The Offer

Company Overview

Medline Inc. (MDLN) is the largest provider of medical-surgical products and integrated supply-chain solutions in the U.S., offering approximately 335,000 mission-critical items across all care settings and distributing them through a vast global logistics network of 69 facilities and over 2,000 owned trucks, enabling next-day delivery to 95% of U.S. customers. Built on a vertically integrated model combining manufacturing, sourcing, and distribution, Medline leverages its Medline Brand and Supply Chain Solutions segments to deliver high-quality, cost-efficient products and services, strengthening long-term Prime Vendor partnerships that create visibility into customer demand and reinforce a recurring revenue base that has compounded at 18% annually since inception. The company’s expansive product portfolio, differentiated logistics capabilities, and customer-centric culture—supported by a 3,800-member commercial team—enable Medline to expand wallet share, enhance operating efficiency, and drive superior value across hospitals, ambulatory centers, physician offices, and post-acute facilities. With a track record of consistent organic growth, resilience through economic cycles, and a portfolio dominated by recurring consumables, Medline is well positioned to capitalize on rising healthcare utilization, customer consolidation, channel expansion, new product development, selective M&A, and international scaling to sustain long-term revenue and earnings growth.

Key Highlights

Primary Offering:

179,000,000 shares (or 205,850,000 shares if the underwriters exercise in full their option to purchase additional shares of Class A common stock)

Use of proceeds:

Primary Use of Base Offering Proceeds: Medline Inc. expects to generate approximately USD 4.899 billion in net proceeds from the base offering at an assumed IPO price of USD 28 per share, with sensitivity of roughly USD 175 million for every USD 1 change in the IPO price. These funds will be used to acquire an equivalent number of newly issued Common Units from Medline Holdings, aligning with the planned organizational and capital structure transactions described in the prospectus.

Debt Repayment and Corporate Allocation Strategy: Medline Holdings will deploy approximately USD 729 million of these proceeds to fully repay the outstanding balance under the New Euro Term Loan Facility and USD 3.280 billion to partially repay the 2028 Refinancing Term Loan Facility, with both loans maturing in October 2028 and carrying variable interest structures linked to EURIBOR or SOFR benchmarks. The remaining proceeds will support general corporate purposes and cover estimated offering expenses of USD 38 million, thereby strengthening Medline’s balance sheet and reducing interest burdens through refinancing of previously higher-margin term loans.

Use of Additional Proceeds from Over-Allotment Option: If underwriters exercise their option to purchase up to 26.85 million additional shares, Medline anticipates receiving roughly USD 735 million in incremental proceeds, which will be used exclusively to purchase or redeem outstanding Common Units and Class A shares from certain pre-IPO owners at the IPO price net of underwriting discounts. These proceeds will not be retained by Medline, but will instead facilitate ownership transitions outlined in the organizational structure and principal stockholder disclosures.

Dividend policy:

Medline Inc. does not currently plan to pay dividends on its Class A common stock, and any future dividend decisions will rest solely with the board based on cash availability, legal constraints, debt covenants, and broader financial considerations. As a holding company, Medline Inc. depends entirely on distributions from Medline Holdings to fund taxes, expenses, tax receivable agreement obligations, and any dividends it may declare, with all Common Unit holders receiving distributions on a pro rata basis. While excess cash from tax distributions may allow Medline Inc. to fund share repurchases, acquire additional Common Units, or potentially pay dividends, multiple credit-agreement covenants and Delaware law impose significant restrictions on upstreaming distributions. Accordingly, dividend payments, if any, are likely to be limited and conditional on both operational performance and compliance with financing and legal constraints.

