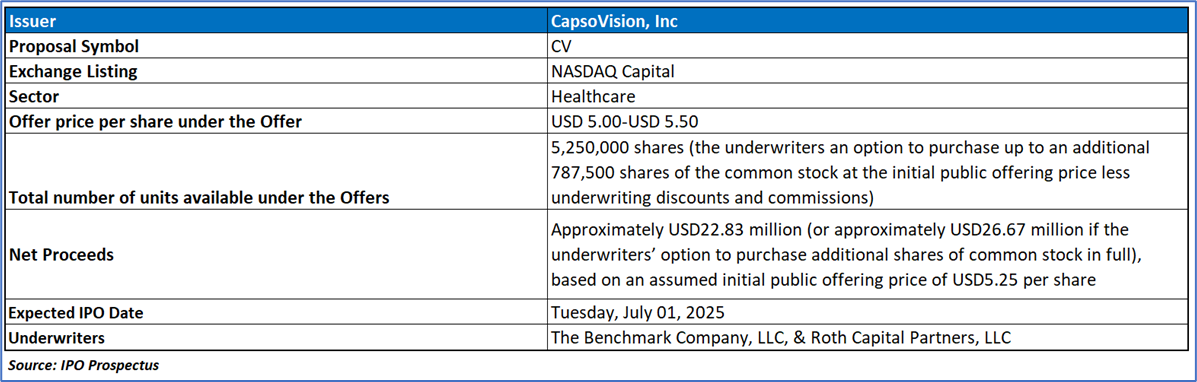

The Offer

Company Overview

CapsoVision Inc (CV), a commercial-stage medical technology company, specializes in advanced imaging and AI-driven capsule endoscopy solutions to diagnose gastrointestinal (GI) tract abnormalities, offering the CapsoCam Plus, a wire-free, FDA-cleared Class II device that panoramically visualizes the small bowel to detect conditions like obscure GI bleeding and Crohn’s disease, with images stored onboard and reviewed via CapsoCloud or CapsoView software for streamlined clinician workflows. The company is enhancing its CapsoCam Plus with self-developed AI-assisted reading tools to improve diagnostic efficiency and is developing the CapsoCam Colon, incorporating AI polyp detection and 3D sizing for colorectal screening, with FDA 510(k) submissions underway and a second-generation launch planned for 2026. CapsoVision is also exploring new GI indications, such as esophageal varices and pancreatic cancer detection, with feasibility studies targeted for 2025 and 2026, respectively, while expanding its global sales presence in key markets like France, Germany, and Canada through direct and distributor channels.

Key Highlights

Primary Offering:

5,250,000 shares (the underwriters an option to purchase up to an additional 787,500 shares of the common stock at the initial public offering price less underwriting discounts and commissions)

Use of proceeds:

- Strategic Allocation of Offering Proceeds: CapsoVision intends to allocate the estimated net proceeds of approximately USD22.83 million from its initial public offering (or USD26.67 million if the underwriters’ option is fully exercised), based on an assumed offering price of USD5.25 per share, to advance its innovative capsule endoscopy solutions and strengthen its operational framework. Approximately USD8 million will be directed toward research and development to enhance the AI capabilities of the CapsoCam Plus, advance the CapsoCam Colon for colorectal screening, and fund clinical studies to evaluate the CapsoCam’s efficacy in screening esophageal varices in cirrhotic patients and detecting cancerous and precancerous pancreatic neoplasia, reinforcing CapsoVision’s commitment to expanding its diagnostic portfolio for gastrointestinal health.

- Financial and Operational Flexibility: The company will allocate USD1 million to repay a loan from an existing investor, dated May 28, 2025, to enhance liquidity prior to the offering’s completion, with the remaining proceeds designated for general corporate purposes, including working capital, operating expenses, and capital expenditures. Management retains broad discretion over the precise application of these funds, with expenditures contingent on factors such as operational cash flows and business growth, while any unutilized proceeds will be invested in capital-preservation vehicles like government securities and money market funds to ensure financial stability and support CapsoVision’s long-term strategic objectives.

Dividend policy:

CapsoVision, a commercial-stage medical technology company, has not historically declared or paid cash dividends or distributions on its capital stock and plans to retain all earnings to fund the growth and development of its innovative capsule endoscopy solutions, including the AI-enhanced CapsoCam Plus and the CapsoCam Colon, with no intention to pay cash dividends on its common stock in the foreseeable future. Any future dividend payments will be at the discretion of the board of directors, contingent upon factors such as the company’s financial condition, operational results, capital needs, financing agreement restrictions, applicable legal provisions, and other considerations deemed relevant by the board.

