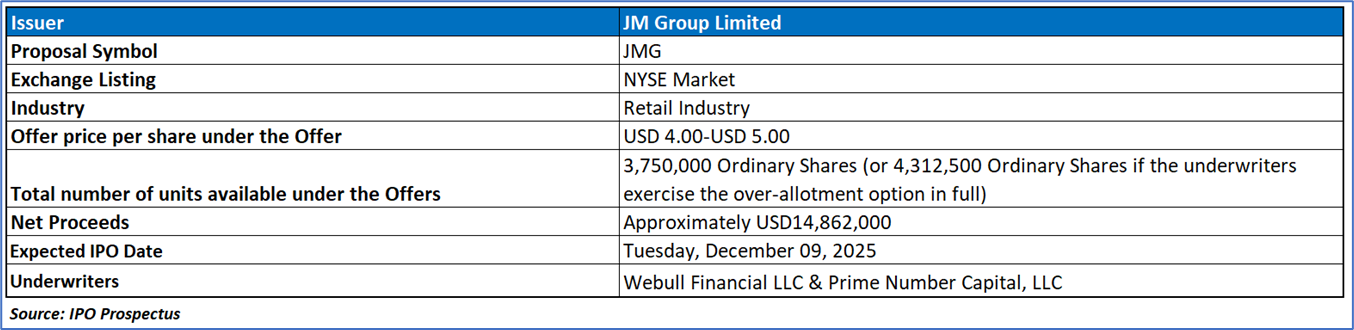

The Offer

Company Overview

JM Group Limited (JMG) is a Hong Kong–headquartered sourcing solutions provider that globally sources and wholesales a diverse portfolio of consumer products across eight major categories, including sports and outdoor goods, toys and games, seasonal décor, electronics, home and tools, school and office supplies, clothing and accessories, and personal care items. Serving retailers, distributors, and wholesalers in markets such as Australia, Hong Kong, Mexico, and the United States, the Company works primarily with manufacturing partners in mainland China, producing items based on in-house designs or customer specifications. Its operations are supported by value-added services—including market research, trend analysis, product and packaging design, and quality management—which, while not direct revenue generators, play a critical role in product development, customer support, and ensuring efficient and compliant sourcing workflows.

Key Highlights

Primary Offering:

3,750,000 Ordinary Shares (or 4,312,500 Ordinary Shares if the underwriters exercise the over-allotment option in full)

Use of proceeds:

- Overview of Expected Net Proceeds and Allocation Framework: JM Group anticipates receiving approximately USD 14.86 million in net proceeds from the offering, based on an assumed IPO price of USD 4.50 per ordinary share and excluding any exercise of the over-allotment option. The Company intends to allocate these funds evenly across four primary areas—brand promotion and marketing, recruitment of talent, strategic investments and acquisitions, and general working capital—each representing 25% of the net proceeds. While these allocations reflect current plans and operating conditions, management retains full discretion to adjust the deployment of funds as circumstances evolve, with any unused proceeds temporarily placed in short-term, interest-bearing deposits or debt instruments.

- Planned Use of Funds for Growth, Capability Building, and Strategic Expansion: A portion of the proceeds is designated to enhance JM Group’s brand visibility and strengthen its professional image, supporting trust-building with existing and prospective customers and facilitating feasibility studies for expansion into the U.S., Europe, and broader Asian markets. Another allocation is dedicated to human capital development, with plans to recruit additional administrative, executive, accounting, marketing, sales, design, and research personnel to support business expansion and new product development. Additionally, the Company intends to set aside funds for potential strategic investments or acquisitions in complementary businesses, products, or services, although no specific commitments or targets have been identified at this stage.

- Working Capital and Operational Flexibility: JM Group also plans to reserve 25% of the net proceeds for general working capital to support daily operations and maintain financial flexibility amid changing economic conditions. This allocation is intended to provide a buffer for routine business needs while ensuring stability in operational execution. Overall, the proposed use of proceeds reflects the Company’s current strategic priorities, though management maintains flexibility to reallocate funds as required to support future developments and operational demands.