Market Opportunity Overview

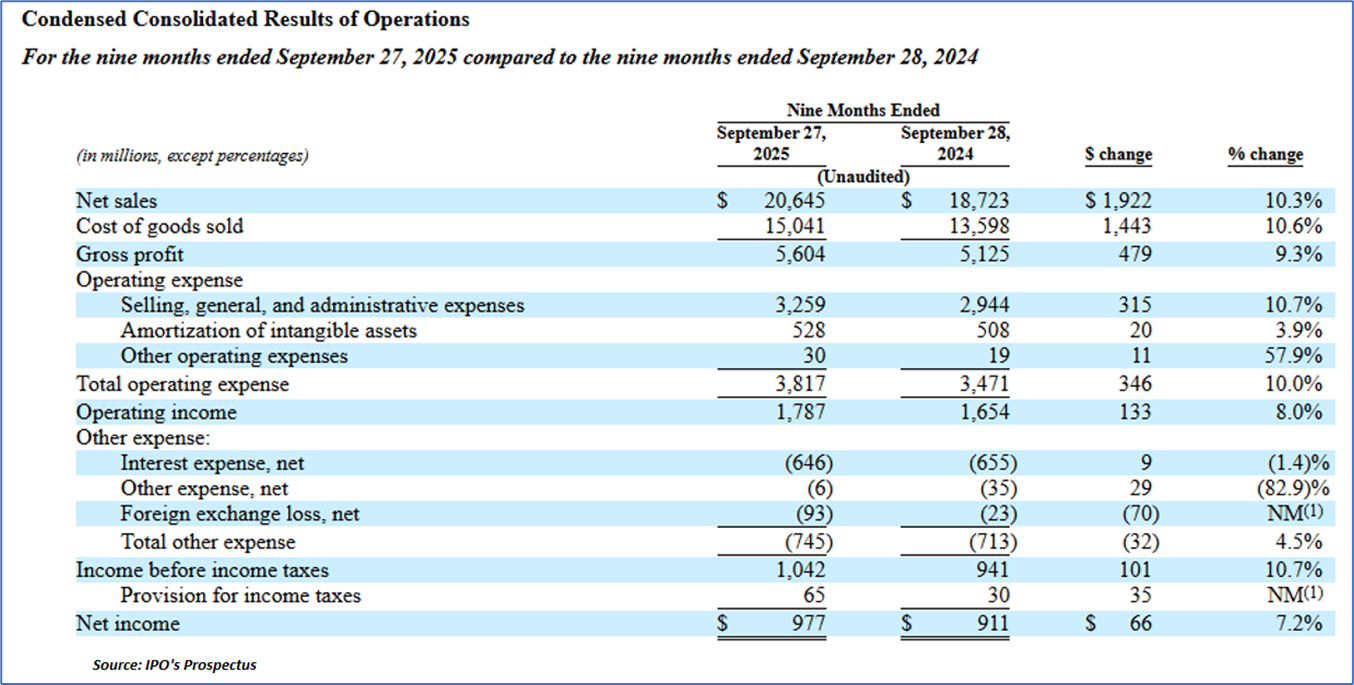

Financial Highlights (Results of Operations) (Expressed in USD)

