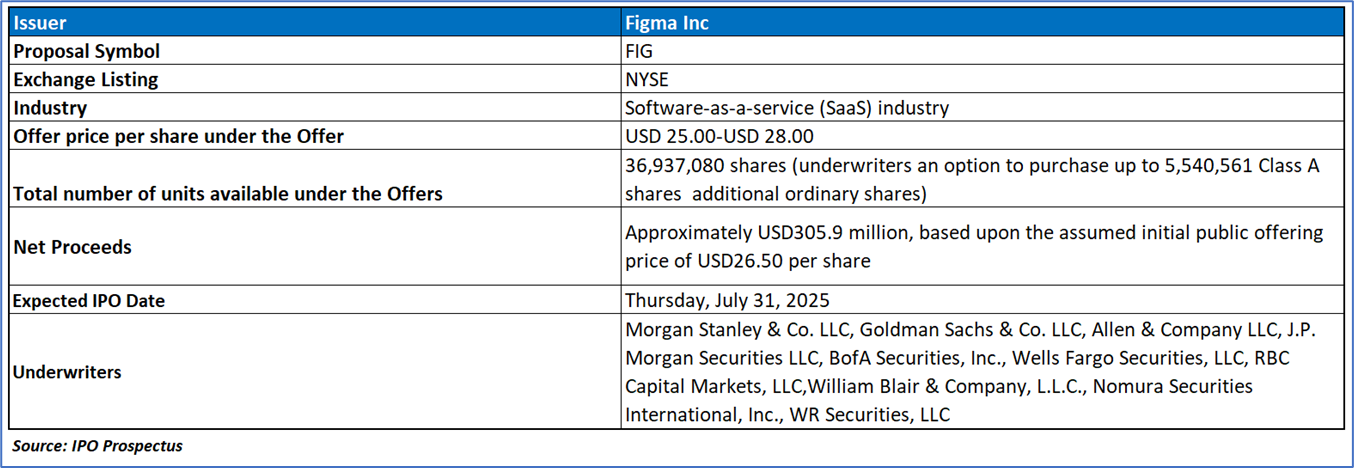

The Offer

Company Overview

Figma, Inc. (FIG) operates within the software-as-a-service (SaaS) industry, specifically focusing on collaborative design and product development platforms. Its browser-based platform, which includes products like Figma Design, FigJam, Figma Slides, Figma Sites, Figma Make, Figma Buzz, and Figma Draw, serves teams across the entire lifecycle of software creation, from ideation to prototyping, development, and marketing. Catering to a diverse user base, including designers, developers, product managers, and marketers, Figma’s AI-powered tools facilitate real-time collaboration and streamline the creation of digital products and experiences for major companies like Google, Uber, and Airbnb.

Key Highlights

Primary Offering:

36,937,080 shares (underwriters an option to purchase up to 5,540,561 Class A shares additional ordinary shares)

Use of proceeds:

- Primary Allocation of Net Proceeds: Figma, Inc. anticipates receiving approximately USD305.9 million in net proceeds from its initial public offering of Class A common stock, based on an assumed offering price of USD26.50 per share, after accounting for estimated underwriting discounts and offering expenses. The company plans to primarily utilize these proceeds, in conjunction with existing cash reserves, to fully repay USD330.5 million of outstanding debt under its Revolving Credit Facility, which matures on June 27, 2030. This debt repayment is intended to address tax withholding and remittance obligations associated with the RSU Net Settlement, estimated at USD330.5 million, assuming a 49.5% tax rate and the stated IPO price. A USD1.00 change in the IPO price would adjust these obligations by approximately USD12.5 million, with any excess obligations covered by cash on hand.

- Strategic Use and Financial Flexibility: Beyond debt repayment, any remaining net proceeds will be directed toward working capital and general corporate purposes, including product development, general and administrative expenses, and capital expenditures. Figma may also allocate a portion of these funds to potential acquisitions or investments in technologies, solutions, or businesses that align with its strategic objectives, although no specific commitments are currently in place.

Dividend policy:

Figma, Inc. currently plans to retain all available funds and future earnings to support the ongoing operations and growth of its business, with no intention to declare or pay dividends on its capital stock in the near term.