Dividend policy:

JM Group’s dividend policy permits its board of directors to declare dividends when satisfied that the Company will remain solvent after such distribution, in accordance with the BVI Act and its governing documents. Historically, its Hong Kong subsidiary, JM Manufacturing HK, paid dividends to its former sole shareholder in 2021 and 2022; however, JM Group itself has not declared or paid any dividends to date. As a holding company, any future dividends would depend on fund transfers from JM Manufacturing HK, which are not subject to Hong Kong dividend withholding tax. At present, JM Group intends to retain available funds for business operations and expansion and does not anticipate paying dividends in the foreseeable future, with any future decision subject to the board’s discretion and financial and operational considerations.

Market and Industry Overview

- Home and Tools Sector: The home and tools sector, which includes home décor, furnishings, textiles, lighting, and related categories, represents a major revenue driver for JM Group. Global research reports indicate steady long-term expansion in the home décor market, with estimates projecting growth from approximately USD 619–749 billion in 2023 to USD 882–1,087 billion by 2032, supported by rising income levels and expanding middle-class populations, particularly in the Asia-Pacific region. The United States remains the largest contributor to global demand due to its high concentration of middle-income and affluent households. Key market drivers include the adoption of eco-friendly materials, integration of smart technologies, growth in e-commerce, and strong influence from social media. However, the sector faces restraints such as reduced spending during economic uncertainty and higher compliance costs associated with environmental and safety regulations.

- Seasonal Décor and Party Supplies Sector: The seasonal décor and party supplies segment encompasses decorations, tableware, balloons, themed accessories, and other celebration-related products. Global market studies estimate growth from USD 19.8 billion in 2023 to between USD 24 billion and USD 30.8 billion by 2032–2033, driven by increased personalization, demand for sustainable materials, technological innovation, and expanding online retail channels. North America—particularly the United States—remains the dominant market, supported by strong cultural emphasis on celebrations and high disposable income levels. Key opportunities arise from eco-friendly product lines, customizable offerings, and rising demand from corporate and government events. Key challenges include intensifying competition, consumer budget reductions during economic slowdowns, and supply-chain disruptions linked to geopolitical and global health events.

- Sports and Outdoors Sector: The sports and outdoors category includes outdoor toys, sports equipment, water and winter sports toys, playground items, and motorized outdoor toys. Multiple industry reports estimate the market at USD 10–15 billion in 2023, with projected growth to USD 13.7–23.2 billion by 2031–2032, representing a CAGR range of 4%–5.3%. North America accounts for more than 30% of global demand. Growth in this sector is primarily driven by rising health consciousness, greater focus on physical activity, and the incorporation of innovative materials and smart features such as sensors and app-connectivity. However, the sector is constrained by potential economic downturns affecting discretionary spending, increasing regulatory requirements, supply-chain volatility, and intensified competition from low-cost manufacturers.

- Toys and Games Sector: The toys and games sector encompasses puzzles, preschool toys, construction sets, dolls, accessories, outdoor and sports toys, video games, and related categories. Global market estimates for 2023 range from USD 113.5 billion to USD 190.7 billion, with forecasts reaching USD 170.9–299.8 billion by 2032, supported by diversified demographics, strong demand for educational and developmental products, and high levels of discretionary income in markets such as the United States. Although U.S. toy retail sales declined in 2023, the market remains the world’s largest and continues to contribute significantly to the national economy. Digital retail platforms and social media play important roles in shaping consumer preferences and product trends. Restraints affecting the sector include sensitivity to economic cycles, supply-chain instability, increased cost of regulatory compliance, and heightened competition, particularly from lower-priced producers.

