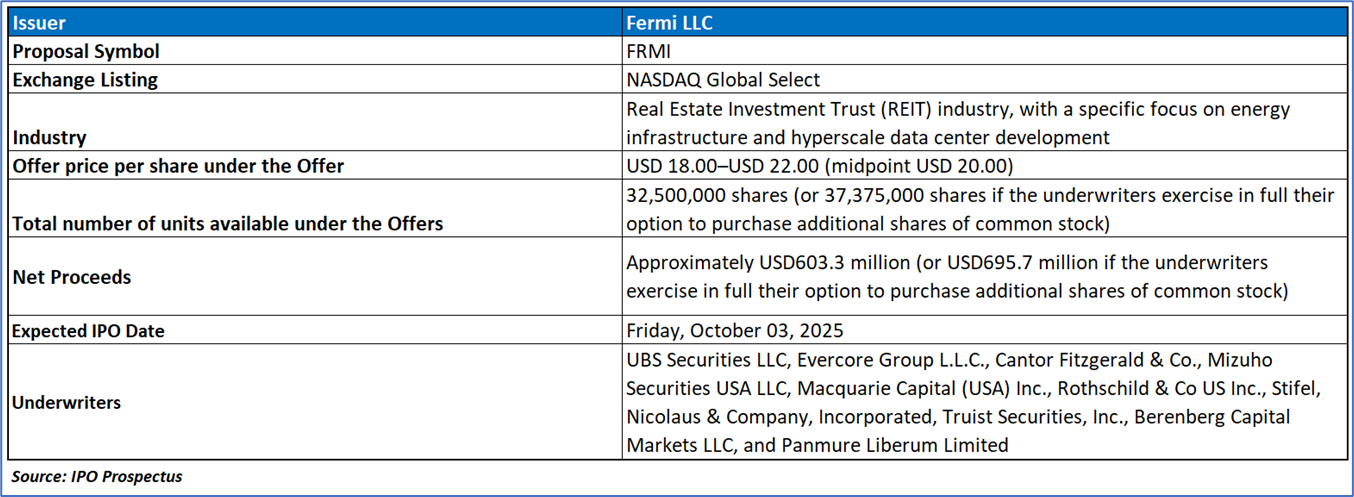

The Offer

Company Overview

Fermi LLC (FRMI), a Real Estate Investment Trust (REIT), is developing Project Matador, a 5,236-acre energy and hyperscale data center campus in Amarillo, Texas, aimed at powering the AI revolution with up to 11 gigawatts of low-carbon, HyperRedundant™ energy by 2038, integrating natural gas, nuclear, solar, and battery storage. Secured through a 99-year lease with Texas Tech University, the project targets 1.1 GW online by 2026, leveraging strategic proximity to natural gas fields, fiber networks, and the DOE’s Pantex Plant to deliver reliable, grid-independent power for AI data centers. Led by a seasoned team including former U.S. Energy Secretary Rick Perry and nuclear expert Mesut Uzman, Fermi has secured key contracts (e.g., Siemens turbines) and a nuclear Combined License Application accepted by the NRC, positioning it to capitalize on the USD457 billion generative AI market and U.S. data center demand projected to reach 1,000 TWh by 2030, though it faces risks from its development-stage status, regulatory hurdles, and reliance on third-party suppliers.

Key Highlights

Primary Offering:

32,500,000 shares (or 37,375,000 shares if the underwriters exercise in full their option to purchase additional shares of common stock)

Use of proceeds:

- Estimated Net Proceeds: Based on an assumed initial public offering price of USD 20.00 per share, the company expects to generate approximately USD 603.3 million in net proceeds from the offering, or USD 695.7 million if underwriters fully exercise their option to purchase additional shares. These figures are calculated after deducting underwriting discounts and related expenses. Variations in the offering price or the number of shares issued could materially affect net proceeds, with each USD 1.00 change in share price impacting proceeds by roughly USD 30.8 million, and each 1 million share adjustment altering proceeds by approximately USD 19.0 million.

- Planned Use of Funds: The net proceeds, together with existing cash and short-term investments, will primarily be directed towards business growth, long lead-time equipment procurement, and construction initiatives, while also supporting financial flexibility. Specifically, the company has allocated USD 325 million for procurement and installation of long lead-time items, USD 45 million for construction of powered shells, and approximately USD 233.3 million for general corporate purposes. Long lead-time expenditures include payments for gas-fired generation equipment, Siemens systems, cabling, transformers, and other non-nuclear power generation infrastructure. A portion of proceeds may also be utilized for acquisitions or investments in complementary technologies and solutions.