CapsoVision Market Overview and Strategic Opportunities

- Small Bowel Endoscopy and Diagnostic Advantages: CapsoVision operates in the specialized market of capsule endoscopy, focusing on non-invasive visualization of the small bowel to diagnose conditions such as obscure gastrointestinal (GI) bleeding, chronic iron-deficiency anemia, Crohn’s disease, tumors, and polyposis syndromes. Capsule endoscopy, recognized as the first-line modality for small bowel imaging, offers superior diagnostic yield (30%-70%) compared to alternatives like push enteroscopy (31%), double-balloon enteroscopy (23%), and small-bowel series (5%), due to its non-invasive nature and ability to identify lesions like ulcers, vascular anomalies, and polyps, particularly within 14 days of a bleeding episode. The CapsoCam Plus, with its panoramic imaging and wire-free design, enhances diagnostic accuracy for conditions like Crohn’s disease (91%-100% sensitivity, 91%-92% specificity) and supports ongoing surveillance for polyposis syndromes, such as Peutz-Jeghers, outperforming traditional endoscopy for polyp detection beyond the duodenum.

- Emerging Opportunities in Colon Capsule Endoscopy: CapsoVision is poised to capitalize on the growing colon capsule endoscopy market, estimated at USD213 million in 2025 and projected to reach USD311 million by 2030, with its CapsoCam Colon, which leverages advanced AI and 3D polyp sizing for colorectal cancer (CRC) screening, addressing a USD17.8 billion U.S. market expected to grow to USD21.8 billion by 2030. Despite challenges in colon capsule adoption, such as incomplete visualization due to bowel preparation or battery life issues and limited high-quality evidence for CRC screening, CapsoCam Colon’s superior polyp detection accuracy compared to CT colonography and stool-based tests (e.g., Cologuard’s 75% false-positive rate for advanced neoplasia) positions it to serve the underserved population of unscreened patients, where early detection of CRC—responsible for 153,000 new U.S. cases and 53,000 deaths annually—can significantly improve survival rates.

- Future Growth in Esophageal and Pancreatic Indications: CapsoVision is expanding its market potential through planned feasibility studies in 2025 and 2026 to evaluate the CapsoCam’s efficacy in screening esophageal varices in 5.5 million U.S. cirrhotic patients and detecting pancreatic neoplasia, addressing critical unmet needs given the low sensitivity of existing solutions like Medtronic’s PillCam (64% for varices) and the high lethality of pancreatic cancer (13% five-year survival rate, 67,000 U.S. cases in 2025). The CapsoCam’s high duodenal papilla detection rate (82% vs. 15% for PillCam in a 2024 study) and panoramic imaging capabilities offer potential improvements in diagnostic accuracy for these conditions, enhancing CapsoVision’s competitive edge in the GI diagnostics market while addressing significant clinical and economic challenges associated with invasive procedures and late-stage diagnoses.

