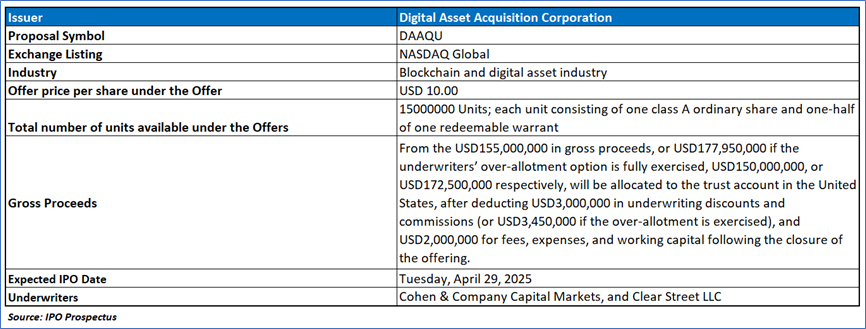

The Offer

Company Overview

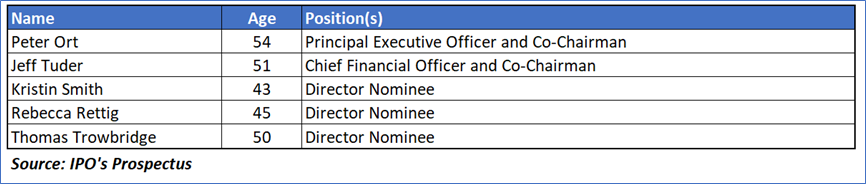

Digital Asset Acquisition Corporation (DAAQU), a special purpose acquisition company (SPAC) incorporated on December 9, 2024, as a Cayman Islands exempted company, was established to effect a merger, amalgamation, share exchange, asset acquisition, share purchase, reorganization, or similar business combination, primarily targeting opportunities in the digital asset and cryptocurrency sectors, though it may pursue combinations in any industry or region. The Company, which has not yet selected a target or initiated substantive discussions, leverages the expertise of its management team, led by Co-Chairmen Peter Ort and Jeff Tuder, who bring significant SPAC experience from their involvement with Concord Acquisition Corps I, II, and III, to identify and evaluate potential targets, focusing on innovation-driven platforms in digital assets, real estate, and related technology infrastructure, while acknowledging the inherent uncertainties and potential conflicts of interest due to the team’s concurrent engagements.

Key Highlights

Primary Offering:

DAAQU is conducting an initial public offering of 15,000,000 units, each priced at USD10.00 and comprising one Class A ordinary share and one-half of one redeemable warrant, with each whole warrant exercisable at USD11.50 per share to purchase one Class A ordinary share, becoming exercisable 30 days after the completion of an initial business combination and expiring five years thereafter, subject to potential redemption or liquidation as outlined. The offer includes a 45-day option for underwriters to purchase up to an additional 2,250,000 units to cover overallotments, with only whole warrants tradable and exercisable, ensuring no fractional warrants are issued upon unit separation.

Use of proceeds:

- Allocation of Offering Proceeds: DAAQU is launching an initial public offering of 15,000,000 units priced at USD10.00 each, with projected net proceeds, combined with funds from the sale of private placement warrants, allocated as outlined in the accompanying table. The total gross proceeds are expected to reach USD155,000,000, or USD177,950,000 if the underwriters’ over-allotment option for an additional 2,250,000 units is exercised, comprising USD150,000,000 (or USD172,500,000 with over-allotment) from public units and USD5,000,000 (or USD5,450,000 with over-allotment) from private placement warrants. After accounting for USD3,000,000 in underwriting commissions (or USD3,450,000 with over-allotment) and USD700,000 in other offering expenses—including legal, printing, trustee, accounting, SEC/FINRA, travel, Nasdaq listing, and miscellaneous costs—the remaining USD151,300,000 (or USD173,800,000 with over-allotment) will be distributed, with USD150,000,000 (or USD172,500,000) deposited into a trust account, representing 100% of the public offering size, and USD1,300,000 retained for operational use.