Dividend policy:

The company, structured as a REIT, is required under U.S. federal tax law to distribute at least 90% of its REIT taxable income annually; however, given its growth phase, substantial capital investments, and high non-cash depreciation charges, it does not expect to generate meaningful REIT taxable income or pay dividends in the near term. While dividends may eventually be declared to satisfy REIT qualification requirements, their authorization will rest with the board and depend on operational results, liquidity, financing covenants, and other relevant factors. If required distributions exceed available cash, dividends could be funded through financings, asset sales, or taxable stock dividends. At present, there is no plan to use IPO proceeds for dividends, and any future dividends, if paid, will generally be taxable to shareholders, with the company annually providing statements detailing the income characterization.

Powering the AI Revolution: Fermi’s Strategic Response to Infrastructure Challenges

- Structural Power Constraints in the AI Era: The exponential growth of AI workloads and hyperscale data centers has created a structural bottleneck in electricity supply, surpassing even land availability as the critical limiting factor for infrastructure expansion. Power shortages, coupled with grid interconnection delays and limited interregional transfers, are expected to widen the gap between demand and supply, with data centers forecast to account for nearly half of U.S. electricity demand growth in the coming years. This imbalance poses significant risks to AI deployment timelines and cost predictability, necessitating scalable, low-carbon, and reliable energy solutions.

- Fermi’s Integrated Energy and Infrastructure Model: Fermi addresses these constraints through a vertically integrated model that combines behind-the-meter power generation with selective grid supplementation. By leveraging a diversified portfolio of natural gas-fired, nuclear, solar, and battery energy storage systems, Fermi offers highly reliable base load energy that minimizes reliance on traditional grid operators and mitigates regulatory and interconnection risks. The company’s strategy also incorporates strong utility partnerships, co-located infrastructure for fuel, water, cooling, and fiber, and a development roadmap capable of delivering up to 11 GW of dispatchable, low-carbon capacity. This model uniquely positions Fermi to provide tenants with predictable, scalable, and cost-efficient infrastructure delivery.

- Expanding Market Opportunity in AI and Data Centers: The market backdrop reinforces the scale of opportunity. The global generative AI market is projected to grow from USD 64 billion in 2023 to USD 457 billion by 2027, with U.S. AI power demand expected to rise nearly fourfold by 2030. Simultaneously, data centers are experiencing a step-change in power density, with next-generation AI deployments requiring up to 240 kW per rack. These dynamics, coupled with capital expenditure of over USD 200 billion on AI-focused infrastructure in 2024 alone and a decentralization of data center builds into Tier 2 and Tier 3 markets, underscore the need for integrated, grid-independent solutions. Fermi’s Project Matador, with its scale, energy independence, and strategic positioning, is well placed to capture this “gravitational pull” of hyperscale tenants and establish itself as a hub for the future of AI and cloud computing.

Financial Highlights (Results of Operations) (Expressed in USD)

