponsor is an affiliate of Meteora Capital, a SPAC-focused investment adviser led by Vikas Mittal, who also serves as a Company director. Meteora will provide non-compensated advisory support, drawing on its full lifecycle SPAC experience, capital markets expertise, and broad network across crypto, technology, fintech, and other emerging sectors. Meteora’s integrated SPAC platform—including risk capital, secondary investments, and private-market relationships—creates a strong sourcing advantage. Its affiliated funds have expressed interest in acquiring up to 19.99% of offering units, potentially enabling approval of a business combination even without majority support from unaffiliated public shareholders, thereby influencing both liquidity dynamics and voting outcomes.

- Market Opportunity and Differentiated Execution Framework: BIXIU intends to capitalize on major structural trends reshaping global finance, including bitcoin’s emergence as a collateral asset, the exponential growth of USD stablecoins following U.S. regulatory clarity, and the accelerating institutional shift toward tokenized real-world assets (RWAs). These trends underpin multi-trillion-dollar market expansions, presenting significant opportunities for infrastructure providers in custody, liquidity, payments, and tokenization. The Company’s strategy is to target mission-driven, globally scalable businesses with strong regulatory alignment, particularly those enabling real-world utility across payments, DeFi, cross-border finance, and digital capital markets. Backed by a management team with deep domain expertise, global relationships, and experience navigating complex regulatory environments, BIXIU aims to execute a value-accretive business combination and serve as a long-term strategic partner to a leading digital financial infrastructure company.

Financial Highlights (Results of Operations) (Expressed in USD)

- Financial Position Prior to the Offering: Bitcoin Infrastructure Acquisition Corp Ltd. (“BIXIU”) has not commenced operations and has generated no revenues to date, with activities strictly limited to organizational setup and IPO preparation. The Company anticipates no operating revenues until the completion of its initial business combination, though it expects to earn interest income on trust account balances. No material adverse financial developments have occurred since its audited statements; however, public-company compliance, regulatory reporting, and due-diligence costs are expected to rise substantially following the offering.

- Liquidity Framework and Trust Account Structure: BIXIU’s liquidity prior to the IPO has been supported by USD 25,000 in Sponsor-funded formation costs and a USD 300,000 Sponsor loan. Following the offering, the Company expects net proceeds of approximately USD 202.2 million (or USD 232.7 million with full over-allotment), of which USD 200 million (or USD 230 million) will be deposited into a trust account invested in U.S. Treasury instruments or qualifying money-market funds. Only about USD 2.22 million (or USD 2.67 million with over-allotment) will remain outside the trust for operating activities during the 24-month search period. These funds are earmarked for legal and accounting expenses, SEC reporting obligations, administrative services, directors’ and officers’ insurance, and general working capital requirements.

- Ongoing Capital Needs and Financial Risks: Management believes the non-trust funds will be sufficient to support operations for up to 24 months; however, actual expenses may differ materially from estimates, especially if extensive due diligence, complex negotiations, or target-specific regulatory reviews are required. As of July 18, 2025, the Company held USD 25,000 in cash with a working-capital deficit of USD 15,153, relying on Sponsor commitments to meet obligations prior to the IPO. Future additional financing may be required if operating costs exceed projections, if substantial shareholder redemptions reduce available cash at the business combination, or if post-combination working capital needs exceed trust proceeds not used for consideration.

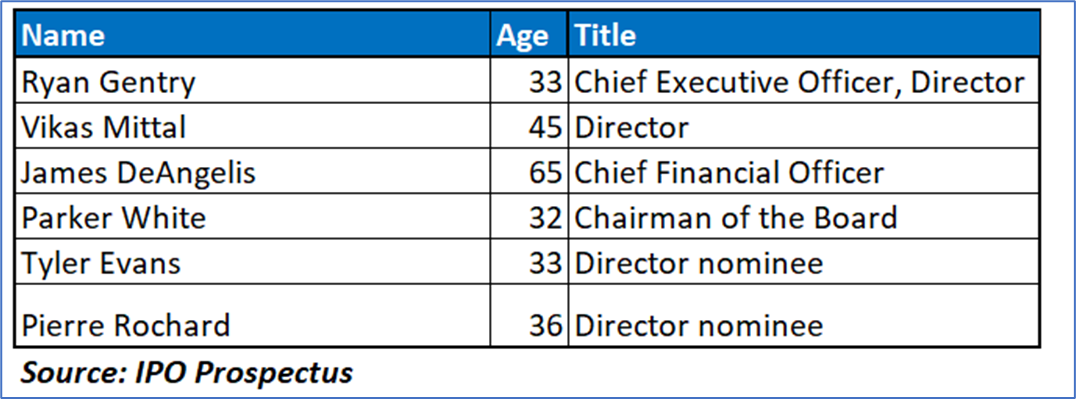

Key Management Highlights

Risk Associated (High)

Investment in the IPO of “BIXIU” is exposed to a variety of risks such as:

- Dependence on Successful Completion of a Business Combination: BIXIU has no operating business and will not generate revenue until a merger is completed, making its entire value proposition contingent on identifying, negotiating, and closing a suitable digital-asset–focused target within the 24-month deadline. Failure to consummate a transaction would require liquidation, resulting in investors receiving only trust proceeds and losing any potential upside while the Company incurs unrecoverable operating expenses.

- High Concentration of Control by Sponsor and Affiliates: The Sponsor—controlled solely by Vikas Mittal—and its affiliated funds (including Meteora) may purchase up to 19.99% of the public units and have agreed to vote all such securities in favor of any proposed business combination. This concentrated voting power may enable approval of a transaction even without broad public shareholder support, creating misalignment of interests and elevating governance and conflict-of-interest risks.

- Limited Operating Capital Outside the Trust and Reliance on Sponsor Financing: BIXIU will have only approximately USD 2.22 million (or USD 2.67 million with over-allotment) available outside the trust account to fund its 24-month operating period. Given significant expected legal, diligence, regulatory, and administrative costs, the Company may require additional Sponsor loans or third-party financing to complete a deal. Any shortfall could impair due diligence quality, reduce negotiating leverage, or jeopardize timely completion of a business combination.

Conclusion

Bitcoin Infrastructure Acquisition Corp Ltd (BIXIU) is a Cayman Islands–incorporated SPAC formed in 2025 with no operating activities, established to identify and merge with a target in blockchain infrastructure, Web3 technologies, financial services infrastructure, DeFi, custody and wallet solutions, exchanges, tokenized assets, and blockchain-enabled payment systems. The IPO structure involves issuing 20–23 million units, with USD 200–230 million of gross proceeds placed into a U.S. trust account invested in short-term Treasuries, while approximately USD 2.22–2.67 million remains available for legal, regulatory, diligence, administrative, and insurance expenses during the 24-month search period. The Sponsor, controlled by Vikas Mittal and affiliated with Meteora, provides sector networks and SPAC-execution experience and may acquire up to 19.99% of the units, which could affect voting outcomes on a future business combination. The Company’s strategy centers on targets aligned with structural trends in digital-asset infrastructure, including custody, tokenization, payments, cross-border finance, and Web3 services, while its financial position prior to the offering reflects no revenues, limited liquidity, reliance on Sponsor funding for formation costs, and the expectation of earning only interest income until a merger is completed.

Hence, given the financial performance of the company, use of proceeds, and associated risks “Bitcoin Infrastructure Acquisition Corp Ltd (BIXIU)” IPO seems “Neutral" at the IPO price.

Past performance is not a reliable indicator of future performance.

Please wait processing your request...

Please wait processing your request...