- Distribution of Non-Trust Proceeds: The approximately USD1,300,000 not held in the trust account will be strategically allocated to support pre-business combination activities, with USD220,000 (16.9%) designated for accounting, due diligence, travel, and related expenses, USD175,000 (13.5%) for legal and accounting fees tied to regulatory reporting, and USD75,000 (5.8%) for Nasdaq and other regulatory fees. Additionally, USD420,000 (32.3%) will reimburse administrative support over a 21-month period, USD350,000 (26.9%) will fund directors’ and officers’ liability insurance, and USD60,000 (4.6%) will cover miscellaneous costs, ensuring sufficient resources to manage initial operational needs. These funds, supplemented by potential permitted withdrawals, are considered adequate, though additional capital may be sought if costs exceed estimates, primarily through sponsor or management loans, with no expectation of third-party financing due to trust account restrictions.

- Management of Offering Expenses and Financing Support: Offering expenses, estimated at USD700,000 excluding underwriting commissions, include various professional and regulatory fees, with a portion initially funded by a non-interest-bearing loan of up to USD300,000 from the sponsor, repayable from the allocated proceeds upon closing or by December 31, 2025, whichever comes first. The underwriters have deferred USD6,000,000 in commissions (or USD6,900,000 with over-allotment), payable from the trust account post-business combination after shareholder redemptions, with any excess released for acquisition costs, debt repayment, or working capital. The sponsor may also provide non-interest loans up to USD1,500,000 for transaction costs, convertible into private placement warrants at USD1.00 each, reinforcing financial flexibility without compromising the trust’s integrity.

Dividend policy:

DAAQU has not paid cash dividends on its ordinary shares and does not plan to do so prior to completing its initial business combination, as outlined in its amended and restated memorandum and articles of association, which prohibits dividends or distributions from assets outside the trust account before such a combination unless approved by two-thirds of Class B ordinary shareholders. Post-business combination, dividend payments will be at the discretion of the board, contingent on revenues, earnings, capital needs, and overall financial condition, with potential limitations from indebtedness covenants, and the Company will maintain founder shares at 25% of issued shares through adjustments if the offering size changes under Rule 462(b).

Market Landscape and Strategic Focus for DAAQU

- Overview of Blockchain Technology and Industry Focus: DAAQU is strategically positioned to target opportunities within the expansive blockchain and digital asset sector, leveraging the innovative framework of blockchain technology, which employs an open, distributed ledger managed by a peer-to-peer network to record transactions securely across global computer networks. Notable examples include the Bitcoin blockchain, serving as a public ledger for digital asset transactions, and the Ethereum Blockchain, a distributed platform that supports decentralized applications through self-executing smart contracts powered by its native cryptocurrency, Ether, highlighting the sector’s potential for transformative applications.

- Characteristics of Digital Assets and Cryptocurrencies: The industry encompasses a variety of digital assets, such as tokens, non-fungible tokens (NFTs), and cryptocurrencies, with the latter defined as blockchain-based assets transferable between parties, categorized into store-of-value or payment cryptocurrencies like Bitcoin, which are increasingly accepted by merchants albeit with limited adoption, and more functional cryptocurrencies integral to blockchain economies, such as Ether, Solana, and TRON. Stablecoins, including U.S. Dollar Coin (USDC) and Tether, aim to maintain stable values tied to non-volatile assets, though they remain susceptible to price fluctuations due to factors like supply-demand dynamics, market confidence, and liquidity risks, particularly when linked to fluctuating fiat currencies like the U.S. dollar.

- Market Growth and Economic Significance: The blockchain and cryptocurrency market has experienced remarkable growth, with the total market capitalization rising from USD783 billion on January 1, 2021, to over USD3.4 trillion by January 1, 2025, reflecting a robust compound annual growth rate of 45%, driven by widespread adoption. Bitcoin alone commands over USD1.9 trillion, comprising more than 50% of the market, though it remains significantly below gold’s USD17.9 trillion market cap, while facilitating over 650,000 daily transactions by December 2024, underscoring the sector’s increasing economic relevance and transaction volume.

Financial Highlights (Results of Operations) (Expressed in USD)

- Current Operations and Revenue Expectations: DAAQU has not yet commenced operations or generated any revenues since its inception, with activities limited to organizational efforts and preparations for this offering, and no operating revenues are anticipated until the completion of an initial business combination. Post-offering, the Company expects to earn non-operating income through interest on cash and cash equivalents, with no significant changes in financial or trading position reported since the audited financial statements, though increased expenses are foreseen due to public company obligations, including legal, financial reporting, accounting, auditing compliance, and due diligence costs. These expenses are projected to rise substantially following the offer closure, reflecting the Company’s transition to a publicly traded entity.