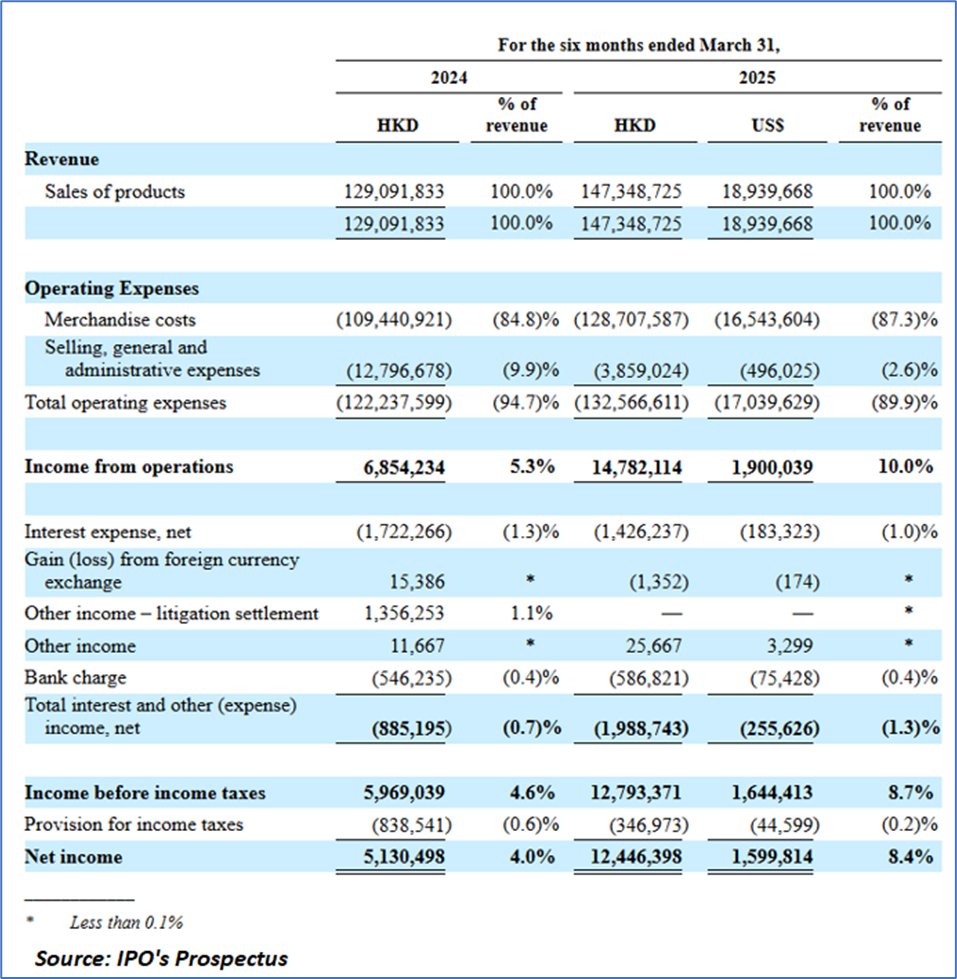

Financial Highlights (Results of Operations) (Expressed in USD)

- Revenue Performance and Cost Dynamics: For the six months ended March 31, 2025, JM Group’s revenue increased 14.1% to HKD147.35 million (USD 18.94 million), compared with HKD129.09 million in the prior-year period. Growth was driven primarily by stronger demand in the sports and outdoors and personal care categories, along with contributions from a newly acquired customer. Product mix shifted notably, with sports and outdoors sales rising 32% and personal care sales more than doubling year over year. Merchandise costs rose 17.6% to HKD128.71 million (USD 16.54 million), increasing slightly faster than revenue due to higher sales volume, resulting in modest gross margin pressure. The Company retained a stable relationship with its top U.S. customer, which continued to contribute across multiple product categories.

- SG&A Trends, Operating Profitability, and Bottom-Line Results: Selling, general, and administrative expenses declined significantly to HKD3.86 million (USD 0.50 million) from HKD12.80 million, mainly due to a substantial HKD10.45 million reversal of expected credit losses following major customer repayments. Excluding this reversal, underlying SG&A grew modestly, driven by higher staff costs, marketing expenses aligned with sales growth, and increased professional and audit fees related to U.S. listing preparation. Operating income more than doubled, rising 116% to HKD14.78 million (USD 1.90 million). Net income increased 143% to HKD12.45 million (USD 1.60 million), supported by improved operating performance and lower interest expenses, reflecting reduced reliance on factoring arrangements and slightly lower benchmark interest rates. Tax expenses declined due to the Company’s position under the Hong Kong two-tiered profits tax regime.

- Cash Flow Position and Financing Activities: Operating cash flow improved to HKD4.80 million (USD 0.62 million), compared with HKD1.67 million in the prior-year period, supported by higher profitability, reduced accounts receivable, and lower prepayments. Working capital movements included decreases in accounts payable and accrued expenses, reflecting repayment timing and completion of listing-related professional services. Investing activities generated HKD6.97 million (USD 0.90 million), primarily due to shareholder-related inflows, compared with an outflow in the prior year. Financing activities provided HKD0.99 million (USD 0.13 million), driven by bank loan and factoring proceeds, contrasting with a net outflow in the prior-year period due to loan repayments. Overall, JM Group demonstrated stronger liquidity and operational cash generation alongside improved earnings quality in the six-month period.