Figma, Inc.: Industry Context and Strategic Analysis

- Evolution of Collaborative Design: Figma, Inc. operates within the software-as-a-service (SaaS) industry, specifically in the collaborative design and product development platform sector, addressing the growing demand for efficient, browser-based tools that streamline the creation of digital products. Founded in 2012 by Dylan Field and Evan Wallace, Figma disrupted the traditional design landscape, which was characterized by siloed workflows and fragmented toolchains that hindered collaboration. By leveraging WebGL technology, Figma introduced a pioneering browser-based platform that combines the accessibility of web applications with the performance of native desktop software, enabling real-time collaboration, seamless version control, and universal access via a URL. This innovation has transformed design from an isolated task into a collaborative process, fostering co-creation across designers, developers, product managers, and marketers, and establishing Figma as a critical tool for modern product development.

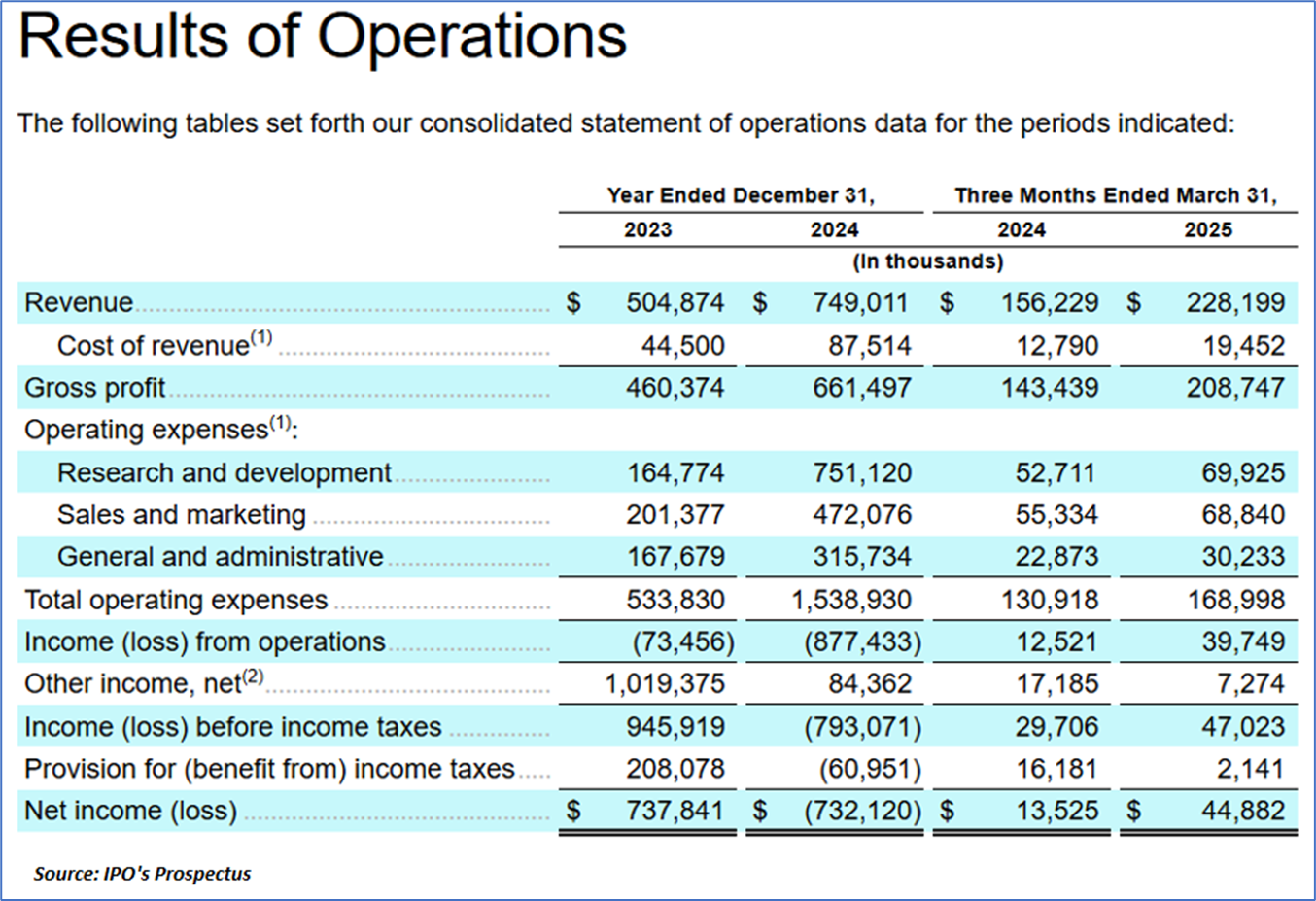

- Market Position and Financial Performance: Figma’s strategic focus on an end-to-end platform, encompassing products like Figma Design, FigJam, Figma Slides, Figma Sites, Figma Make, Figma Buzz, and Figma Draw, has positioned it as a system of record for design and product development, capitalizing on the exponential growth of software and digital experiences. The company reported robust financial performance, with revenue of USD749.0 million in 2024, reflecting 48% year-over-year growth, and USD228.2 million for Q1 2025, up 46% from Q1 2024, alongside a four-year compounded annual revenue growth rate of 53%. Despite a 2024 operating margin of (117)% due to one-time events like the May 2024 RSU Release and Stock Option Grants, Figma achieved a non-GAAP operating margin of 17% in 2024 and 18% in Q1 2025, with a Net Dollar Retention Rate of 132% as of March 31, 2025. Serving 95% of the Fortune 500 and 78% of the Forbes Global 2000, Figma’s platform supports 13 million monthly active users, with non-designers comprising two-thirds, highlighting its broad adoption across diverse roles.

- Future Opportunities and Industry Impact: Figma is well-positioned to capitalize on a USD33 billion total addressable market, as estimated by IDC, driven by the global workforce engaged in software design and the projected growth of software spending to over USD1.2 trillion in 2025, per Gartner. The rise of generative AI and the increasing importance of design in differentiating digital products underscore Figma’s relevance, as its AI-powered features, such as Figma Make, enable rapid prototyping and