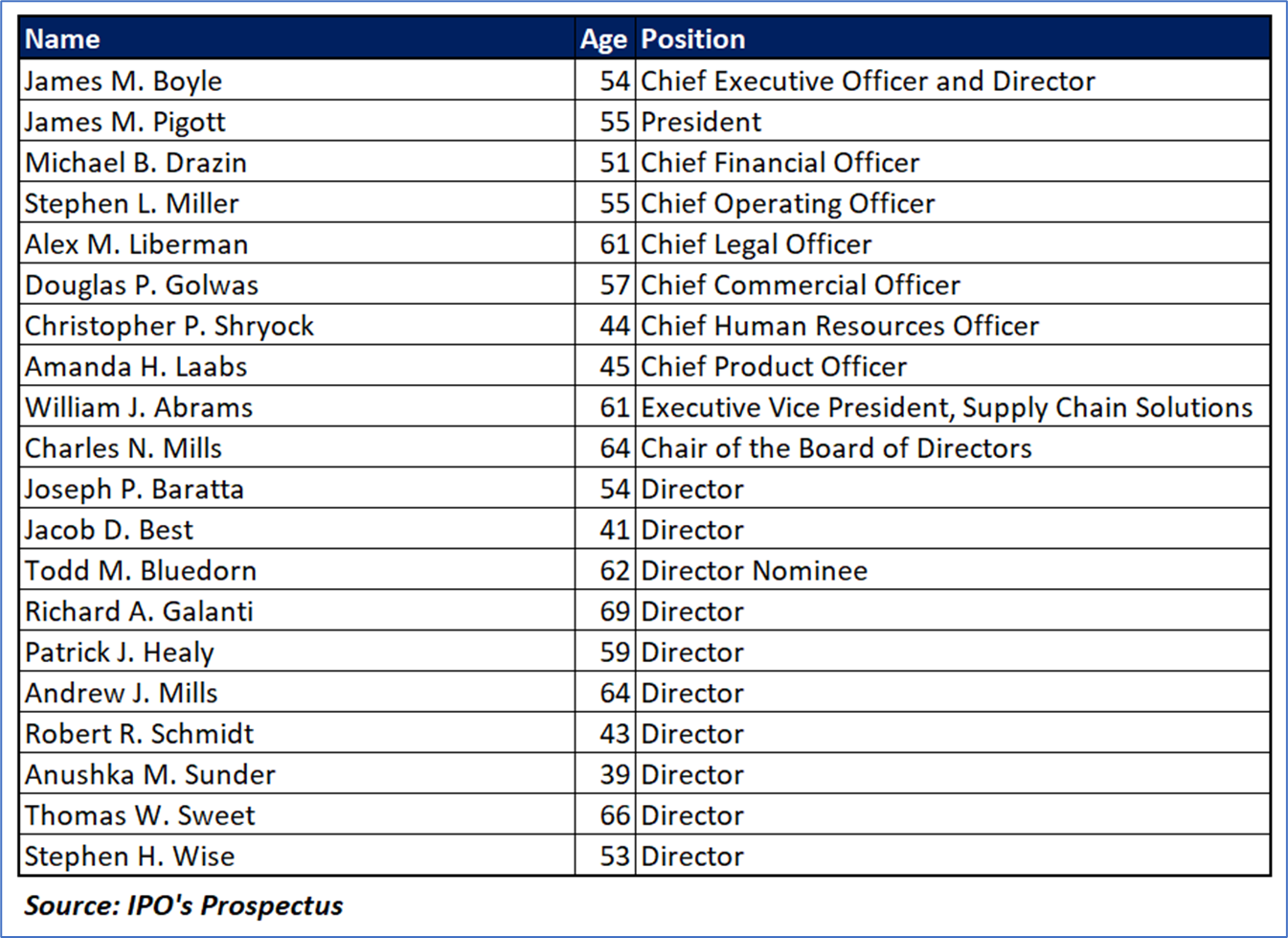

Key Management Highlights

Risk Associated (High)

Investment in the IPO of “MDLN” is exposed to a variety of risks such as:

Conclusion

JM Group Limited (JMG) is a Hong Kong–based sourcing solutions provider that supplies a broad range of consumer products across eight major categories to customers in markets including the U.S., Australia, Mexico, and Hong Kong, supported by in-house design, product development, and quality management capabilities. Through its IPO, the Company plans to raise approximately USD 14.86 million, which intends to allocate evenly toward brand promotion, talent recruitment, strategic investments, and general working capital, with flexibility retained for future adjustments. JMG operates within several expanding global markets—including home and tools, seasonal décor, sports and outdoors, and toys and games—each driven by long-term trends such as rising disposable income, increased health and lifestyle awareness, demand for customization, and growth of e-commerce, though each faces constraints ranging from economic sensitivity to supply-chain and regulatory pressures. Financially, JMG reported a 14.1% increase in revenue for the six months ended March 31, 2025, stronger profitability driven by lower SG&A due to a major credit-loss reversal, and improved operating cash flow alongside modest increases in merchandise costs tied to higher sales volume. Key risks include co

ncentration of revenue with a major U.S. customer, reliance on mainland China suppliers, and exposure to margin pressures within highly competitive, price-sensitive product categories.

Hence, given the financial performance of the company, use of proceeds, and associated risks “Medline Inc. (MDLN)” IPO seems “Neutral" at the IPO price.

Kalkine Equities LLC, with Delaware File Number 4697384, Foreign Qualification Registration in California File Number 202109211078, and Texas File Number 805521396, is authorized to provide general advice only. The information on https://kalkine.com/ does not take into account any of your investment objectives, financial situation or needs. You should consider the appropriateness of advice taking into account your own objectives, financial situation and needs and seek independent financial advice before making any financial decisions. The link to our Terms and Conditions and Privacy Policy has been provided for your reference. On the date of publishing the reports (mentioned on the website), employees and/or associates of Kalkine do not hold positions in any of the stocks covered on the website. These stocks can change any time and readers of the reports should not consider these stocks as advice or recommendations later.

Past performance is not a reliable indicator of future performance.

Please wait processing your request...

Please wait processing your request...