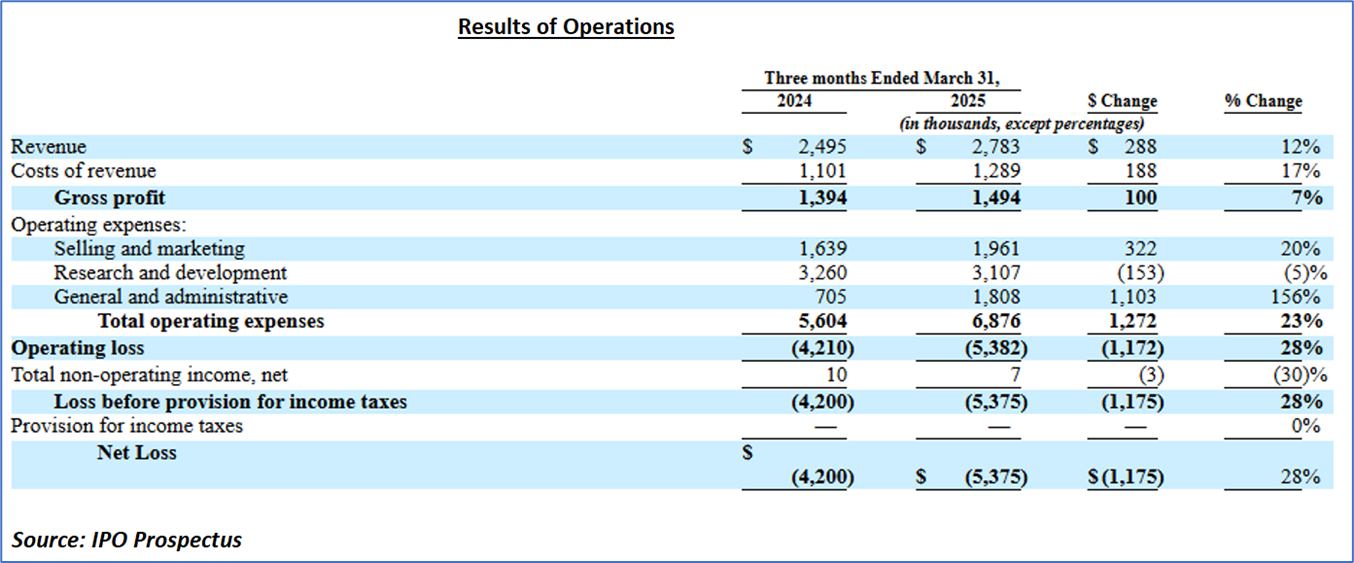

Financial Highlights (Results of Operations) (Expressed in USD)

- Revenue Growth and Cost Dynamics: CapsoVision reported a revenue increase to USD2.783 million in Q1 FY25, a 12% rise from USD2.495 million in Q1 FY24, driven by an 11% year-over-year increase in CapsoCam Plus unit sales, with 10% growth in the U.S. and 13% internationally, reflecting robust demand for its small-bowel capsule endoscopy solution. However, costs of revenue rose by 17% to USD1.289 million from USD1.101 million, outpacing revenue growth due to higher unit sales and related services, resulting in a gross profit increase of 7% to USD1.494 million but a slight gross margin decline from 56% to 54%, indicating margin pressure from scaling operations.

- Operating Expense Trends: Operating expenses surged 23% to USD6.876 million in Q1 FY25 from USD5.604 million in Q1 FY24, primarily due to a 156% increase in general and administrative expenses to USD1.808 million, driven by USD0.6 million in professional service fees, USD0.3 million in headcount and office-related costs, and USD0.1 million in stock-based compensation, alongside a 20% rise in selling and marketing expenses to USD1.961 million, half of which stemmed from U.S. sales team expansion. Research and development expenses decreased by 5% to USD3.107 million, reflecting the completion of the CapsoCam Colon pivotal study in 2024, though ongoing clinical trials for AI-assisted reading technology continued to incur costs, highlighting CapsoVision’s investment in innovation despite cost pressures.

- Liquidity and Financial Challenges: CapsoVision’s liquidity remains constrained, with USD4.4 million in cash as of March 31, 2025, and a USD1 million loan from an existing investor on May 28, 2025, to bolster liquidity pre-IPO, while net cash used in operating activities increased to USD4.986 million in Q1 FY25 from USD4.025 million in Q1 FY24, driven by a net loss of USD5.4 million and inventory buildup. The company’s accumulated deficit of USD135.7 million and ongoing operating losses, coupled with an auditors’ going concern qualification for 2024, underscore significant financial risks, necessitating the planned USD22.83 million IPO proceeds to fund R&D, repay debt, and support general corporate needs, with management retaining discretion over fund allocation to navigate growth and competitive challenges.