- Liquidity and Financial Resources: The Company’s liquidity needs prior to this offering have been met through a USD25,000 payment from the sponsor for offering and formation costs in exchange for founder shares, alongside a USD300,000 non-interest-bearing loan from the sponsor, both to be repaid upon offering closure. Net proceeds from the offering, estimated at USD151,300,000 (or USD173,800,000 with over-allotment), including USD5,000,000 from private placement warrants, will allocate USD150,000,000 (or USD172,500,000 with over-allotment) to a trust account invested in short-term U.S. government treasury obligations or compliant money market funds, with the remaining USD1,300,000 reserved for operational expenses, adjustable based on actual offering costs.

- Capital Utilization and Future Funding Needs: The funds held outside the trust account, approximately USD1,300,000, will support expenses such as USD350,000 for legal and due diligence, USD175,000 for regulatory reporting, USD75,000 for Nasdaq fees, USD240,000 for administrative services, USD350,000 for insurance, and USD110,000 for working capital, though these are estimates subject to variation. The Company may seek additional financing from the sponsor or affiliates for working capital or transaction costs, with up to USD1,500,000 convertible into private placement warrants at USD1.00 each, and anticipates targeting businesses requiring funds beyond trust proceeds, potentially issuing equity or incurring debt to complete a business combination, with liquidation as a contingency if insufficient funds are secured.

Key Management Highlights

Risk Associated (High)

Investment in the IPO of “DAAQU” is exposed to a variety of risks such as:

- Limited Shareholder Influence on Business Combination Decisions: DAAQU’s public shareholders may face restricted influence over the initial business combination, as the Company may not hold a shareholder vote unless required by law or stock exchange rules, and even if a vote occurs, the participation of founder shareholders—who, along with management, have committed to vote in favor—could lead to approval despite majority public opposition. With initial shareholders holding 25% of shares post-offering, only 33.3% of public shares (5,000,001 shares) are needed for an ordinary resolution, or none if only a quorum votes, and for a special resolution, 55.56% (8,333,334 shares) are required if all shares are voted, potentially allowing the combination to proceed without broad public support. This structure limits public shareholders’ ability to impact the decision, with their primary recourse being the exercise of redemption rights, which may not align with their investment goals.

- Challenges Posed by Redemption Rights and Financial Constraints: The ability of public shareholders to redeem their shares for cash introduces significant risks, as excessive redemptions could render DAAQU’s financial condition unattractive to potential targets, hindering the ability to meet minimum cash requirements for a business combination and potentially leading to the failure of the transaction. Additionally, a high redemption rate, combined with the obligation to pay deferred underwriting commissions, may prevent the Company from pursuing the most desirable business combination or optimizing its capital structure, necessitating third-party financing that could involve dilutive equity issuances or burdensome debt, further diluting shareholder value and impacting the financial stability of the post-combination entity.

- Time Constraints and Due Diligence Limitations: DAAQU must complete its initial business combination within an 18-month window (extendable to 21 or 36 months under certain conditions), which may give target businesses negotiating leverage, particularly as the deadline approaches, potentially forcing the Company to accept less favorable terms. This time constraint could also limit the thoroughness of due diligence on potential targets, increasing the risk of overlooking critical issues that might undermine the value of the combination for shareholders, especially if the Company rushes to avoid liquidation, where shareholders may face delays in accessing funds or incur losses if forced to sell shares at a discount in the open market.

Conclusion

Digital Asset Acquisition Corporation (DAAQU), a Cayman Islands-based SPAC incorporated on December 9, 2024, is offering 15,000,000 units at USD10.00 each through an initial public offering, aiming to raise USD151.3 million (or USD173.8 million with over-allotment) to pursue a business combination primarily in the digital asset and cryptocurrency sectors, which has grown to a USD3.4 trillion market by January 2025, though it remains without a target, revenues, or dividends pre-combination, and allocates USD1.3 million for operational costs while relying on the SPAC experience of Co-Chairmen Peter Ort and Jeff Tuder. The investment carries high risks, including limited shareholder influence due to the 25% founder stake and voting agreements, potential financial strain from redemptions and deferred commissions that could necessitate dilutive financing, and an 18- to 36-month window that may constrain due diligence and lead to liquidation if terms become unfavorable, highlighting the uncertainties tied to its strategy and execution.

Hence, given the financial performance of the company, use of proceeds, and associated risks “Digital Asset Acquisition Corporation (DAAQU)” IPO seems “Neutral" at the IPO price.

Past performance is not a reliable indicator of future performance.

Please wait processing your request...

Please wait processing your request...