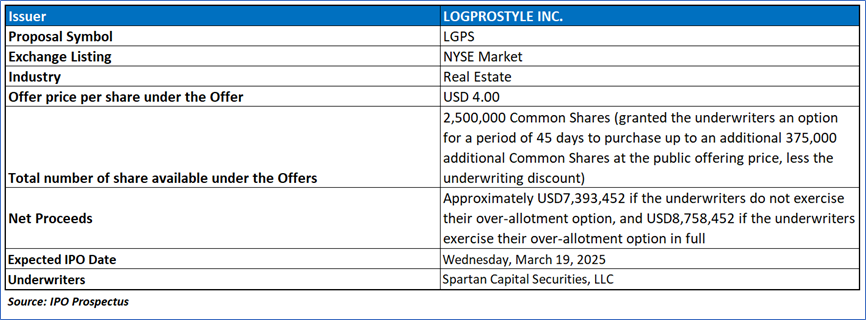

The Offer

Company Overview

Logprostyle Inc., a Japan-based holding company, operates subsidiaries in real estate renovation, development, and hotel management, with LogSuite renovating over 1,700 “Log Mansion” condominiums using in-house wood production, and Prostyle developing residential and “Machinaka Ryokan” hotels. Targeting affluent and international clients, the company’s one-stop service model enhances efficiency and differentiation across its Tokyo, Yokohama, and Okinawa markets.

Key Highlights

Primary Offering:

2,500,000 Common Shares (granted the underwriters an option for a period of 45 days to purchase up to an additional 375,000 additional Common Shares at the public offering price, less the underwriting discount).

Use of proceeds:

- Net Proceeds Estimate: At an assumed IPO price of USD 4.00 per share, LGPS expects net proceeds of approximately USD 7,393,452 without the over-allotment option, or USD 8,758,452 if the underwriters exercise it in full, after deducting underwriting discounts and offering expenses.

- Allocation for ProstyleRyokan Expansion (70%): Approximately 70% of the proceeds will fund the development and management of additional Machinaka Ryokans in Japan (Tokyo, Osaka, Kyoto) and international markets (U.S. cities like New York and Los Angeles, and Dubai, UAE), including joint ventures with Allocation for Real Estate Business Expansion (30%): About 30% will support the expansion of LGPS’s “Log Mansion” real estate renovation and resale business in Kyoto, Osaka, Nagoya, other Asian regions, and the U.S. through investments or acquisitions of local real estate firms.

- Potential Collaborations and Flexibility: LGPS may allocate proceeds to explore hotel and restaurant development opportunities in the Middle East and North Africa via a memorandum of understanding with VAULT INVESTMENT LLC, though specific plans are not yet finalized; management retains discretion to redirect proceeds if business conditions change, with unused funds to be invested in short-term, interest-bearing instruments.

Dividend policy:

Logprostyle Inc. (LGPS) paid annual dividends of 55 Japanese yen (approximately USD 0.36) per Common Share, totaling 346,940,000 Japanese yen (approximately USD 2,294,273) for the fiscal year ended March 31, 2022; however, future dividend payments will be subject to approval by shareholders at the annual meeting and the board of directors, contingent on factors such as operational results, cash requirements, financial condition, and contractual restrictions, with potential limitations from future agreements or indebtedness, and compliance with Japan’s Companies Act, which caps dividends at a calculated distributable amount to ensure financial stability.

Market Opportunities for Logprostyle Inc. (LGPS)

- Real Estate Markets in Japan: The real estate industry in Japan is influenced by economic growth, employment levels, demographic trends (e.g., population growth and urbanization), interest rates impacting mortgage affordability, government policies such as tax incentives and housing subsidies, and the availability of financing, all of which shape the demand for residential and commercial properties and the sector’s overall health.

- General Geographical Market Trends: Despite a projected decline in condominium demand due to Japan’s aging population, the National Institute of Population and Social Security Research (IPSS) forecasts stability in Tokyo’s population over the next 25 years, with a notable increase to 119.5% of the 2015 level by 2045 in the central wards of Chiyoda, Chuo, and Minato (key areas for LGPS’s renovation business), driven by intensified urban population concentration among the 25-60 age group.

- Governmental Policies Regarding Residential Real Estate: The Japanese government offers tax exemptions on monetary gifts from ascendants for home construction, purchase, or renovation, and allows income tax deductions based on housing loan balances for properties acquired between January 1, 2022, and December 31, 2025, extended in 2024 to mitigate the impact of prior consumption tax increases, thereby supporting housing demand.

- Market Outlook for New Condominium Units: In 2023, new condominium prices in the greater Tokyo metropolitan area rose by 28.8% to an average of JPY 81.01 million (approximately USD 536,000), with a 39.4% increase to JPY 114.83 million (approximately USD 759,000) in Tokyo’s inner 23 wards, attributed to higher land, labor, and material costs, while contract rates remained stable at 70.3% overall and rose to 71.0% in the 23 wards, supported by low mortgage rates (e.g., Flat 35 at 1.85% in June 2024) and a promising 3.2% supply increase forecast for 2024.

- Market Outlook for Pre-Owned Condominium Units: Since 2019, pre-owned condominium contracts in the greater Tokyo area have exceeded new unit supplies, with 35,987 contracts in 2023 (up 1.6%), driven by affordability (average price per square meter at JPY 719,000 or USD 5,000, 6.9% higher than 2022), though prices have risen 88.3% over 11 years; demand for renovated older units (e.g., 21-30 years and over 31 years) is growing, aligning with LGPS’s renovation focus.