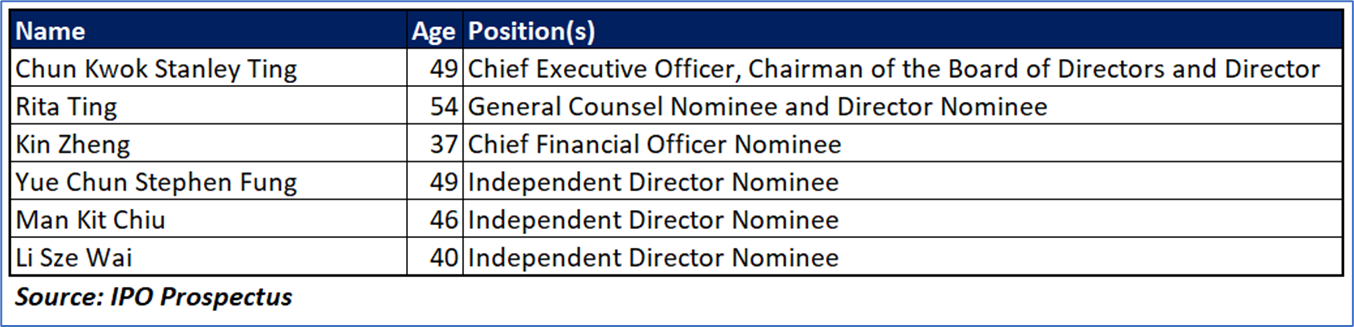

Key Management Highlights

Risk Associated (High)

Investment in the IPO of “JMG” is exposed to a variety of risks such as:

- High Dependence on a Concentrated Customer Base: JM Group relies heavily on a small number of key customers, including one major U.S.-based client that contributes a significant portion of total revenue across multiple product categories. Any loss, reduction in orders, delayed payments, or changes in procurement strategies by these customers could materially affect the Company’s revenue stability, cash flows, and overall business performance.

- Reliance on Mainland China–Based Suppliers and Manufacturing Partners: The Company’s sourcing model depends primarily on manufacturers located in mainland China, exposing it to supply-chain disruptions arising from regulatory changes, geopolitical tensions, cost inflation, logistics bottlenecks, or quality-control challenges. Disruptions in production or delays in fulfillment could adversely impact JM Group’s ability to meet customer delivery timelines and contractual obligations.

- Exposure to Earnings Volatility Due to Low Margins and Rising Operating Costs: JM Group operates in highly price-sensitive product categories with limited gross margins, while merchandise costs and compliance-related expenses continue to rise. In addition, SG&A expenses—such as professional fees, staff costs, and marketing expenditure—are increasing in line with business expansion. Any mismatch between revenue growth and cost escalation could pressure profitability and weaken financial resilience.

Conclusion

JM Group Limited (JMG) is a Hong Kong–based sourcing solutions provider that supplies a broad range of consumer products across eight major categories to customers in markets including the U.S., Australia, Mexico, and Hong Kong, supported by in-house design, product development, and quality management capabilities. Through its IPO, the Company plans to raise approximately USD 14.86 million, which it intends to allocate evenly toward brand promotion, talent recruitment, strategic investments, and general working capital, with flexibility retained for future adjustments. JMG operates within several expanding global markets—including home and tools, seasonal décor, sports and outdoors, and toys and games—each driven by long-term trends such as rising disposable income, increased health and lifestyle awareness, demand for customization, and growth of e-commerce, though each faces constraints ranging from economic sensitivity to supply-chain and regulatory pressures. Financially, JMG reported a 14.1% increase in revenue for the six months ended March 31, 2025, stronger profitability driven by lower SG&A due to a major credit-loss reversal, and improved operating cash flow alongside modest increases in merchandise costs tied to higher sales volume. Key risks include concentration of revenue with a major U.S. customer, reliance on mainland China suppliers, and exposure to margin pressures within highly competitive, price-sensitive product categories.

Hence, given the financial performance of the company, use of proceeds, and associated risks “JM Group Limited (JMG)” IPO seems “Neutral" at the IPO price.

Past performance is not a reliable indicator of future performance.

Please wait processing your request...

Please wait processing your request...