task automation, enhancing efficiency across the product development lifecycle. The company’s extensible ecosystem, with over 250,000 community-created resources and 10,000 plugins, further strengthens its platform by allowing customization and integration with external tools. As digital transformation accelerates and companies prioritize well-crafted user experiences to compete for customer attention, Figma’s innovative, collaborative, and AI-enhanced platform positions lead to the evolving landscape of software design and development.

Financial Highlights (Results of Operations) (Expressed in USD)

- Revenue Growth and Customer Expansion: Figma, Inc. demonstrated strong financial performance in the first quarter ended March 31, 2025, reporting revenue of USD228.2 million, a 46% year-over-year increase from USD156.2 million in Q1 2024. This growth was driven by a robust Net Dollar Retention Rate of 132%, reflecting significant expansion within existing customers, and a substantial increase in Paid Customers, with those generating over USD10,000 in Annual Recurring Revenue (ARR) rising 39% to 11,107 and those exceeding USD100,000 in ARR growing 47% to 1,031. Approximately 70% of revenue for the quarter came from customers on Organization and Enterprise plans, underscoring Figma’s success in serving larger organizations with advanced features tailored to their needs. The company’s scalable platform, utilized by 450,000 Paid Customers globally, continues to drive adoption across diverse industries, supported by its ability to meet evolving demands through new product offerings and enhanced functionality.

- Operating Performance and Expense Dynamics: Figma achieved a non-GAAP operating margin of 18% in Q1 2025, an improvement from 17% for the full year 2024, and recorded a net income of USD44.9 million, a significant increase from USD13.5 million in Q1 2024, despite a 2024 full-year net loss of USD732.1 million impacted by one-time events, including the May 2024 RSU Release and Stock Option Grants. Operating expenses increased notably, with research and development costs rising 33% to USD69.9 million, driven by a USD12.0 million increase in employee-related costs due to higher headcount and a company-wide bonus program, alongside USD2.6 million in AI-related technical infrastructure costs. Sales and marketing expenses grew 24% to USD68.8 million, reflecting increased headcount and marketing initiatives, while general and administrative expenses rose 32% to USD30.2 million, primarily due to higher professional service fees and employee costs. These investments highlight Figma’s commitment to innovation and global expansion, particularly in enhancing its AI-powered product development platform.