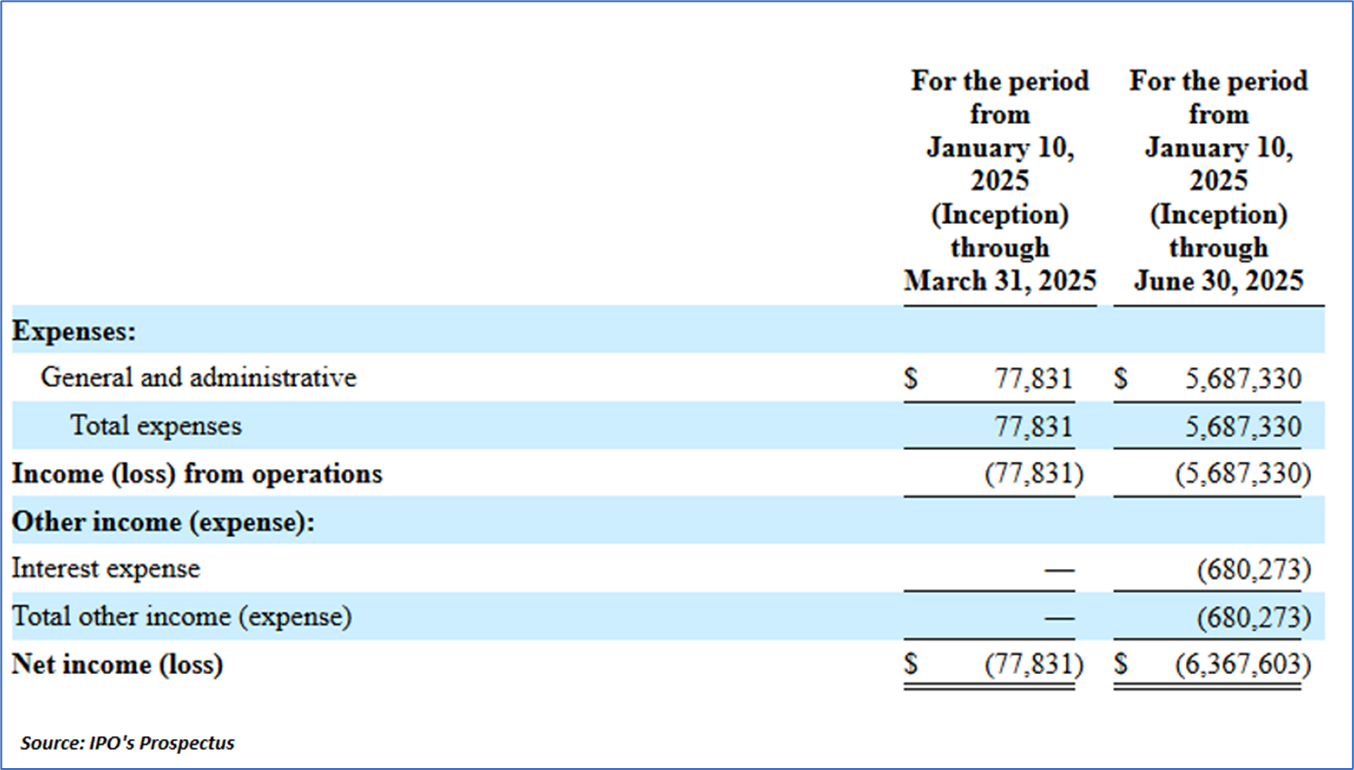

- Strategic Overview and Project Matador: Fermi America, a development-stage REIT, is focused on powering AI infrastructure through Project Matador, a 5,236-acre energy and data center campus in Amarillo, Texas, targeting 11 GW of low-carbon power by 2038, with 1.1 GW online by 2026. Secured via a 99-year lease with Texas Tech University, the project leverages proximity to natural gas fields, a high-radiance solar corridor, and the Pantex Plant’s nuclear expertise to deliver grid-independent power through a mix of natural gas, nuclear, solar, and battery storage. The company has secured key contracts, including a Siemens turbine purchase and a non-binding tenant LOI for 1 GW of powered shell, while its nuclear Combined License Application (COL) was accepted by the NRC in September 2025. Fermi’s REIT structure aims to provide tax-efficient exposure to AI growth, but its lack of revenue and USD 6.4 million net loss through June 30, 2025, reflect significant pre-revenue investments in site preparation, equipment, and regulatory efforts.

- Financial Position and Capital Raising: As of June 30, 2025, Fermi reported USD 40.3 million in cash and USD 85.7 million in debt, with no revenue and a USD 6.4 million loss, driven by USD 3.6 million in share-based compensation, USD 2.1 million in general and administrative expenses, and USD 0.7 million in interest expense. The company raised USD 246.6 million through convertible debt, including USD 26.1 million in Seed Convertible Notes, USD 75.5 million in Series A Convertible Notes, and USD 145 million in Series B Convertible Notes, all converted into Class A Units in August 2025. Additionally, Fermi secured USD 107.6 million via Preferred Units Financing and a USD 100 million Macquarie Term Loan (expandable to USD 250 million) to fund Siemens equipment purchases. The IPO, targeting USD 603.3 million in net proceeds, will support long lead-time equipment (USD 325 million), powered shell construction (USD 45 million), and general corporate purposes (USD 233.3 million), though tenant contracts and further financing are critical to meet the estimated USD 2 billion Phase 0 and 1 capex.

- Operational and Market Risks: Fermi’s revenue model hinges on securing high-credit-quality hyperscaler tenants for long-term, power-centric triple-net leases, with expected revenues starting in 2027. Key risks include failure to secure binding tenant agreements, regulatory delays in nuclear licensing, supply chain disruptions, and technological shifts in AI that could reduce power needs. The company’s September 2025 gas supply agreements with ETC Marketing ensure up to 300,000 MMBtu/day of natural gas for Project Matador, but obligations like a USD 65.3 million assurance payment by January 2026 add financial pressure. Environmental, community, and geopolitical factors, including potential policy shifts or local opposition, could disrupt permitting and operations. Fermi’s phased development plan, targeting 2.6 million square feet of data center capacity by 2026 and scalability to 15 million square feet, relies on successful execution of infrastructure integration and stakeholder coordination to capitalize on the USD 457 billion generative AI market and growing U.S. data center demand.