Financial Highlights (Results of Operations) (Expressed in USD)

- Revenue Growth and Key Drivers: Logprostyle Inc. (LGPS) reported a revenue increase of 6.5% year-over-year, rising by JPY 857,432 thousand to JPY 14,121,840 thousand (USD 93,386 thousand) for the fiscal year ended March 31, 2024. This growth was primarily driven by a JPY 457,422 thousand rise in real estate revenue, fueled by increased sales of new condominiums (15 units sold compared to 10 in the prior year) and renovated condominiums (42 units sold compared to 31), alongside a JPY 353,585 thousand increase in hotel accommodation services revenue, attributed to a higher occupancy rate (70.8% versus 53.6%) and elevated average daily rates (JPY 23,000 or USD 0.2 thousand versus JPY 17,000), reflecting a surge in tourism post-COVID-19.

- Cost of Revenues, Gross Profit, and Margin Analysis: The cost of revenues for LGPS rose by 6.7% or JPY 725,025 thousand to JPY 11,469,951 thousand (USD 75,849 thousand), aligning with the increased revenue and associated direct costs. Gross profit for the fiscal year stood at JPY 2,667,194 thousand (USD 17,638 thousand), up from JPY 2,532,854 thousand the previous year, though the gross profit margin slightly declined from 19.1% to 18.9%. Selling, General, and Administrative (SG&A) expenses increased by 6.9% or JPY 110,761 thousand to JPY 1,713,388 thousand (USD 11,330 thousand), driven by higher payroll costs from new director appointments and staff additions, as well as increased brokerage fees due to higher sales volumes.

- Net Income, Other Expenses, and Cash Flow Dynamics: Net income for LGPS decreased to JPY 323,605 thousand (USD 2,141 thousand) from JPY 354,025 thousand the prior year, impacted by a 34.3% rise in other expenses, which increased by JPY 106,854 thousand to JPY 418,542 thousand (USD 2,768 thousand) due to higher interest expenses from an elevated average loan balance. Cash flow from operating activities improved, with net cash used decreasing to JPY 2,083,273 thousand (USD 13,776 thousand) from JPY 3,655,316 thousand (USD 24,172 thousand), driven by increased contract liabilities and consumption tax collections. However, investing activities saw a net cash outflow of JPY 13,538 thousand (USD 90 thousand) compared to a prior inflow of JPY 17,851 thousand (USD 118 thousand) due to increased property, plant, and equipment acquisitions, while financing activities provided JPY 2,909,974 thousand (USD 19,243 thousand), down from JPY 3,576,111 thousand (USD 23,648 thousand), due to higher loan repayments.

Key Management Highlights

Risk Associated (High)

Investment in the IPO of “LGPS” is exposed to a variety of risks such as:

- Market and Demographic Risks: LGPS faces significant exposure to demographic shifts in Japan, particularly the aging population and declining condominium demand outside Tokyo, as highlighted by the National Institute of Population and Social Security Research (IPSS). While Tokyo’s central wards (Chiyoda, Chuo, Minato) show population growth among the 25-60 age group, a broader decline could reduce demand for its “Log Mansion” renovated units and new condominiums, potentially impacting revenue stability.

- Economic and Interest Rate Volatility: The company’s real estate and hotel businesses are sensitive to interest rate fluctuations and economic conditions, which influence mortgage affordability and investor returns. Rising interest rates, as seen with the Flat 35 mortgage rate increasing to 1.85% by June 2024, or potential tightening of credit conditions, could dampen buyer willingness, particularly for high-end properties in Tokyo, affecting LGPS’s sales and profitability.

- Operational and Financial Leverage Risks: LGPS’s increased reliance on loans, as evidenced by higher interest expenses (JPY 418,542 thousand in 2024) and loan repayments (reducing net cash from financing to JPY 2,909,974 thousand), introduces financial risk. Coupled with rising costs of revenues (JPY 11,469,951 thousand) and SG&A expenses (JPY 1,713,388 thousand), any unexpected market downturn or failure to generate sufficient cash flow could strain liquidity, especially with planned expansions into international markets like the U.S. and UAE.

Conclusion

The company has diversified revenue streams from renovation, development, and hotel operations contribute to financial stability and resilience against market fluctuations. The company's control over natural solid wood supply chains helps manage costs effectively, maintaining profitability in a competitive market. Further, the company's focus on niche targeting in both renovation and hotel management allows it to differentiate its products and services, appealing to affluent individuals and international customers. This strategy enhances its competitive edge in the market. The "Log Mansion" brand has sold over 1,700 renovated condominium units, establishing a strong reputation in central Tokyo. The company operates across multiple sectors, including real estate renovation, development, hotel management, and restaurant management, reducing reliance on a single market segment. With a strong brand reputation and diversified revenue streams, LGPS is well-positioned for future growth, particularly in the Tokyo market where it has established a significant presence. The company's ability to manage costs effectively and its improving cash flow dynamics further enhance its investment appeal. Hence, given above rationale and associated risks “LOGPROSTYLE INC. (LGPS)” IPO seems “Attractive" at the IPO price.

Past performance is not a reliable indicator of future performance.

Please wait processing your request...

Please wait processing your request...