- Financial Position and Strategic Outlook: Figma’s financial position was further strengthened by a 96% Gross Retention Rate as of March 31, 2025, indicating strong customer loyalty, and a significant reduction in the provision for income taxes to USD2.1 million, down 87% from USD16.2 million in Q1 2024, due to additional U.S. tax deductions from net operating loss carryforwards. Other income, net, decreased by 58% to USD7.3 million, primarily due to an USD8.6 million reduction in unrealized gains on equity securities, including investments in a Bitcoin exchange-traded fund. With 85% of its 13 million monthly active users based outside the U.S., yet only 53% of revenue from non-U.S. markets, Figma sees substantial opportunities for international growth, supported by its multilingual platform and offices in seven countries. The company’s financial results, coupled with its strategic focus on expanding its collaborative design ecosystem and leveraging AI to streamline product development, position Figma for sustained long-term growth in the rapidly evolving software-as-a-service industry.

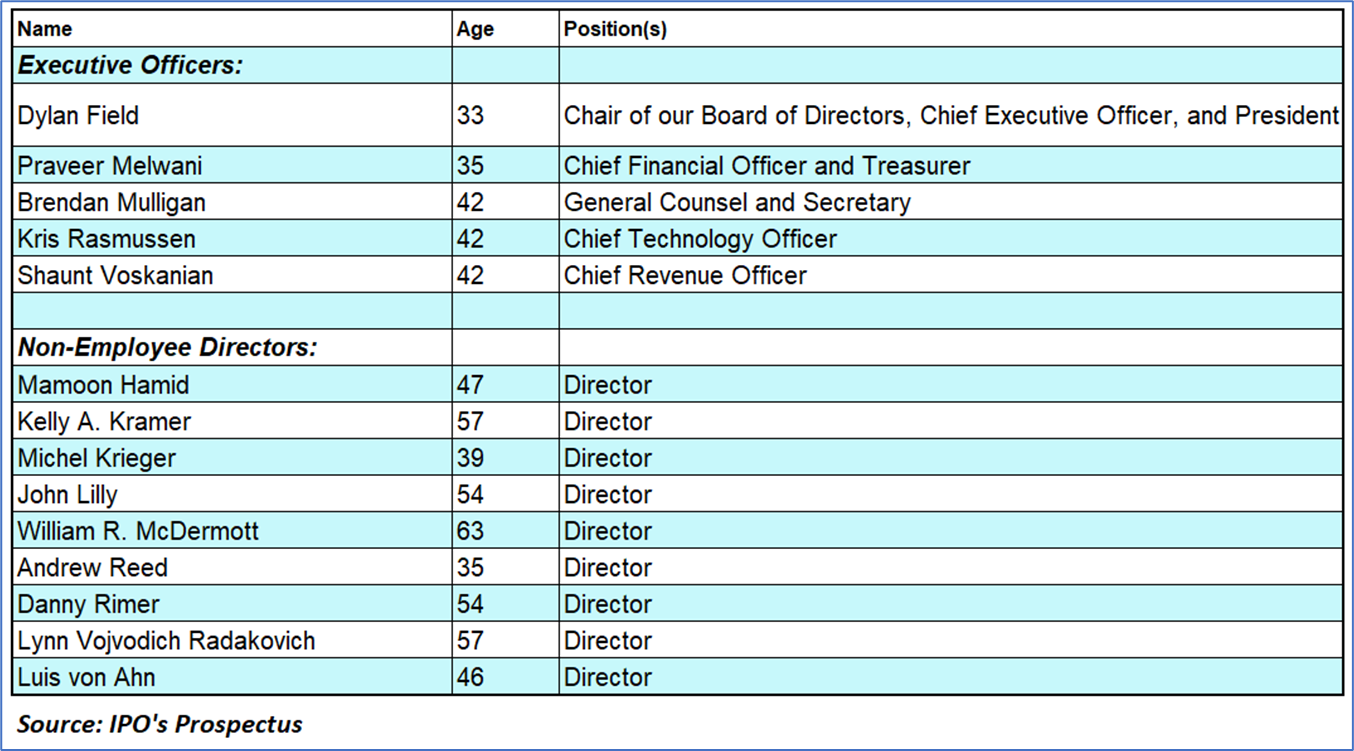

Key Management Highlights

Risk Associated (High)