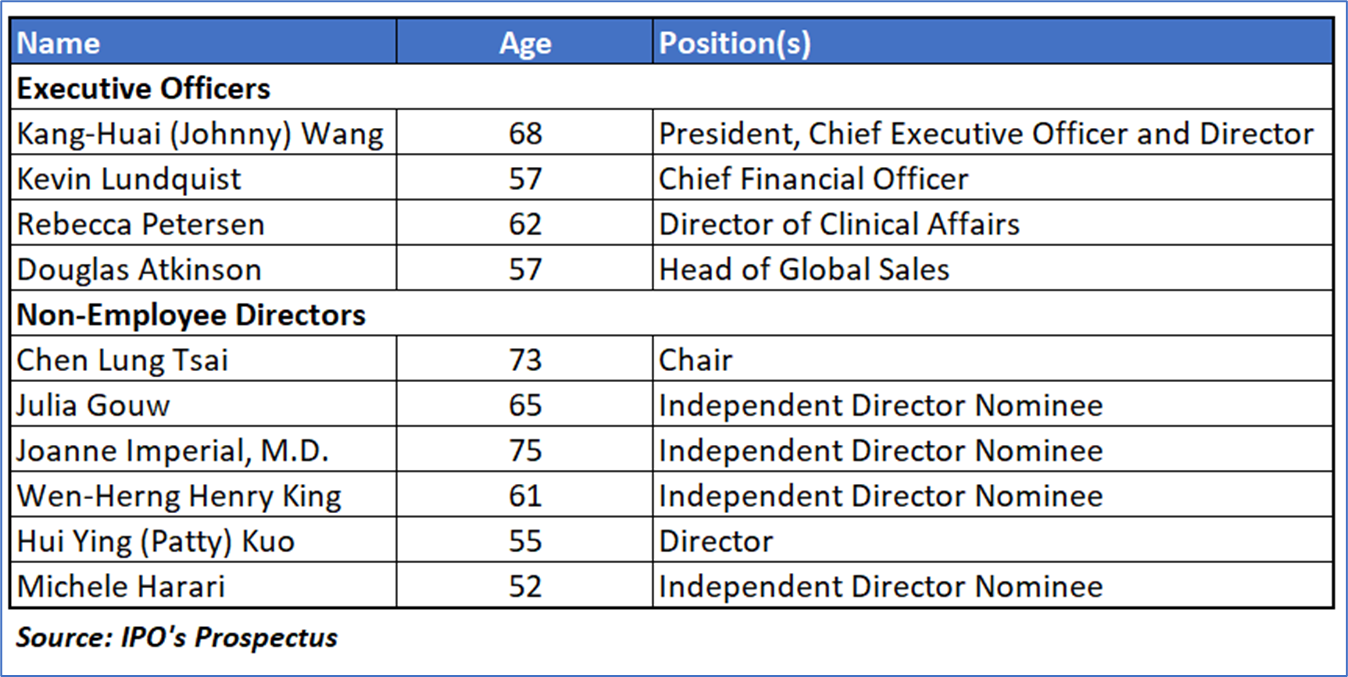

Key Management Highlights

Risk Associated (High)

Investment in the IPO of “CV” is exposed to a variety of risks such as:

- Substantial Doubt About Going Concern: CapsoVision’s audited financial statements for 2024 and Q1 FY25 highlight a substantial doubt about its ability to continue as a going concern, with an accumulated deficit of USD135.7 million and net cash used in operating activities of USD4.986 million in Q1 FY25, posing a risk of operational jeopardy if the company fails to secure sufficient funding through its planned USD22.83 million IPO or other sources to sustain its growth and R&D initiatives.

- Regulatory Approval Delays for New Products: The company’s growth strategy hinges on timely FDA 510(k) clearances for its AI-enhanced CapsoCam Plus and CapsoCam Colon, with submissions targeted for late 2025 and 2026, respectively; however, potential delays or failure to obtain these clearances could hinder commercialization timelines and revenue generation, particularly in the competitive colon capsule endoscopy market.

- Competitive Pressures in Capsule Endoscopy Market: CapsoVision faces intense competition from established players like Medtronic’s PillCam, which has a stronger market presence, and must differentiate its CapsoCam solutions through superior panoramic imaging and AI capabilities while overcoming barriers such as incomplete colon visualization and limited high-quality evidence for CRC screening, which could impede market adoption and sales growth.

Conclusion

CapsoVision, Inc., a commercial-stage medical technology company specializing in advanced imaging and AI-driven capsule endoscopy, presents a compelling yet high-risk investment opportunity through its initial public offering (IPO) of 5,250,000 shares, aiming to raise approximately USD22.83 million (or USD26.67 million if the underwriters’ option for 787,500 additional shares is exercised) at an assumed price of USD5.25 per share. The company’s innovative CapsoCam Plus, a wire-free, FDA-cleared device for small-bowel diagnostics, demonstrates strong market traction with a 12% revenue increase to USD2.783 million in Q1 FY25, driven by an 11% rise in unit sales, and its development of the CapsoCam Colon with AI polyp detection targets the growing USD213 million colon capsule endoscopy market, projected to reach USD311 million by 2030. Planned feasibility studies for esophageal varices and pancreatic neoplasia in 2025 and 2026 further enhance its growth potential in addressing unmet GI diagnostic needs. However, significant risks temper this opportunity, including a substantial doubt about its going concern status due to an accumulated deficit of USD135.7 million and ongoing losses (USD5.4 million net loss in Q1 FY25), potential delays in FDA 510(k) clearances for new products, and intense competition from established players like Medtronic’s PillCam. Given the company’s constrained liquidity (USD4.4 million in cash as of March 31, 2025) and reliance on IPO proceeds to fund R&D (USD8 million) and debt repayment (USD1 million), CapsoVision’s innovative potential and market opportunity against its financial vulnerabilities and regulatory uncertainties must be weighed.

Hence, given the financial performance of the company, use of proceeds, and associated risks “CapsoVision, Inc (CV)” IPO seems “Neutral" at the IPO price.

Past performance is not a reliable indicator of future performance.

Please wait processing your request...

Please wait processing your request...