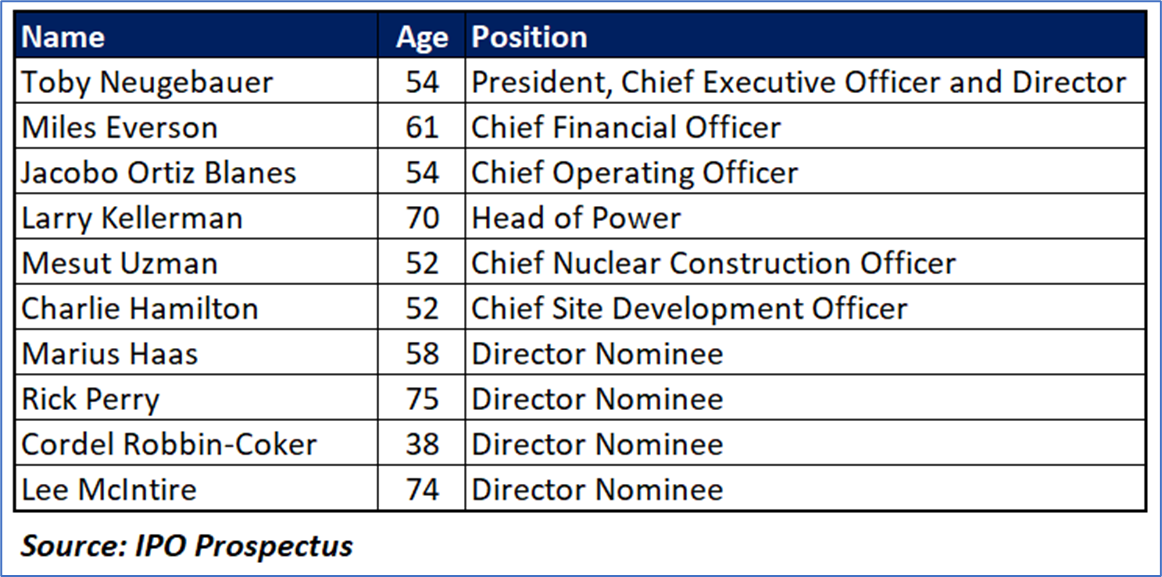

Key Management Highlights

Risk Associated (High)

Investment in the IPO of “FRMI” is exposed to a variety of risks such as:

- Lack of Operating History and Revenue: Fermi, a development-stage REIT, has no operating history or revenue as of June 30, 2025, and reported a net loss of USD 6.4 million. Revenue depends on turning non-binding tenant agreements, like the September 2025 LOI, into binding deals, making financial viability highly uncertain.

- Regulatory and Permitting Challenges: The company’s 4 GW nuclear project with Westinghouse Reactors requires multiple regulatory approvals, including an NRC Combined License Application and environmental permits. Delays, policy shifts, or legal challenges from third parties could inflate costs, extend timelines, and jeopardize scalability, creating significant risk to development progress and tenant commitments.

- Regulatory and Permitting Challenges: Fermi’s revenue strategy relies on hyperscaler tenants through long-term triple-net leases, but income is unlikely before 2027. Failure to secure binding contracts, competitive pressures, or reduced energy needs from AI technology could weaken adoption and jeopardize the USD 2 billion needed for early capital phases.

Conclusion

Fermi LLC (FRMI) directly addresses the AI power crisis with Project Matador, a visionary 11 GW, grid-independent data center and power campus in Texas, targeting 1.1 GW online by 2026. This vertical integration, spanning real estate, natural gas, and future nuclear capacity, creates a critical competitive moat in the foundational AI infrastructure market. The proposed IPO price range of $18-$22 per share implies a bold ~$12-$13 billion valuation for this development-stage company, which currently has zero revenue. Key risks include high execution hurdles for the $2 billion Phase 1 capex, securing binding hyperscaler contracts, and substantial regulatory challenges. Despite this ambitious valuation and high risk, the sector-defining scale and first-mover advantage warrant an “Attractive” rating on “Fermi LLC(FRMI)” at the IPO price.

Past performance is not a reliable indicator of future performance.

Please wait processing your request...

Please wait processing your request...