Investment in the IPO of “FIG” is exposed to a variety of risks such as:

- Dependence on AI Innovation and Competitive Pressures: Figma faces significant risks from the rapid evolution of AI-driven design tools, which could reduce customer reliance on its platform if competitors develop superior AI capabilities. As noted in recent discussions, Figma acknowledges that AI advancements might make some customers less dependent on its services, particularly as generative AI simplifies the creation of digital products. The company’s heavy investment in AI features, such as Figma Make, which transforms prompts into functional prototypes, is still in early stages, with many new products in beta testing. Failure to maintain technological relevance or to successfully integrate proprietary AI models could erode Figma’s competitive edge against rivals like Canva, Axure, or emerging AI-native platforms, potentially impacting its 46% year-over-year revenue growth and 132% Net Dollar Retention Rate as of March 31, 2025.

- Cost Structure and Vendor Lock-In: Figma’s cost of revenue is growing faster than its top line, driven by increasing technical infrastructure and hosting expenses, particularly its USD100 million annual AWS bill, which represents 12% of its 2024 revenue of USD749.0 million. A five-year, USD545 million hosting agreement with AWS creates significant vendor lock-in, limiting Figma’s flexibility to negotiate costs or switch providers, which could strain margins if revenue growth slows. For Q1 2025, cost of revenue increased 52% to USD19.6 million, outpacing the 46% revenue growth, with USD3.5 million attributed to higher hosting and AI-related costs. This rising cost structure, combined with potential macroeconomic pressures affecting customer spending, poses a risk to Figma’s profitability, which improved to a 17% operating margin in Q1 2025 from a (117)% margin in 2024.

- Dual-Class Share Structure and Governance Risks: Figma’s dual-class share structure, granting CEO Dylan Field 74% of voting rights, concentrates decision-making power and may limit shareholder influence on critical strategic choices, such as mergers and acquisitions or capital allocation. This structure, while ensuring founder-led stability, could lead to governance risks if Field’s decisions, such as the planned USD30 million additional investment in Bitcoin or aggressive M&A strategies, do not align with broader investor interests. The company’s Bitcoin holdings, approximately USD70 million as of March 31, 2025, introduce volatility risks due to cryptocurrency’s 20%+ price swings, potentially impacting stock price stability post-IPO. Additionally, Figma’s ambitious M&A plans, as flagged in a board memo, could heighten execution risks if acquisitions like the recent Payload CMS deal fail to deliver expected synergies.

Conclusion

Figma, Inc., a leading SaaS provider in the collaborative design and product development platform sector, reported robust financial performance for Q1 2025, with revenue of USD228.2 million, reflecting 46% year-over-year growth, driven by a 132% Net Dollar Retention Rate and a 39% increase in Paid Customers with over USD10,000 in ARR. The company achieved a non-GAAP operating margin of 18% and net income of USD44.9 million, though its cost of revenue grew faster at 52%, primarily due to increased AWS hosting and AI-related expenses. Figma faces risks from rising AI competition, a high-cost structure with significant AWS vendor lock-in, and governance concerns due to its dual-class share structure, which grants CEO Dylan Field 74% voting control. The company plans to use USD305.9 million in IPO net proceeds to repay USD330.5 million in debt and support general corporate purposes, while its no-dividend policy reflects a focus on reinvesting earnings for growth. Figma’s platform, serving 95% of the Fortune 500 and leveraging AI and community-driven resources, positions it for continued expansion in a USD33 billion addressable market, though macroeconomic uncertainties and technological disruptions remain challenges.

Hence, given the financial performance of the company, use of proceeds, and associated risks “Figma Inc (FIG)” IPO seems “Neutral" at the IPO price.

Past performance is not a reliable indicator of future performance.

Please wait processing your request...

Please wait processing your request...